- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- AUD/USD fades corrective bounce after snapping four-day uptrend, reversing from the highest level in a month.

- RBA’s Lowe defends hawkish surprise by citing inflation woes, Australia Q1 GDP growth rate eases.

- Recently softer China data join fears of global economic slowdown to exert downside pressure on Aussie pair.

- Australia trade numbers, risk catalysts eyed for clear directions.

AUD/USD stays depressed around 0.6650 after reversing from a one-month high. In doing so, the quote struggles to find traction as hawkish concerns about the Reserve Bank of Australia (RBA) join growth fears to challenge the Aussie bulls. With this, the risk-barometer pair stays clueless amid the early hours of Thursday’s Asian session, after snapping a four-day uptrend the previous day.

The recent challenges to the major economies, as perceived from the latest downbeat statistics from the United States, China, Australia, Europe and the UK, renew recession fears and weigh on the AUD/USD price. Adding strength to the economic pessimism are the concerns surrounding higher interest rates from the top-tier central banks, especially after the latest hawkish surprises from the Reserve Bank of Australia and the Bank of Canada (BoC).

That said, China’s headline Trade Balance deteriorates to $65.81 billion versus the $92.0 billion expected and $90.21 billion previous readings. That said, the Exports and Imports came in mixed with the former falling past -0.4% expected and 8.5% previous readings to -7.5% YoY whereas the latter improves to 2.3% from -0.8% market forecasts and 4.2% prior. On the other hand, Aussie Q1 GDP rose 0.2% QoQ compared to 0.5% previous readings and 0.3% market forecasts. On the same line, the yearly GDP came in as 2.3% versus the analysts’ estimation of 2.4% YoY and 2.7% previous readings.

Even so, RBA Governor Philip Lowe signaled further rate hikes from the Aussie central bank and propelled the five-day uptrend of the Aussie pair. That said, the policymaker said, “Some further tightening of monetary policy may be required, depending on how economy and inflation evolve.” It should be known that the RBA surprised markets for the second time in a row by announcing a 25 basis points (bps) rate hike on Tuesday.

It should be noted that the latest Organisation for Economic Co-operation and Development (OECD) report, published Wednesday, mentioned, “The global economy is set for a weak recovery over the coming years as persistent core inflation and tighter monetary policy weigh on demand.”

While portraying the mood, Wall Street closed in the red whereas commodities and Antipodeans closed in the red. Further, the benchmark US 10-year Treasury bond yields rose the most in five weeks to 3.79% while the two-year counterpart marched to 4.52% at the latest.

Looking forward, Australia Trade Balance for April and the US weekly Initial Jobless Claims will be eyed for clear directions. However, major attention should be given to the risk catalysts and the yields as the latest shift in the market’s sentiment weighs on the risk-barometer pair.

Technical analysis

AUD/USD portrays reversal from two downward-sloping resistance lines from February 02 and 14 respectively, currently around 0.6715 by the press time. The pullback moves join downbeat oscillators to direct Aussie bears toward the 21-DMA support of around 0.6610.

As per the latest survey from the UK’s Recruitment and Employment Confederation (REC), funded by the global quant giant KPMG, published early Thursday, “Britain's labour market cooled further in May as starting salaries for permanent staff rose at the weakest pace in over two years.”

It should be noted that the recruiters included in the survey are the ones being closely watched by the Bank of England (BoE) and hence the results appear more important for the GBP/USD pair traders.

Also read: GBP/USD Price Analysis: Bulls are in the market but 1.2450s resistance could be tough

Key findings

REC said the number of permanent staff placements dropped last month at the sharpest rate since January 2021, as its gauge of demand for staff fell to a five-month low.

The survey chimed with other gauges of the labour market that show it is now clearly loosening.

REC's gauge of growth in starting salaries for permanent staff fell to its lowest level since April 2021, although it said this still represented ‘a historically sharp pace overall’.

Elsewhere, another poll of the Royal Institution of Chartered Surveyors' (RICS) hints that measure of new buyer enquiries rose to a net balance of -18, the least negative figure since -14 in May 2022, and up from -34 in April, per Reuters.

- NZD/USD stays pressured at the lowest levels in a week.

- NZ Q1 Manufacturing Sales improved from prior but slide beneath upbeat forecasts.

- Clear downside break of one-week-old symmetrical triangle, bearish MACD signals suggest further fall in Kiwi price.

- RSI conditions suggest bottom-picking around yearly low marked in the last week.

NZD/USD bears occupy the driver’s seat as the Kiwi pair remains depressed at the weekly low surrounding 0.6030 amid the early Asian session on Thursday, after falling the most in a fortnight the previous day.

In doing so, the Kiwi pair ignores the recently firmer New Zealand (NZ) data while paying more attention to the previous day’s downside break of a one-weeklong symmetrical triangle. That said, NZ Manufacturing Sales improves to -2.1% in the first quarter (Q1) of 2023 versus 3.9% expected and -4.7% prior.

It should be noted that the heaviest bearish MACD signals in nearly two weeks join the aforementioned triangle breakdown to keep the NZD/USD bears hopeful.

With this, the quote appears all set to prod the 0.6000 psychological magnet. However, the RSI (14) is below the 50.0 level and hence the yearly low marked in the last week around 0.5985 may offer an opportunity for the counter-trend traders to take the risk.

Should the quote fails to recover from 0.5985, the odds of witnessing a slump toward the early October 2022 top near 0.5815 can’t be ruled out.

On the contrary, NZD/USD recovery appears elusive unless the quote stays below the previously stated triangle formation’s bottom line, close to 0.6065 at the latest. Even so, the top of the triangle, near 0.6100, can act as an extra check for the bulls before giving them control.

Following that, a convergence of the 200-SMA and 50% Fibonacci retracement level of the pair’s May 10-31 downturn, around 0.6180, will be key to watch for the NZD/USD bulls.

NZD/USD: Four-hour chart

Trend: Limited downside expected

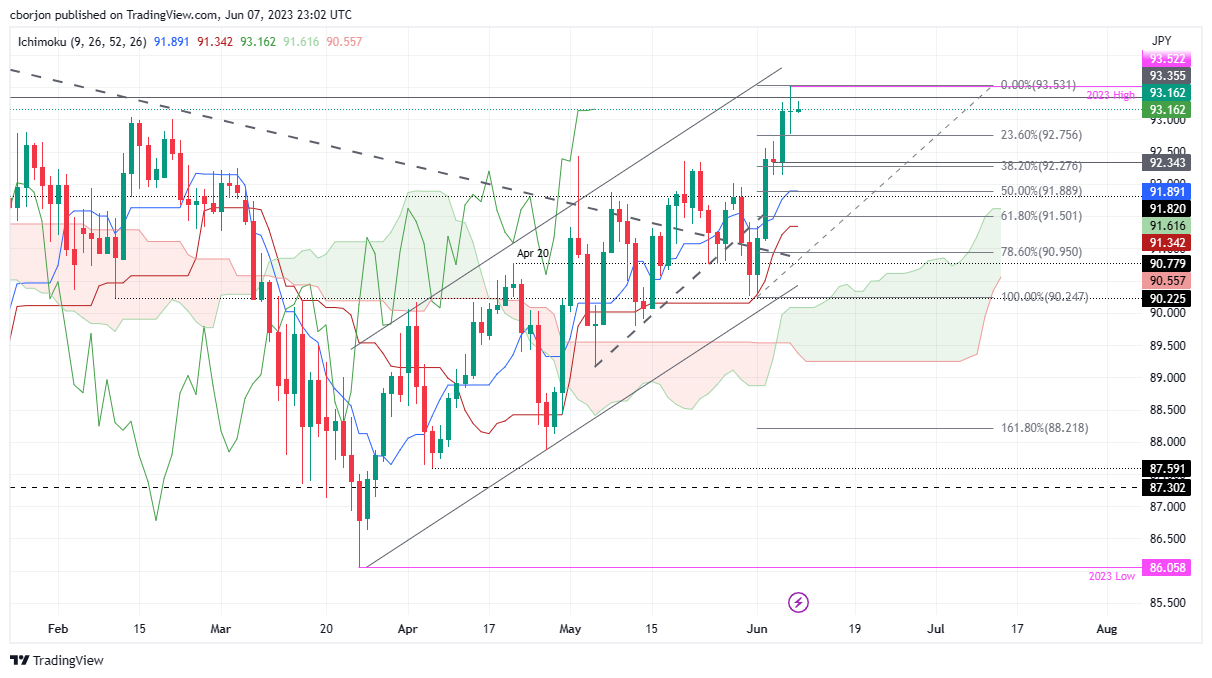

- AUD/JPY forms a doji at YTD highs, signaling a possible pause in the rally.

- Potential retracement could test the 91.89 support zone, an intersection of the 50% Fibonacci and Tenkan-Sen line.

- On the upside, surpassing the YTD high could push the pair towards 94.00, with a potential target at 95.00.

AUD/JPY hovers at around the 93.20 area as the Asian session begins, following Wednesday’s session, which formed a doji after reaching new year-to-date (YTD) highs. However, a daily close below the June 6 high of 93.26 suggests buyers are losing control ahead of Thursday’s session.

AUD/JPY Price Analysis: Technical outlook

AUD/JPY seems to pause its rally, as a doji emerged on Wednesday after hitting a new YTD high. However, in the medium term, the AUD/JPY is still upward biased but might pull back toward the confluence of the 50% Fibonacci retracement and the Tenkan-Sen line at around 91.89. Further downside is expected, towards the next confluence, of the Kijun-Sen line and the 61.8% Fibo retracement at around 91.34/50, before resuming its uptrend.

Conversely, a bullish continuation will witness the AUD/JPY exploding past the YTD high and testing the psychological level at 94.00. A breach of the latter will expose the November 16 daily high at 94.65, ahead of gaining traction and challenging the 95.00 figure.

AUD/JPY Price Action – Daily chart

US inflation expectations, as per the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve (FRED) data, rise to the highest levels in a week and justify the recently hawkish Federal Reserve (Fed) expectations, which in turn propel the yields. The same should have underpinned the US Dollar rebound but an absence of the Fed policymakers’ comments, due to the pre-FOMC blackout, joins a light calendar to restrict immediate USD moves.

That said, interest rate futures suggest an increase in the market’s bets on the Federal Reserve’s (Fed) 25 basis points (bps) of rate hike in July, even as June rate hike concerns are minimal.

It should be noted that the 5-year inflation expectations per the aforementioned calculations rise to the highest level in a week to around 2.15% by the press time whereas the 10-year counterpart rose for the third consecutive day to refresh weekly top near 2.21% at the latest.

Given the US inflation expectations and upbeat US Treasury bond yields, the US Dollar is likely to pick up bids. That said, the greenback’s gauge versus the six major currencies, namely the US Dollar Index (DXY), remained sluggish on Wednesday, mildly offered around 104.10 at the latest.

Also read: Forex Today: Another hawkish surprise shows inflation remains central bank’s main concern

- EUR/USD remains sidelined within trend continuation chart pattern.

- Sustained trading beyond five-month-old ascending support line lures Euro buyers.

- Looming bull cross on MACD, nearly oversold RSI signal EUR/USD’s further upside.

- Pennant’s top line, 100-DMA challenge Euro bulls before giving control.

EUR/USD steadies within a one-week-old Pennant formation, near 1.0700 by the press time of early Thursday in Asia, as bulls and bears jostle amid fears of economic slowdown, higher rates and softer Eurozone data.

Also read: Gold Price Forecast: XAU/USD bears ignore sluggish USD on mixed growth concerns, hawkish central banks

That said, the Euro pair’s rebound from a five-month-old ascending support line joins the recently downbeat RSI (14) line, as well as an impending bull cross on the MACD, to keep the EUR/USD buyers hopeful.

However, a clear upside break of the stated Pennant’s top line, currently around 1.0730, becomes necessary for the EUR/USD pair buyers to retake control.

Even so, the 100-DMA hurdle of around 1.0810 can check the upside momentum ahead of directing the Euro price towards the mid-May swing high of near 1.0910.

On a different page, the stated Pennant’s bottom line, close to 1.0670 by the press time, restricts the short-term downside of the EUR/USD, a break of which will drag the Euro pair to an upward-sloping support line from early January, near 1.0640.

It’s worth noting that the previous monthly low of around 1.0635 acts as an extra check for the EUR/USD bears, past 1.0640, before directing them to the lows marked in March and January, respectively near 1.0515 and 1.0480 in that order.

EUR/USD: Daily chart

Trend: Recovery expected

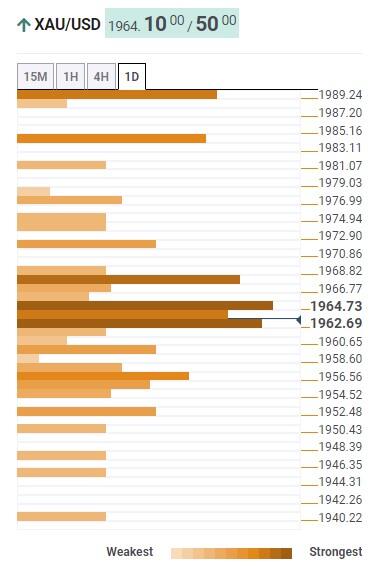

- Gold Price braces for the weekly loss despite sluggish US Dollar, taking offers to poke weekly low of late.

- XAU/USD retreats as hawkish central bank actions, fears of higher rates join downbeat statistics from major economies.

- Growth figures from Japan, Eurozone and United States employment clues eyed for clear directions of the Gold Price.

Gold Price (XAU/USD) remains bearish around the weekly low after snapping a two-day winning streak with a heavy loss to around $1,939 by the press time of early Thursday morning in Asia. In doing so, the precious metal bears the burden of the market’s fears of slowing economic growth and higher rates, as well as the firmer United States Treasury bond yields, even if the US Dollar remains sluggish.

Gold Price suffers from fears of economic slowdown, higher rates

Gold Price bears the burden of the recent challenges to the major economies, as perceived from the latest downbeat statistics from the United States, China, Europe and the UK. Adding strength to the economic pessimism are the fears of the higher interest rates from the top-tier central banks, especially after the latest hawkish surprises from the Reserve Bank of Australia and the Bank of Canada (BoC).

“The global economy is set for a weak recovery over the coming years as persistent core inflation and tighter monetary policy weigh on demand,” per the latest Organisation for Economic Co-operation and Development (OECD) report published Wednesday. The same raises doubts on the XAU/USD demand as China trade numbers trace the last week’s downbeat activity data while the German Industrial Production followed the previous day’s Factory Orders after marking the easy growth figure earlier. That said, the US activity numbers have been downeat and the Goods And Services Trade Balance also disappointed the previous day.

Not only the growth fears but the concerns surrounding the higher rates amid sluggish economic transition also weigh on the Gold Price.

On Wednesday, the Bank of Canada (BoC) surprised markets by announcing 25 basis points (bps) of increase to increase benchmark interest rate, to 4.75%, versus market expectations supporting no change in the previous rate of 4.50%. Earlier in the week, the RBA surprised markets for the second time in a row by announcing a 25 basis points (bps) rate hike.

Elsewhere, market’s bets of the Fedearl Reserve’s 25 bps rate hike in July increased, even as the June Federal Open Market Committee (FOMC) is likely to keep the rates unchanged. Even so, the OECD said, “(It) sees US Fed funds rate peaking at 5.25%-5.5% from Q2 2023, followed by two ‘modest’ cuts in H2 2024.”

Rising yields weigh on the XAU/USD

With the growth fears and hawkish central bank actions, as well as signals, the US Treasury bond yields rallied and weighed on the Gold Price the previous day. That said, the benchmark US 10-year Treasury bond yields rose the most in five weeks to 3.79% while the two-year counterpart marched to 4.52% at the latest.

It should be noted that the looming fears of a $1.0 bond issuance by the United States Treasury Department, due to the debt-ceiling deal, also prods the markets sentiment and weigh on the bond price, as well as bolster the yields. The same exerts downside pressure on the Gold Price.

While portraying the mood, Wall Street closed in the red whereas commodities and Antipodeans closed in the red.

Looking forward, growth numbers from Japan and Europe will join the weekly US Jobless Claims to entertain the Gold traders but risk catalysts and the bond market moves will be crucial to watch for clear directions.

Gold Price Technical Analysis

Gold Price breaks a one-week-old ascending support line while reversing the previous weekly gains.

That said, the steady conditions of the Relative Strength Index (RSI) line, placed at 14, join a looming bear cross on the Moving Average Convergence and Divergence (MACD) indicator to suggest further grinding of the XAU/USD towards the south.

With a clear downside break of the aforementioned support line, now resistance near $1,943, the Gold Price confirms a fall toward the monthly, as well as the yearly low, marked in the last week around $1,932.

In a case where the XAU/USD remains bearish past $1,932, the odds of witnessing a fall towards the 61.8% Fibonacci Expansion (FE) of May 10 to June 02 moves, near $1,910, can’t be ruled out.

On the contrary, the Gold Price recovery remains elusive unless the quote crosses the three-week-old horizontal resistance area surrounding $1,985, quickly followed by the 200-SMA level of around $1,987. That said, the support-turned-resistance line restricts immediate upside near $1,943.

Even if the XAU/USD crosses the $1,987 hurdle, the $2,000 psychological magnet will be crucial for the Gold buyers to surpass to tighten the grip.

Gold Price: Four-hour chart

Trend: Further downside expected

- GBP/JPY sees a bullish continuation, testing the year-to-date high amid a weaker JPY and BoE tightening expectations.

- A move past the YTD high could propel the pair toward the 175.00 supply zone and possibly a seven-year high.

- Potential correction below the Tenkan-Sen line could hit support at 172.66 and drop towards the Kijun-Sen line at 171.26.

GBP/JPY prints minuscule gains, with buyers eyeing a test of the year-to-date (YTD) high at 174.68 as the Asian session begins. On Wednesday, the GBP/JPY pair finished with gains of 0.42%, bolstered by a weaker Japanese Yen (JPY). Meanwhile, expectations for further tightening by the Bank of England (BoE) underpinned the Pound Sterling (GBP). Hence, the GBP/JPY exchanges hand at 174.28.

GBP/JPY Price Analysis: Technical outlook

GBP/JPY is set for a bullish continuation, as shown by the daily time frame. As the pair closes into the YTD high, price action turns choppy, which could open the door for a reversal, as the Tenkan-Sen line, at 173.59, is the closest to the current price action.

If GBP/JPY extends its gains past the YTD high, the next supply zone would be 175.00. A rally above that level could pave the way for the GBP/JPY to hit seven-year new highs and test the 2016 yearly high at 177.37.

Conversely, a fall below the Tenkan-Sen line and the GBP/JPY might correct lower. First, support would be found at the weekly low of 172.66. A breach of the latter will expose 2022 yearly high shifted support at 172.13, ahead of falling toward the 172.00 figure. Downside risks lie beneath that level, with the Kijun-Sen line at 171.26.

GBP/JPY Price Action – Daily chart

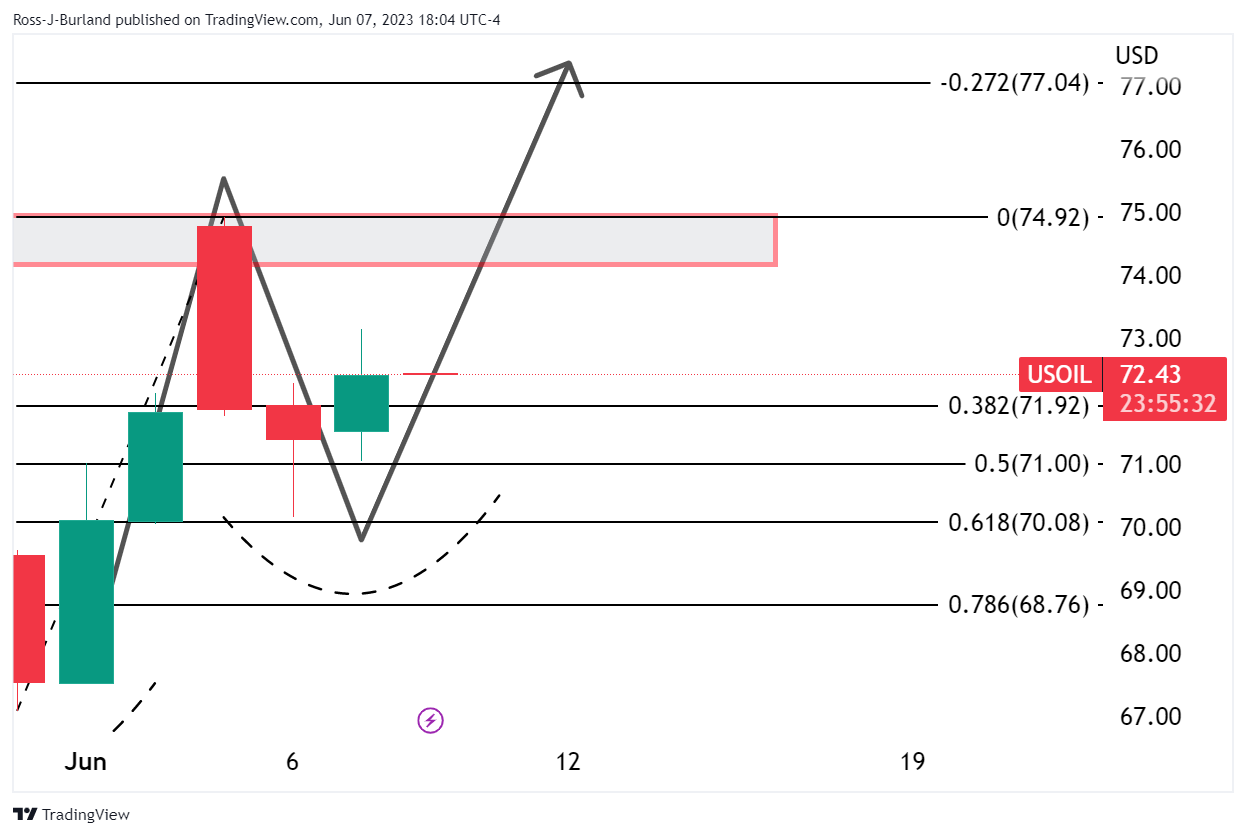

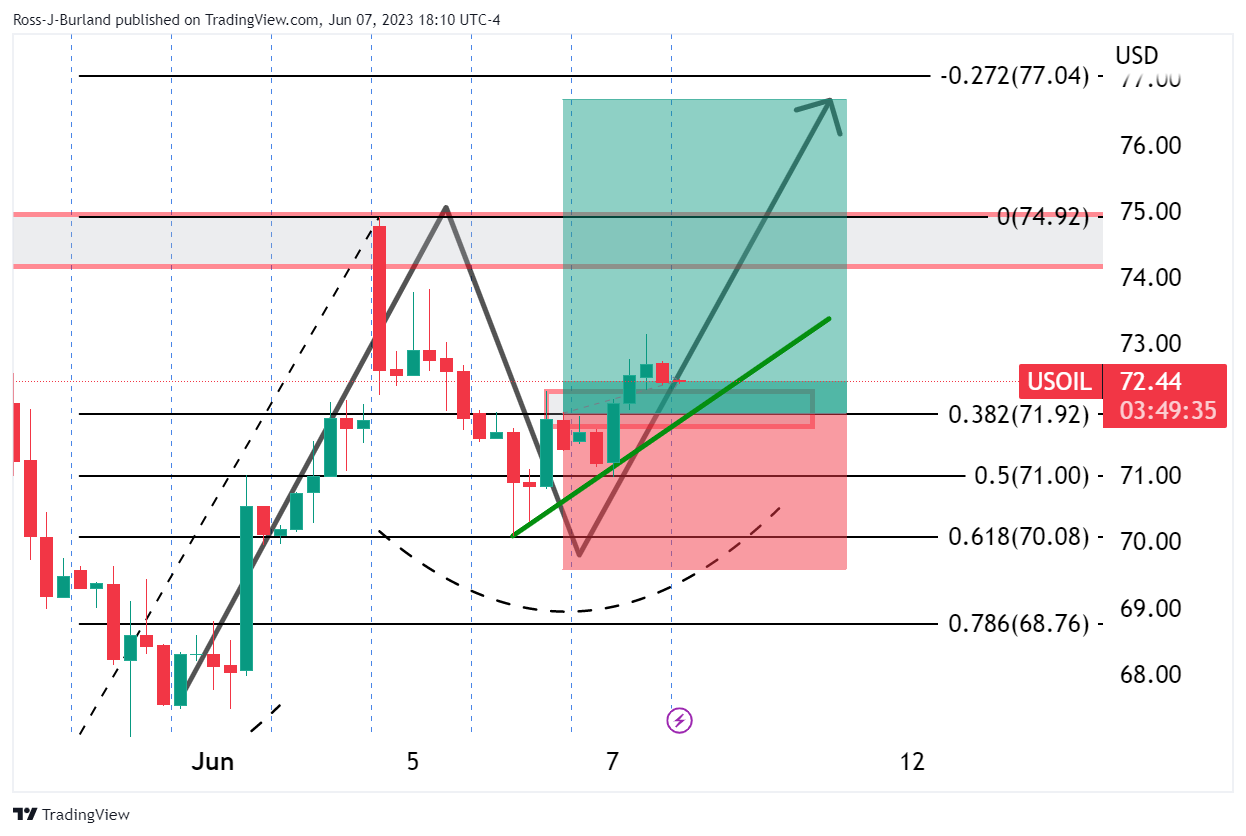

- WTI bulls looking to engage in anticipation of a bullish continuation.

- Daily inverse H&S is a compelling feature on the charts.

West Texas Intermediate, WTI, crude oil ended higher on Wednesday as a report showed an unexpected drop in US inventories while China's imports rose last month. Nevertheless, the bulls remain in good stead as per the following technical analysis:

WTI daily chart

We have an inverse head and shoulders which is bullish.

Pulling the chart across to see the impulse correction and what could now be another bullish impulse in the making, we can see that the market is supported at a 61.8% Fibonacci retracement level. This too is bullish.

WTI H4 chart

The 4-hour chart shows the price has breached prior resistance that could now well act as a support on the pullback. Bulls could be encouraged to enter the market in anticipation of a bullish continuation.

- USD/CHF shows bullish momentum, targeting the 0.9100 mark with 0.27% gains.

- RSI and three-day RoC indicators suggest bullish dominance despite sideways movement.

- Overcoming the 0.9120 hurdles could steer the USD/CHF toward the 0.9147 and 0.9200 landmarks.

USD/CHF bounces off the 50-day Exponential Moving Average (EMA) and threatens to claim the 0.9100 figure late after Wall Street closed. The US Dollar (USD), propelled by risk aversion, helped the USD/CHF to Regusters solid gains of 0.27%. At the time of writing, the USD/CHF is trading at 0.9090 after hitting a low of 0.9043.

USD/CHF Price Analysis: Technical outlook

From the USD/CHF daily chart perspective, the pair is neutrally biased, consolidated within the limits of solid support found around the 20- and 50-day EMAs, each at 0.9036 and 0.9040) and resistance at the 100-day EMA at 0.9123. Although price action remains sideways, the Relative Strength Index (RSI) shows bulls are in charge, further cemented by the three-day Rate of Change (RoC). Hence, the USD/CHF path of least resistance is upwards. Of note, the Average True Range (ATR) suggests that volatility in the pair could lean up to 60 pips.

Dialing into the USD/CHF hourly chart, price action remains sideways, though it broke above a resistance trendline late in the New York session, exacerbating a rally above 0.9100. However, buyers must reclaim the weekly high of 0.9120, so they can pose a threat toward the last week’s high of 0.9128. The breach of those levels will pave the way towards the R1 daily pivot at 0.9147, ahead of challenging the 0.9200 figure. Conversely, a fall below the daily pivot at 0.9083 could open the door towards the EMAs at around 0.9074/76, followed by the 200-EMA at 0.9065.

USD/CHF Price Action – Hourly chart

The Bank of Canada surprised markets with a rate hike on Wednesday, following the Reserve Bank of Australia's rate increase on Tuesday. These developments come ahead of a crucial week with meetings from the Federal Reserve and the European Central Bank. In terms of data for Thursday's Asian session, the highlights will be Japan's Q1 GDP. New Zealand will report Q1 Manufacturing Sales and Australia, trade data. Later in the day, the Eurozone's GDP and employment figures will be released, along with the weekly US Jobless Claims report.

Here is what you need to know on Thursday, June 8:

The Canadian Dollar outperformed on Wednesday following the Bank of Canada's surprise rate hike. Against expectations, the central bank raised its key rate by 25 basis points to 4.75%, citing persistent excess demand and increasing concerns that inflation could "get stuck" materially above the target. This decision follows the Reserve Bank of Australia's hike on Tuesday, which also exceeded economic consensus. In the upcoming week, the Federal Reserve, the European Central Bank, and the Bank of Japan will have their own monetary policy meetings.

The Fed remains in its blackout period, preventing markets from hearing any official comments. Recent data shows a weakening in the manufacturing sector, though there are no imminent signs of a recession. All eyes are now on the upcoming Consumer Price Index (CPI) report next Tuesday, which is expected to be a key determinant for the Fed’s decision.

Analysts at Wells Fargo commented on the US economic outlook:

We still expect the delayed effects of monetary tightening and tighter credit availability to dampen economic growth. However, the enduring strength of the labor market prompted upward adjustments to our forecast for employment, real disposable income and consumption, shifting the expected start of the downturn closer to the end of this year.

During Wednesday's American session, US Treasury yields surged as market participants pared back their bets for rate cuts by the Fed by the end of the year. However, the most likely scenario for next week's Fed meeting is that rates will remain unchanged. The 10-year Treasury yield settled at 3.79%, the highest since May 29. Global government bond yields rose in response to another surprise rate hike, while equity prices on Wall Street posted mixed results. The VIX dropped to 13.90, the lowest level since February 2020, despite ongoing caution due to a gloomy global outlook and higher interest rates.

With the debt ceiling drama now resolved, the Wall Street Journal is warning of a potential flood of over $1 trillion in Treasury bills that could trigger volatility across financial markets in the weeks ahead. Investors will be closely watching for any signs of disruption as this massive amount of new issuance hits the market.

China reported weak trade data on Wednesday, with exports dropping 7.5% YoY in May against expectations of a 1.8% decline. This marks the first contraction in three months. Meanwhile, imports dropped 4.5% YoY, less than the 8.0% decline expected by the market consensus. These disappointing numbers add pressure on Chinese officials to provide more policy support, including rate cuts. The USD/CNH climbed to 7.15, the strongest level since November.

EUR/USD continues to trade around 1.0700, moving sideways and stuck ahead of next week's central bank meetings. On Thursday, the Eurozone will release a new reading on Q1 GDP and Employment.

GBP/USD approached the 1.2500 level before falling back to the 20-day Simple Moving Average (SMA) around the 1.2430 area, as the US dollar gained strength. A consolidation below 1.2400 would indicate potential for further losses in the pair.

Rabobank’s GBP outlook:

The risk for GBP is that further progressive rate hikes from the Bank significantly undermines the recently improved growth outlook. The line-up of UK fundamentals has already been poor for some time. The backdrop has been been characterised by high inflation, weak growth in addition to low investment and productivity. The UK’s current deficit last year likely enhanced the vulnerability of the pound. This has shrunk recently, which could afford GBP a little protection. However, on the view that the ‘higher for longer’ interest rate story is set to support the USD into Q3, we see scope for cable to edge lower to GBP/USD1.22 on a 3 mth view.

The Japanese Yen was hit by rising government bond yields. USD/JPY jumped from 139.00, surpassing 140.00. Japan will report Bank Lending, Trade data, and a new estimate of Q1 GDP. Also due is the Eco Watches Survey.

USD/CAD tumbled to 1.3319 after the unexpected rate hike by the BoC. It then rebounded, trimming losses to stabilize at 1.3370/80. The crucial support area above 1.3300 remains firm.

AUD/USD dropped after a four-day positive streak. The pair failed to hold above 0.6700. A relevant short-term support is located at 0.6640. The momentum that emerged from the hawkish RBA hike and Governor Lowe's comments faded amid cautious markets and a slide in commodity prices. Australia will report exports and imports on Thursday.

NZD/USD dropped below 0.6050, posting the lowest daily close in a week. The 0.6000 psychological area is back on the radar.

Despite new government appointments with more market-friendly names, the Turkish Lira remains under pressure. USD/TRY gained more than 7%, reaching fresh record highs above 23.00. Meanwhile, the Mexican peso hit its highest level since 2016, with USD/MXN falling to 17.30.

Gold tumbled to $1,940 and is looking at May lows, affected by higher Treasury yields. Silver reversed after approaching $24.00, falling below $23.50. Crude oil prices rose more than 1% on the back of inventory data, despite rate hikes and trade data from China. The WTI barrel settled around $72.50.

Cryptocurrencies weakened, with BTC/USD losing 2.25% to $26,360. Volatility still prevails after the Securities and Exchange Commission sued Coinbase on Tuesday and asked for a temporary restraining order to freeze assets tied to Binance on Monday.

Like this article? Help us with some feedback by answering this survey:

- NZD/USD bears moved in despite soft US Dollar.

- Attention turns to US CPI and Fed next week and local GDP.

NZD/USD traded down some 0.65% on the day by the last 45 minutes of the US session on Wednesday. The US Dollar, however, was little changed on the day as per DXY as investors awaited US inflation data for May and the Federal Reserve’s interest rate decision next week.

´´The Kiwi is lower this morning, and this time it’s not because of USD strength (with the USD DXY little changed after a whippy night), but instead, the decline was an Antipodean AUD and NZD move,´´ analysts at ANZ Bank said:

´´Exactly what the driver was isn’t clear but both currencies have corrected against EUR and GBP, so call it a wash-up. One thing we do think bears saying is that the USD itself isn’t really budging despite having put things like the debt ceiling and bank wobbles behind it, and as markets eye an end to the tightening cycle.´´

´´Instead, it is holding up against most forecasters’ expectations. And last night’s rise in US bond yields may sustain it for a bit longer. New Zealand's first quarter manufacturing data today will be key for Gross Domestic Product next week, but we are also a little nervous about New Zealand's first quarter current account data next week.´´

Meanwhile, what might play into the hands of risk currencies such as the antipodeans is the sentiment around the central bank divergences. The prospects for the Fed to pause raising interest rates next week while the likes of the Bank of Canada, Australia, and the European Central Bank align a chorus of hawkish counterparts should underpin the risk on currencies. With that being said, there is the risk of a hawkish surprise at the Fed.

´´The headwinds on the US Dollar (banking sector weakness, debt ceiling battle) have been resolved even as the tailwinds (strong economy and robust labor market) pick up,´´ analysts at Brown Brothers Harriman have argued, ´´We look for this post-Nonfarm Payrolls rally to continue.´´

´´Fed tightening expectations remain steady,´´ the analysts said.

´´WIRP suggests odds of a hike this month around 30% and those odds rise to around 80% in July. More importantly, WIRP suggests around 50% odds of a rate cut by year-end. There has been quite a bit of Fed repricing in recent weeks but more needs to be done. ´´

´´ It’s going to be a close call for the Fed and the final determinant for its decision will be May CPI data next Tuesday.´´

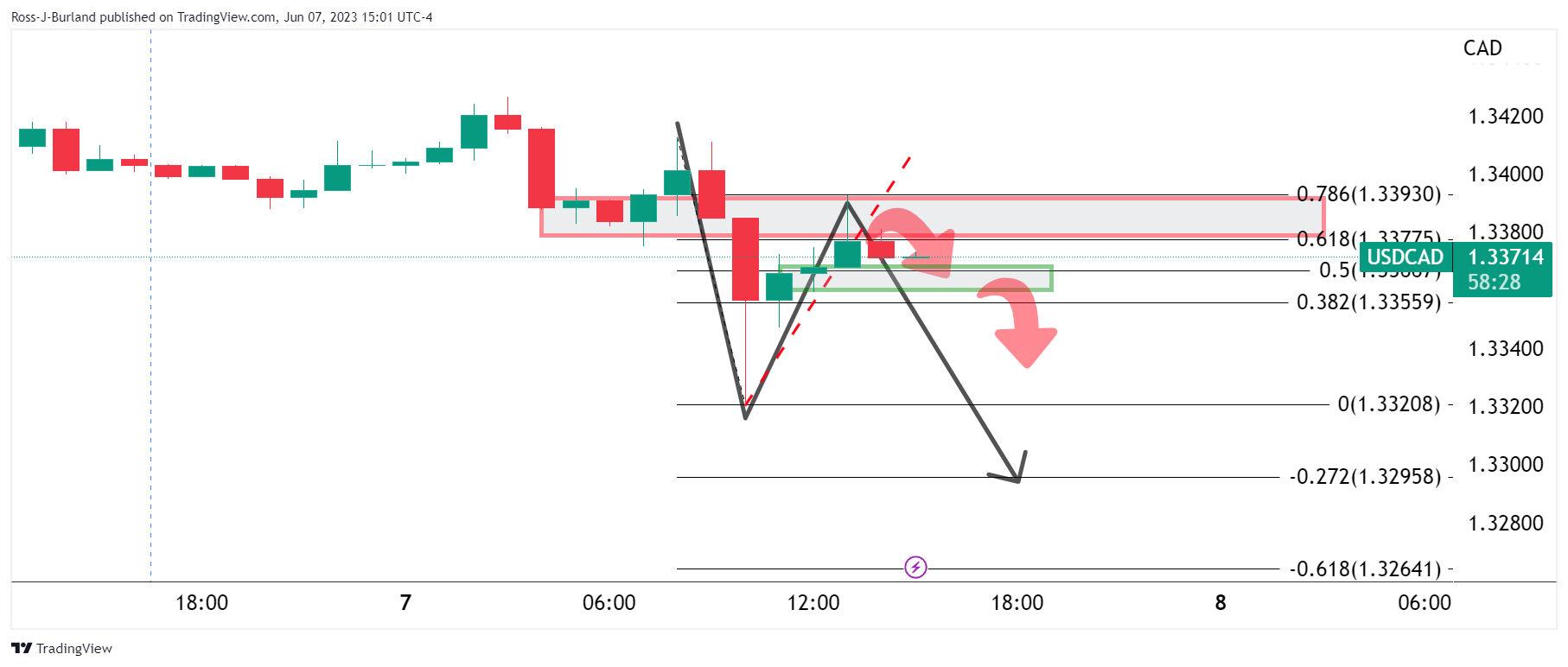

- USD/CAD bulls come up to meet resistance on the correction of the BoC induced sell-off.

- USD/CAD bears eye a downside extension on a break of 15-minute support area between 1.3370 and 1.3360.

The Canadian Dollar popped to a four-week high vs. the Greenback on Wednesday after the Bank of Canada said it would continue to raise interest rates next month after it tightened for the first time since January. The BoC showed its hand to the market as it warned that inflation could get stuck significantly above its 2% target amid persistently strong economic growth.

This has flipped the script technically ahead of US Consumer Price Index and the Federal Reserve events next week, putting the bears in control again as the following technical analysis will illustrate:

USD/CAD daily chart

The bears are targeting the lows and we could see further selling coming in following this meanwhile correction. However, traders would be aware of the CPI and Fed events at the start of next week and thus we could see some derisking into the events that would likely see a deceleration of the bearish impulse as drawn above.

USD/CAD H1 and M15 charts

For the time being, however, it appears that the correction is decelerating at resistance and this could lead to further selling pressure in the sessions and days ahead before the week is out. A downside extension could be on the cards if the 15-minute support area between 1.3370 and 1.3360 gives way with sellers potentially encouraged to add below 1.3350.

- USD/MXN sinks to a seven-year low, influenced by the MXN’s favorable interest rate and Fed’s dovish stance.

- Despite USD/MXN decline, higher US Treasury bond yields hint at a potential Fed rate hike in July.

- A widened US trade deficit for April, driven by falling exports and rising imports, contributes to USD’s depreciation against the MXN.

USD/MXN collapsed to new seven-year lows on Wednesday, as the interest rate differential favors the Mexican Peso (MXN), while the US Dollar (USD) weakened on last week’s Fed dovish commentary ahead of the next week’s monetary policy meeting. Even though a risk-off impulse is present in the markets, the USD/MXN is trading at around 17.3600s after hitting a daily high of 17.3915.

Interest rate differential Favors the Mexican Peso; therefore, further USD/MXN downside expected

Sentiment remains deteriorated, as shown by US equities. Higher US Treasury bond yields cushion the USD/MXN from falling further, as investors bet the US Federal Reserve would hike rates in July after skipping the June meeting. The CME FedWatch Tool portrays odds for a 25-bps increase at 50.8%, at around the same level as yesterday.

Nevertheless, G10 central banks tightening monetary policy after skipping some rate-setting decisions keeps investors nervous about the Fed’s next move. During the last week, policymakers stressed that a pause is necessary to assess the impact of the cumulative tightening in the economy.

Data-wise, the US economic agenda featured the US Trade Balance, showing the deficit broadened in April, compared with March’s data. Numbers came at $-74.6B in April of 2023, vs. March’s $-60.B. A notable dip in exports contributed to this shift, while imports rose sharply

The greenback shifted positively; printing gains as shown by the US Dollar Index (DXY). The DXY, which tracks the USD performance against a basket of six currencies, pares its earlier losses, up 0.04%, at 104.078.

USD/MXN Price Analysis: Technical outlook

After testing the 17.99 on May 26, the USD/MXN plunged 3.50%, sponsored by overall MXN strength. Swing In market sentiment tempered the pair’s fall, but even comments that the Bank of Mexico would keep rates unchanged for two meetings was no excuse for the MXN to appreciate. Technical indicators like the Relative Strength Index (RSI) and the three-day Rate of Change (RoC) suggest that sellers remain in charge. That said, the USD/MXN next support would be the year-to-date (YTD) low of 17.3046. A breach of the latter will expose the 2016 low of 17.0500 before diving to 17.0000. Conversely, the USD/MXN first resistance would be the 20-day EMA at 17.6314, followed by the 50-day EMA at 17.8587.

- GBP/USD bulls are moving in and eye a 38.2% Fibo retracement.

- Longer-term bulls eye a bullish extension from trendline support.

GBP/USD has traveled between a low of 1.2395 and a high of 1.2499 so far while it attempts to correct higher late in the New York day. At the time of writing, the pair is trading at 1.2444 and is 0.16% higher. Markets are looking ahead to the central bank meetings with the Federal Reserve scheduled for June 14 and the next Bank of England meeting is scheduled for June 22.

Meanwhile, the technical outlook is meanwhile bullish into a resistance area as follows:

The hourly chart shows an M-formation´s neckline as vulnerable to a restest as the price turns on a dime and moves in towards a 38.2% Fibonacci retracement level. However, bears could move in and target the trendline support.

Longer-term, we could have a scenario whereby the support holds and the bulls commit to target the 1.2580s-1.2680s as illustrated below:

- AUD bulls failed to hold above the 200-SMA after the RBA rate hike momentum.

- The cautious market mood following weak Chinese data favours USD.

- Rising US bond yields gave a boost to the greenback.

The AUD/USD trades with losses on Wednesday below 0.6650 area after hitting a daily high at 0.6717. A stronger US Dollar during the American session pushed the pair to the dowside. A surprising 25 basis point (bps) hike by the Bank of Canada (BoC) slightly strengthened the case for a hike by the Federal Reserve (Fed) in the upcoming June 13-14 meeting, sending US yields higher, favoring the US Dollar.

US bond yields rise ahead of Fed decision

The BoC announced on Wednesday a rate hike by 25 bps while markets expected them to maintain them steady at 4.5%. In that sense, adding to the Reserve Bank of Australia’s (RBA) decision on Tuesday, the expectations of a 25 bps hike next Wednesday by the Federal Reserve (Fed) slightly increased. However, the CME FedWatch tool suggests that investors are placing higher probabilities on the Fed refraining from hiking rates and instead, keeping the target rate steady at 5.25% but the odds of a 25 bps hike jumped to 30%.

As a reaction, the US bond yields are seeing gains across the curve. The 10-year bond yield rose to 3.79% seeing a 2.35 % surge on the day, while the 2-year yield stands at 4.60% with a 2.02 % advance and the 5-year yielding 3.95% with a 2.37 % increase respectively giving additional traction to the US Dollar.

Earlier on Wednesday, the AUD/USD peaked at 0.6717, the highest level since May 11, despite weak Chinese data. The Australian Dollar was boosted by a hawkish tone from RBA Governor Lowe. However, Australian Q1 GDP data fell below expectations, with a quarterly expansion of 0.2% compared to the market consensus of 0.3%.

Levels to watch

Technically speaking, the AUD/USD holds a neutral to bullish outlook for the short term as the bulls are struggling to maintain their dominance, but technical indicators are still favourable, suggesting that the market may still have some upside potential.

In case the Aussie recovers momentum, the following resistance line up at the 200-day Simple Moving Average (SMA) at 0.6690, followed then by the daily high at 0.6715/20 and the 100-day SMA at 0.6743. On the downside, the next support levels to watch are 0.6640, followed by 0.6605/10 and 0.6575 (weekly low).

- Silver prices dropped after testing weekly highs of $24.00, impacted by rising US bond yields.

- Bullish momentum was curbed by the strong US Dollar and significant resistance at the $24.00 area, according to technical indicators.

- Downward bias confirmed by bearish Relative Strength Index (RSI) and three-day Rate of Change (RoC).

Silver price dropped after testing weekly highs of $24.00, and retraces weighed due to elevated US bond yields, strong US Dollar (USD), and technical indicators. The XAG/USD exchanges hands at around $23.40s after hitting a weekly high of $24.05.

XAG/USD Price Analysis: Technical outlook

XAG/USD remains neutral-to-downward biased, unable to break decisively above the $24.00 mark area. Technical indicators, like the 50- and 20-day Exponential Moving Averages (EMAs) confluence at $23.71-$23.87, dragged Silver’s spot price lower.

Furthermore, the Relative Strength Index (RSI) indicator and the three-day Rate of Change (RoC) portray that sellers are in charge, both at bearish territory warrant downward action.

Therefore, the XAG/USD first support would be the current week’s low at $23.25, which, once cleared, the white metal could extend its losses toward the $23.00 figure. If XAG/USD slides further will challenge the 200-day EMA at $22.87.

Otherwise, the XAG/USD resistance area would be the abovementioned confluence of the 20/50-day EMAs, at around $23.71-$23.87, which, once breached, could spark a test of $24.00. if XAG/USD clears that area, the next supply zone would be the $25.00 mark.

XAG/USD Price Action – Daily chart

- USD/JPY rose past the 140.00 zone during the New York session.

- The US Dollar cleared daily losses amid rising US bond yields and a cautious market mood.

- Investors await Q1 Gross Domestic Product data from Japan.

The USD/JPY pair rose for a second consecutive day on Wednesday to currently trade around 140.00. On the other hand, as per the DXY index, the USD weakened against most of its rivals earlier but cleared daily losses finding support at 103.66 and recovering above 104.00 on the back of significant increases in the US bond yields. Another surprising rate hike, this time by the Bank of Canada (BoC), increased slightly the hawkish bets on the Fed.

BoC surprise decision fueled hawkish bets on the Fed

Market expectations for the upcoming June 13-14 Federal Reserve (Fed) still favour a no-hike despite the BoC surprise hike on Wednesday boosted prospects of another Fed hike. According to the CME FedWatch Tool, investors are betting on higher odds (64.7%) of the Fed not raising interest rates with expectations of maintaining the target rate at 5.25% but the probabilities of a 25 bps hike jumped to 30%

Against this backdrop, the US bond yields are seeing increases across the curve. The 10-year bond yield rose to 3.78%, while the 2-year yield stands at 4.59% and the 5-year yielding 3.94%, all up on the day, lifting the US Dollar.

On the other hand, the Yen's decline might be limited by speculations of Japanese authorities intervening in the markets to support the domestic currency. For Wednesday’s session, a cautious market mood amid weak Chinese economic data reported during the Asia session weighed on the JPY as it fueled a risk-off market mood.

USD/JPY levels to watch

According to the daily chart, the USD/JPY holds a neutral to bullish outlook for the short term. The Relative Strength Index (RSI) holds resilient above its midline while the Moving Average Convergence Divergence (MACD) fell slightly to the negative zone, but the pair trading above the 20-,100- and 200-day Simple Moving Averages (SMAs) suggests that the overall technical outlook is positive for the pair.

If USD/JPY manages to move higher, the next resistance to watch is at the 140.00 level, followed by the 140.50 zone and the psychological mark at 141.00. On the other hand, the 139.50 zone level is key for USD/JPY to maintain its upside bias. If breached, the pair could see a steeper decline towards the 139.00 psychological level and weekly low and then at the 20-day Simple Moving Average (SMA) at 138.60.

USD/JPY daily chart

- Gold prices decline, hindered by rising US bond yields and the greenback’s resilience; XAU/USD is down 0.50%.

- Gloomy global economic outlook impacts sentiment, with disappointing export data from China and broadened US trade deficit.

- The US dollar gains momentum as the US Dollar Index (DXY) pares earlier losses, adding pressure on gold prices.

Gold price retraces after facing solid resistance at the confluence of technical indicators, as well as weighed by rising US Treasury bond yields and a gloomy global economic outlook, with China’s export falling more than estimates. The XAU/USD is trading at $1952.36, down 0.50%, after hitting a daily high of $1970.15.

Resilient USD and risk aversion adds to XAU’s downward pressure; the US trade deficit widens

XAU/USD is on the defensive, weighed by high US bond yields, with the 10-year benchmark note climbing more than ten bps, at 3.774%. US real yields are heading towards the 1.60% region, a headwind for the yellow metal. China’s data revealed that Exports declined 7.5% YoY in US Dollar terms, below estimates for a 1.8% drop; meanwhile, Imports fell a less-than-forecasts at 4.5% YoY in May, vs. an 8.1% plunge.

The greenback shifted positively, printing gains as shown by the US Dollar Index (DXY). The DXY, which tracks the USD performance against a basket of six currencies, pares its earlier losses, up 0.04%, at 104.078.

Risk aversion is another factor impacting Gold prices as Wall Street tumbles. The trade deficit in the United States broadened, as reported by the Bureau of Economic Analysis (BEA), mainly attributed to A notable dip in exports contributed to this shift, while imports rose sharply. The Balance of Trade came at $-74.6B in April of 2023, vs. March’s $-60.B. Exports declined compared to April, came at $249B vs. $258.2B, while imports rose by $323B above March’s $318.8B.

Gold Price Analysis: XAU/USD Technical Outlook

XAU/USD remains consolidated, capped within the boundaries delineated by the 20 and 100-day Exponential Moving Averages (EMAs), each at $1968.35 and $1937.43. The Relative Strength Index (RSI) indicator remains in bearish territory, while the 3-day Rate of Change (RoC) confirms a bearish bias in the near term. Therefore, the XAU/USD first support would be the 100-day EMA, followed by the $1900 figure. A breach of the latter will expose the 200-day EMA at $1889.01. Conversely, if XAU/USD buyers reclaim the confluence of the 20 and 50-day EMA at around $1968-$1970, that would open the door for a rally toward the $2000 mark.

- EUR/USD buoyed by hawkish ECB commentary bounces off 200-day EMA as Fed June rate hike expectations fade.

- The US trade deficit widens significantly to $-74.6B, driven by a decline in exports and a rise in imports.

- Rate hikes by BoC and RBA influence US Treasury bond yields, signaling global central bank response to persistent inflation.

EUR/USD bounces off the 200-day Exponential Moving Average (EMA) and climbs above the 1.0700 handle due to European Central Bank (ECB) official hawkish commentaries boosting the Euro (EUR). Meanwhile, the US Dollar (USD) dives as expectations for Fed’s June rate hike fade. The EUR/USD is trading at around 1.070, a gain of 0.12%.

Euro strengthens against falling USD as G10 central banks scramble amid sticky inflation

Sentiment deteriorated after a brief jump in equities. A sudden slump of the CBOE Volatility Index (VIX), known as the fear index, to 2020 lows shifted investors’ mood, which appeared to book profits, though it remained away from the US Dollar. Before Wall Street opened, the US Bureau of Economic Analysis (BEA) revealed the US deficit widened, as shown by the Balance of Trade to $-74.6B in April of 2023, vs. March $-60.B. Exports declined compared to April, came at $249B vs., $258.2B, while imports rose by $323B above March’s $318.8B.

Lately, US Treasury bond yields, notably the 10-year benchmark note rate, climbed more than ten bps, up to 3.766%, after the Bank of Canada (BoC) lifted rates, following subsequent meetings holding rates unchanged. Therefore, the BoC added its name to the list, led by the Reserve Bank of Australia (RBA), of G10 central banks pausing rates, though had to scramble and increase them, as inflation probes to be stickier than estimated.

In the meantime, hawkish comments by ECB Klas Knot underpin the EUR/USD back above the 1.0700 figure. He noted that the ECB must lift rates in June and July and would become data-dependent. Knot added that peak interest rates “must be maintained for a long time to keep inflation in check.”

Earlier, Governing Council member Isabel Schnabel commented aggressive tightening takes longer than usual to impact the economy, said in an interview published by the ECB.

Datawise, Industrial Production in Germany improved compared to March’s plunge of -3.4%, coming at 0.3% MoM, below estimates of 0.6%. At the same time, France achieved a wider deficit than estimates of €-7.7B, coming at €-9.7B, greater than March €-8.39B, while Italy revealed an improvement in Retail Sales.

EUR/USD Technical Levels

Economists at ANZ Bank analyze Gold (XAU/USD) outlook.

Price dip presents a buying opportunity to build fresh long positions

Strong labour data suggests the Fed needs to tightening monetary policy more to bring inflation into its target range. While this remains a short-term headwind for Gold, other factors are supportive.

The recent price dip presents a buying opportunity to build fresh long positions.

We target $2,100 by the end of 2023.

See – Gold Price Forecast: Prospect of rising rates to weigh on XAU/USD until FOMC meeting – Commerzbank

Economists at MUFG Bank discuss the US Dollar outlook.

Consolidation at these stronger US Dollar levels seems likely

The mixed global growth backdrop remains supportive for the US Dollar at this stage.

Consolidation at these stronger US Dollar levels seems most likely given the probable declining appetite for position-taking ahead of a key week next week with the US Consumer Price Index (CPI) data and the FOMC and European Central Bank (ECB) meetings.

See: Slower growth everywhere ought to help the Yen – SocGen

- Bank of Canada raises policy rate by 25 basis points to 4.75%.

- Loonie jumps across the board following the decision.

- USD/CAD approaching April and May lows.

The USD/CAD plummet toward 1.3300 following the decision of the Bank of Canada (BoC) to raise its key interest rate taking markets off guard. The Loonie is outperforming on the back of the BoC decision.

The BoC raised interest rates by 25 basis points to 4.75%, against market consensus. In its statement, the central bank mentioned increasing concerns about the Consumer Price Index inflation getting “stuck materially above the 2% target”.

The BoC's decision follows an unexpected rate hike from the Reserve Bank of Australia (RBA) on Tuesday and comes ahead of next week’s decisions from the Federal Reserve, the European Central Bank, and the Bank of Japan.

Before the announcement, the USD/CAD was trading around 1.3390, but it quickly dropped to 1.3319, reaching the lowest level since May 8. The bias for the pair is clearly to the downside, moving towards critical medium-term support levels. It is approaching the April and May-June lows at 1.3299 and 1.3314, respectively. The next support area is the January lows around 1.3360.

USD/CAD daily chart

Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes the latest growth data and its implications for the FX market.

The most resilient major economy may be Japan

Monday’s US Services ISM data seem to have flown under the radar. They were very soft but haven’t had a discernible impact on rate pricing or on the Dollar.

I can understand why soft US data currently has less impact on EUR/USD (and indeed many other pairs) than usual – the US may be slowing but the European data are at least as bad and indeed the downturn is pretty general.

The most resilient major economy may be Japan, and that should provide some support for the yen as the market waits for next week’s BoJ meeting.

Economists at Commerzbank analyze the EUR outlook ahead of the decisions of the major central banks next week.

How long the EUR-positive effects will dominate and at which points the EUR-negative arguments will become more important?

We expect the Fed to cut interest rates quite soon (the first ones expect this for around the end of the year), but not so from the ECB. Medium-term the ECB’s monetary policy should therefore be more attractive from the FX market’s point of view.

At the same time, we expect that the ECB’s monetary policy course will be such that (a) a fall in core inflation to levels close to the 2% target cannot be expected longer term and that (b) inflation risks in the Eurozone will not principally disappear, which justifies an inflation and inflation risk premium which could put sustainable pressure on the Euro.

We admit openly: our current projections, which assume that the EUR-positive factors will dominate until the end of the year, is more the result of gut instinct than rational calculation. Please read our EUR projections (1.14 at the end of 2023, 1.08 at the end of 2024) with some caution in this respect!

- GBP/USD gains strong positive traction on Wednesday and snaps a three-day losing streak.

- Bets for an imminent Fed rate-hike pause continue to weigh on the USD and lend support.

- The prospects for further tightening by the BoE boost the GBP and contribute to the move.

The GBP/USD pair catches aggressive bids following an early dip to sub-1.2400 levels and builds on its intraday positive move through the early North American session on Wednesday. Spot prices jump to 1.2470 region, or a fresh weekly high in the last hour, snapping a three-day losing streak and stalling the recent pullback from a nearly three-week high touched last Friday.

The US Dollar (USD) comes under some renewed selling pressure as traders remain uncertain over the Federal Reserve's (Fed) rate-hike path and turns out to be a key factor acting as a tailwind for the GBP/USD pair. Last week's dovish rhetoric by several Fed officials lifted bets for an imminent pause in the US central bank's policy tightening cycle. That said, the recent inflation and labor market data from the US kept alive hopes for a 25 bps lift-off at the June FOMC meeting. This, in turn, leads to a modest recovery in the US Treasury bond yields, albeit fails to impress the USD bulls.

The British Pound, on the other hand, continues to be underpinned by expectations that the Bank of England (BoE) will be far more aggressive in policy tightening to contain stubbornly high inflation. Investors now expect the BoE to raise interest rates again from 4.5% to 4.75% on June 22 and see a roughly 60% chance that rate will peak at 5.5% later this year. The bets were lifted by the official data, which showed that the headline UK CPI fell less than expected in April and a closely watched measure of core price surged to a 31-year high. This is seen as another factor boosting the GBP/USD pair.

Meanwhile, investors now seem to have digested Wednesday's disappointing release of Chinese macro data, which showed that the trade surplus sank to a 13-month low in May and fueled worries about a deeper global economic downturn. This is evident from signs of stability in the equity markets, which could dent the Greenback's safe-haven status and supports prospects for a further intraday appreciating move for the GBP/USD pair. The positive outlook is reinforced by bullish technical indicators on the daily chart, which are still far from being in the overbought territory.

Technical levels to watch

- NZD/USD has turned sideways broadly amid an absence of a potential trigger.

- The US Dollar Index has resumed its downside journey after a less-confident pullback move to near 104.00.

- NZD/USD is auctioning in a Symmetrical Triangle that indicates a contraction in volatility.

The NZD/USD pair is demonstrating topsy-turvy moves in the early New York session. The Kiwi asset is auctioning in a tight range as investors are divided about the Federal Reserve (Fed)’s interest rate policy for June.

While the United States' solid labor market conditions are propelling the continuation of the rate-hiking spell by the Fed, deteriorating economic activities are telling a different story. The US Dollar Index (DXY) has resumed its downside journey after a less-confident pullback move to near 104.00.

The risk-on market mood has improved the appeal of the risk-perceived assets.

NZD/USD is auctioning in a Symmetrical Triangle chart pattern that indicates a contraction in volatility, which is followed by wider ticks and heavy volume after an explosion. The upward-sloping trendline of the aforementioned chart pattern is plotted from June 05 low at 0.6041 while the downward-sloping trendline is placed from June 02 high at 0.6112.

The 20-period Exponential Moving Average (EMA) at 0.6075 seems sticky to the asset, indicating a sideways performance.

Also, the Relative Strength Index (RSI) (14) has been confined into the 40.00-60.00 range, which signals that investors are awaiting a fresh trigger for a decisive move.

A confident break above May 25 high at 0.6110 will drive the Kiwi asset toward May 01 low at 0.6160 followed by the round-level resistance at 0.6200.

Alternatively, a downside move below the intraday low at 0.6015 will expose the asset for a fresh six-month low toward 11 November 2022 low at 0.5984. A slippage below the latter would expose the asset toward 02 November 2022 high at 0.5941.

NZD/USD hourly chart

- USD/TRY clinches fresh all-time highs past 23.00.

- Türkiye lenders appear to have halted their support for the lira.

- Investors home and abroad remain skeptical of the move so far.

The Turkish currency remains in free-fall, which motivates USD/TRY to advance to new record highs north of the 23.0000 hurdle on Wednesday.

USD/TRY looks at the government for clues

USD/TRY maintains the upside bias well in place on Wednesday as investors continue to assess the recent win by President Erdogan at the May 28 elections and the subsequent appointment of market-friendly finance minister M. Simsek.

In the meantime, Wednesday’s collapse of the lira seems to be attributed to state lenders discontinuing their sale of dollars to support the currency, indicating a shift in the new economic administration's approach. This change suggests a departure from expensive interventions and a move towards adopting more conventional economic policies.

So far, the Turkish currency has already depreciated around 24% since the start of the new year, while the drop has reached nearly 170% since the Turkish central bank (CBRT) embarked on its easing cycle in August 2021.

What to look for around TRY

USD/TRY maintains its upside bias well in place, always underpinned by the relentless meltdown of the Turkish currency.

In the meantime, investors are expected to closely monitor upcoming decisions on monetary policy, particularly after President R. T. Erdogan named former economy chief M. Simsek as the new finance minister following the cabinet reshuffle in the wake of the May 28 second round of general elections.

The appointment of Simsek has been welcomed with optimism by market members in spite of the fact that it is not yet clear whether his orthodox stance on monetary policy can survive within Erdogan’s inclination to battle inflation via lower interest rates.

In a more macro scenario, price action around the Turkish lira is supposed to continue to spin around the performance of energy and commodity prices - which are directly correlated to developments from the war in Ukraine, broad risk appetite trends, and dollar dynamics.

Key events in Türkiye this week: Industrial Production (Friday).

Eminent issues on the back boiler: Persistent skepticism over the CBRT credibility/independence. Absence of structural reforms. Bouts of geopolitical concerns.

USD/TRY key levels

So far, the pair is gaining 7.49% at 23.0676 and faces the next hurdle at 23.1582 (all-time high June 7) followed by 24.00 (round level). On the downside, a break below 19.6547 (55-day SMA) would expose 19.2926 (100-day SMA) and finally 18.9152 (200-day SMA).

Economists at Société Générale analyze USD/CAD technical outlook.

Short-term bounce is expected

USD/CAD has evolved within a range-bound consolidation since last October; a clear trend has been lacking as highlighted by crisscross moves around the 50-DMA.

The pair is now approaching the lower limit of its range near 1.3300/1.3220 which is a crucial support. Defence of this zone is essential to avert a deeper down move.

A short-term bounce is expected; April/May high of 1.3670 is likely to be an important hurdle.

- The oil price is marching towards $73.00 as hawkish Fed bets have slimmed vigorously.

- Weak China’s Trade Balance data failed to restrict the upside in the oil price.

- The discussions between US Blinken and Saudi Arabia’s Price, and US EIA inventory data will remain in focus.

West Texas Intermediate (WTI), futures on NYMEX, are looking to extend their recovery towards the crucial resistance of $73.00 in the early American session. The oil price showed a solid recovery amid a sell-off in the US Dollar Index (DXY) and deepening hopes of a steady interest rate policy announcement by the Federal Reserve (Fed).

In the Asian session, oil bears were heated after the release of weak China’s Trade Balance (May) data. In US Dollar terms, Trade Balance data dropped sharply to $65.81B vs. the estimates of $92B and the former release of $90.21B. Exports were sharply contracted by 7.5% while the street was estimated a marginal contraction of 0.4%.

The likes for Chinese products are getting wane and buyers are shifting to other countries for outsourced manufacturing. It is worth noting that China is the largest importer of oil in the world and weak economic prospects in China mean a filthy demand for oil.

The US Dollar Index (DXY) has sensed selling pressure after a minor pullback move to near 104.00. Rising bets for a neutral interest rate policy by the Fed are weighing significant pressure on the USD Index. Meanwhile, the US Goods and Trade Balance deficit has grown to $74.6B, lower than the estimates of $75.2B.

Going forward, oil inventory data for the week ending June 02, reported by the United States Energy Information Administration (EIA) will be keenly watched. Apart from that, investors will keep focusing on the discussions between US Secretary of State Antony Blinken and Saudi Arabia’s Price Mohammed bin Salman Al Saud.

- USD/JPY attracts some dip-buying and recovers a major part of its modest intraday losses.

- Rebounding US bond yields acts as a tailwind for the USD and lends support to the major.

- Economic woes, intervention fears could benefit the JPY and cap any meaningful upside.

The USD/JPY pair edges lower on Wednesday, albeit lacks any follow-through selling and remains confined in the previous day's broader trading range. Spot prices manage to recover a major part of the intraday losses back closer to the weekly low set on Tuesday and hover just above mid-139.00s, nearly unchanged for the day during the early North American session.

A combination of factors provides a modest lift to the Japanese Yen (JPY), which, in turn, prompts some intraday selling around the USD/JPY pair. Disappointing Chinese data, showing that trade surplus sank to a 13-month low in May led by a surprise slump in exports on the back of weaker overseas demand for Chinese goods, weighs on investors' sentiment. This is evident from the cautious mood around the equity markets and benefits traditional safe-haven assets, including the JPY.

Apart from this, speculations for more sizeable interventions by the Bank of Japan (BoJ) to support the domestic currency further underpin the JPY. This, along with the emergence of fresh US Dollar (USD) selling, contributes to the offered tone surrounding the USD/JPY pair. That said, the downside for the USD remains limited amid the uncertainty over the Federal Reserve's (Fed) rate-hike path, which is holding back traders from placing aggressive near-term directional bets.

Last week's dovish rhetoric by several Fed officials lifted bets for an imminent pause in the US central bank's policy tightening cycle.

That said, the recent inflation and labor market data from the US kept alive hopes for a 25 bps lift-off at the June

FOMC meeting. This, in turn, acts as a tailwind for the US Treasury bond yields, which seems to offer some support to the Greenback and assist the USD/JPY pair to attract some dip-buying ahead of the 139.00 round-figure mark.

There isn't any relevant market-moving economic data due for release from the US on Wednesday, leaving the USD at the mercy of the USD price dynamics. Apart from this, the broader risk sentiment will drive demand for the safe-haven JPY and provide some impetus to the USD/JPY pair. The range-bound price action witnessed since the beginning of the current week, meanwhile, warrants some caution before positioning for the next leg of a directional move.

Technical levels to watch

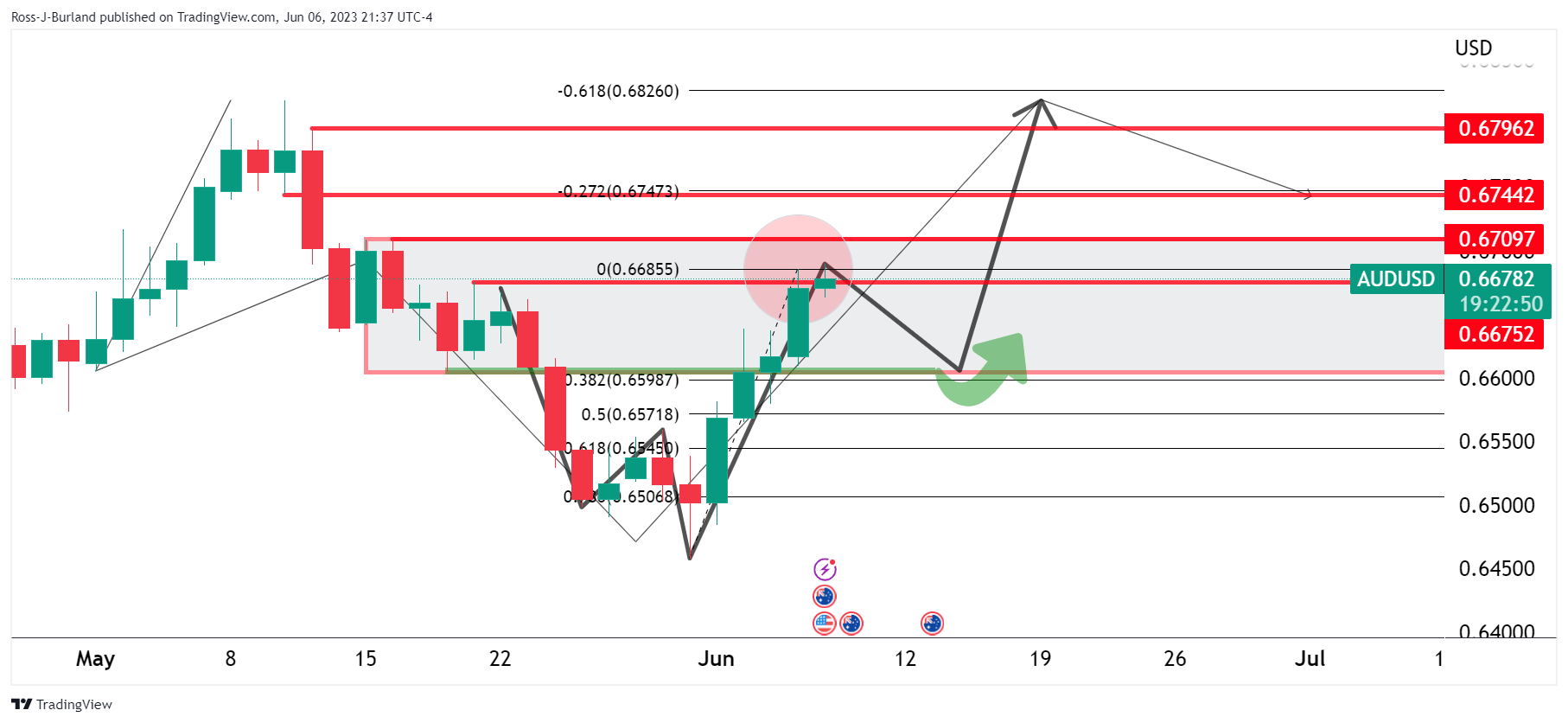

- AUD/USD is facing barricades in extending its rally above 0.6700, however, the upside bias is still solid.

- Offers for the USD Index soared dramatically as investors are anticipating a pause in the policy-tightening spell by the Fed.

- AUD/USD is auctioning in a Rising Channel in which each corrective move is considered a buying opportunity.

The AUD/USD pair is struggling in stretching its rally above the round-level resistance of 0.6700 in the early New York session. The Aussie asset is expected to climb above the aforementioned resistance confidently as the Reserve Bank of Australia (RBA) has opened room for further interest rate hikes to arrest stubborn Australian inflation.

S&P500 futures have added decent gains ahead of United States opening, portraying an upbeat market mood. The US Dollar Index (DXY) displayed a perpendicular fall after failing to recapture the previous day’s high at 104.30. Offers for the USD Index soared dramatically as investors are anticipating a pause in the policy-tightening spell by the Federal Reserve (Fed).

As per the CME Fedwatch tool, the chances of a neutral interest rate policy have jumped above 77%.

AUD/USD is auctioning in a Rising Channel on a two-hour scale in which each corrective move is considered as a buying opportunity by the market participants. The Aussie asset has comfortably shifted above the 61.8% Fibonacci retracement (plotted from May 10 high at 0.6818 to May 31 low at 0.6458) at 0.6682.

The Relative Strength Index (RSI) is oscillating in the bullish range of 60.00-80.00, indicating more upside ahead.

Should the Aussie asset confidently breaks above the round-level resistance of 0.6700, the Australian Dollar bulls will drive the asset toward April 18 high at 0.6748 followed by May 10 high at 0.6818.

On the flip side, if the Aussie asset breaks below June 01 low at 0.6484, US Dollar bulls would drag the asset to 01 November 2022 high around 0.6464 followed by the round-level support at 0.6400.

AUD/USD two-hour chart

- US Goods and Services Trade Balance came in at -$74.6 billion in April.

- US Dollar Index stays in the daily range below 104.00.

The United States international trade deficit in goods and services rose by $14 billion to $74.6 billion in April, the data published jointly by the US Census Bureau and the US Bureau of Economic Analysis revealed on Wednesday. This reading came in slightly below than the market expectation for a deficit of $75.2 billion.

Key takeaways from the report:

April exports were $249.0 billion, $9.2 billion less than March exports. April imports were $323.6 billion, $4.8 billion more than March imports.

The April increase in the goods and services deficit reflected an increase in the goods deficit of $14.5 billion to $96.1 billion and an increase in the services surplus of $0.6 billion to $21.6 billion.

Year-to-date, the goods and services deficit decreased $86.5 billion, or 23.9 percent, from the same period in 2022. Exports increased $55.9 billion or 5.8 percent. Imports decreased $30.6 billion or 2.3 percent.

Exports of goods decreased $9.4 billion to $167.1 billion in April.

Exports of services increased $0.2 billion to $81.9 billion in April.

Imports of goods increased $5.2 billion to $263.2 billion in April.

Considering figures for the first quarter, the biggest surpluses in trade were with South and Central America ($19.6), Netherlands ($13.5) and Australia ($8.2). The biggest deficits were recorded with China ($65.3), Mexico ($38.7), European Union ($35.0), Vietnam ($23.7), Germany ($22.5) and Japan ($16.6).

Market reaction:

The data was ignored by market participants. The US Dollar is trading in negative territory on Wednesday as the attention is set on next week’s inflation data and FOMC meeting. The DXY is falling 0.15% on the day, trading slightly below 104.00.

- EUR/USD leaves behind Tuesday’s pullback and retakes 1.0700

- The selling bias still dominates the sentiment around the pair.

EUR/USD regains upside traction and moves beyond the key barrier at 1.0700 the figure on Wednesday.

The pair remains well under pressure despite the bullish move and the continuation of the selling bias should prompt a probable test of the May low at 1.0635 (May 31) to emerge on the horizon in the short term. If spot clears the 1.0600 support it could then open the door to a deeper decline to the March low at 1.0516 (March 15).

A deeper pullback to the 2023 low at 1.0481 (January 6) would likely need a sharp deterioration of the outlook, which appears not favoured for the time being.

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0510.

EUR/USD daily chart

CAD is firmer ahead of the Bank of Canada (BoC) Interest Rate Decision. Economists at Scotiabank expect a hike to propel the Loonie.

Narrower spreads suggest CAD upside risk

We expect a 25 bps hike in the Overnight Target rate from the current 4.50%.

A somewhat hawkish hike (the policy statement is unlikely to shut the door definitively on more tightening) should put the CAD on course for the mid/low 1.33s at least.

Narrower, short-term US/Canada cash bond spreads already suggest some unrealized downside potential in USD/CAD which tighter BoC policy today may help achieve.

See – BoC Preview: Forecasts from six major banks, rates unchanged but hawkish bias

European Central Bank (ECB) governing council member Gabriel Makhlouf said on Wednesday that key rates are likely to stay there once they reach the "top of the ladder of increasing interest rates," per Reuters.

"Again I'm not going to say how long that will be, but I know some people in markets are pricing in cuts in rates at the end of the year and I'd be interested in how they are coming to those judgements," Makhlouf further added. Regarding the rate outlook, he explained that it would be a "question of judgement" whether they will need to continue with rate hikes after summer.

Market reaction

EUR/USD clings to modest daily gains above 1.0700 following these comments.

EUR/USD is firmer as steady support in upper 1.06s develops. Economists at Scotiabank analyze the pair’s outlook.

Gains through 1.07 have triggered a minor double-bottom signal

ECB policy hawks continue to stress the ‘more ground to cover’ on interest rate messaging (Knot, Schnabel), keeping market expectations high for hikes next week and Jul.

The EUR has found solid support on weakness to the 1.0670 zone over the past few days.

Solid intraday price gains through 1.07 have triggered a minor double-bottom signal which should see gains extend to the 1.0730 area, with a push through here signaling scope for an additional 60 pips or so of strength.

- Gold price has recovered from a minor fall to near $1,956.00 but has turned choppy again.

- The Fed is more likely to leave rates unchanged, rather than cut them any time soon.

- Gold price is showing signs of sheer volatility contraction as the US economic calendar has nothing much to offer.

Gold price (XAU/USD) has returned inside the woods after an attempt at a downside break in the late European session. The precious metal recovered after dropping to near $1,956.00 but has turned choppy again amid an absence of potential triggers.

The recovery move in the Gold price was supported by the vertical sell-off in the US Dollar Index (DXY). The USD Index has slipped below 103.90 as expectations for a raise in interest rates by the Federal Reserve (Fed) have receded. While monetary policies of other central banks belonging to the G7 cartel are far from any sort of a pause amid persistence in inflation in their respective countries.

Analysts at Rabobank cited that given the Fed is more likely to leave rates unchanged, rather than cut them any time soon, the U.S. dollar is likely to boast a natural edge over other currencies for now.

Meanwhile, S&P500 futures have recovered their losses and have turned positive amid rising hopes that Fed chair Jerome Powell will keep interest rates steady. Also, Fed Powell cited last that more interest rate hikes are less appropriate as tight credit conditions are doing the job effectively. The risk appetite of the market participants has improved, which has increased the appeal for risk-perceived assets.

Gold technical analysis

Gold price is showing signs of sheer volatility contraction as the US economic calendar has nothing much to offer. Investors should note that a squeeze in volatility is followed by an expansion in the same, which results in wider ticks and heavy volume.

On a broader note, Gold price is consolidating in a range of $1,932-1,985 for the past three weeks on a four-hour. Horizontal support is plotted from March 15 high at $1,937.39. The magical 200-period Exponential Moving Average (EMA) at $1,975.47 is acting as a strong barrier for the Gold bulls.

An oscillation in the 40.00-60.00 territory by the Relative Strength Index (RSI) (14) indicates a non-directional performance.

Gold four-hour chart

Economists at TD Securities discuss the Bank of Canada (BoC) Interest Rate Decision and its implications for the USD/CAD pair.

Dovish (40%)

Rates unchanged. Bank holds overnight rate at 4.50% as it seeks more evidence that outlook has shifted materially. Statement acknowledges Q1 GDP and labour market strength but also points to weaker survey data, still-anchored inflation expectations, and states that growth is expected to slow to justify pause. Bank maintains forward guidance, leaving hikes on the table if outlook continues to strengthen. USD/CAD +0.40%.

Base-Case (60%)

25 bps hike. Bank steps off the sidelines with hike to 4.75% after accumulation of upside data surprises. Statement has a hawkish tone, cites resilient economic conditions, sticky core inflation pressures, and subsiding US banking risks. Economy remains in excess demand and further tightening still on the table if required. USD/CAD -0.60%.

GBP/USD tracks other majors higher. Economists at Scotiabank analyze the pair’s technical outlook.

Good demand on GBP dips has developed so far this week

Good demand on GBP dips has developed so far this week, putting some positive work in on the daily chart – implying a short-term low may be in at least at Monday’s low.

Cable gains through 1.2470 (40-Day Moving Average) will add to the positive tone in the short run at least and put a return to the mid-1.25s on the radar.

Economists at Commerzbank assess BRL outlook ahead of Brazilian inflation figures.

Political factors pose greater risk to BRL than inflation for now

The June meeting of the National Monetary Council, which will review the inflation target and set a new one for 2026, is more important for the Real exchange rate than today's inflation figures.

Possible attempts by the government to influence the hawkish monetary policy in a more dovish direction via the inflation target or the appointment of new BCB directors, also due in June, remain the biggest risks for the BRL. However, we will only know whether and to what extent such concerns are justified at the first interest rate decision after the National Monetary Council meeting and with the participation of the new directors, probably in August.

See – USD/BRL: Decline to extend on failure to defend 4.89 – SocGen

- DXY fades Tuesday’s uptick and returns to the sub-104.00 region

- Further choppiness seems probable in the near term .

DXY leaves behind Tuesday’s decent gains and resumes the downside below the key 104.00 support on Wednesday.

Considering the ongoing price action, the index could now move into a consolidative phase in light of the current lack of strong catalysts. On the downside, the June low of 103.38 (June 2) emerges as the immediate contention, while the next up-barrier is seen at the May peak of 104.79 (May 31).

Looking at the broader picture, while below the 200-day SMA at 105.51 the outlook for the index is expected to remain negative.

DXY daily chart

- EUR/JPY trades in an inconclusive fashion above 149.00

- Further consolidation appears likely for the time being.

EUR/JPY keeps the trade below the 150.00 region so far on Wednesday.

In case bulls regain the initiative, there is an immediate hurdle at the so far monthly high at 150.19 (June 5). The convincing surpass of this level could put the weekly top at 151.07 (May 29) back on the radar prior to the 2023 peak at 151.61 (May 2).

So far, further upside looks favoured while the cross trades above the 200-day SMA, today at 144.10.

EUR/JPY daily chart

- USD/CAD turns lower for the second straight day and drops to a nearly four-week low.

- A goodish intraday pickup in Oil prices underpins the Loonie and exerts some pressure.

- The emergence of fresh USD selling contributes to the slide ahead of the BoC decision.

The USD/CAD pair attracts fresh sellers following an intraday uptick to the 1.3425 area and turns lower for the second straight day on Wednesday. The downward trajectory extends through the first half of the European session and drags spot prices to a nearly four-week low, around the 1.3380 region in the last hour.

A goodish pickup in Crude Oil prices underpins the commodity-linked Loonie, which, along with the emergence of fresh selling around the US Dollar (USD), exerts downward pressure on the USD/CAD pair. the recent inflation and labour market data from the US kept alive hopes for a 25 bps lift-off at the June FOMC meeting. That said, last week's dovish rhetoric by several Fed officials lifted bets for an imminent pause in the US central bank's policy tightening cycle. This leads to a further decline in the US Treasury bond yields and keeps the USD bulls on the defensive.

The upside for Oil prices, meanwhile, seems limited in the wake of worries that a global economic slowdown will dent fuel demand. The concerns resurfaced following the release of weaker Chinese data, which showed that the trade surplus sank to a 13-month low in May on the back of a surprise slump in exports. This, in turn, suggests that overseas demand for Chinese goods remained weak and poses additional headwinds for the world's second-largest economy. This overshadows additional supply cuts by Saudi Arabia/OPEC and could cap the black liquid.

Traders might also refrain from placing aggressive bets and prefer to wait on the sidelines ahead of the Bank of Canada (BoC) policy decision, due to be announced later during the North American session. The stronger-than-expected employment details and a slight pick-up in price pressures might have raised the possibility of another unanticipated hike by the BoC. Nevertheless, the latest monetary policy update, along with Oil price dynamics, should influence the Canadian Dollar (CAD) and produce short-term trading opportunities around the USD/CAD pair.

Technical levels to watch

EUR is losing more steam. Economists at Credit Suisse analyze the shared currency outlook.

Only 70 bps of rate cuts are priced for the ECB from Sep ’23 to Sep ’24

Softer inflation data are causing EUR to lose upward momentum.

The fact that only 70 bps of rate cuts are priced for the ECB from Sep ’23 to Sep ’24 stands in sharp contrast with the more aggressive rate cut pace priced into the US curve.

EUR is left as a relative G10 low yielder that is now losing the upward rate momentum that was so instrumental to its strength over the past 8 months, but without the cushion of dramatic 2024 cuts having already been priced in. This in our view leaves open the door for EUR/USD to test 1.0500 near term.

The Canadian Dollar has been the best G10-performing currency in the past month. Economists at ING analyze CAD outlook ahead of the Bank of Canada meeting.

A hawkish hold from the BoC

We favour a hawkish hold, signalling that if there isn’t clearer evidence of softening in price pressures it could raise rates again in July.

A hawkish tone by the Bank of Canada at the June meeting is clearly an important element to keep the bullish narrative for CAD alive.