- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- US Dollar Index edges lower as weak US data weigh on hawkish Fed bets.

- Pre-FOMC blackout, light calendar elsewhere also prod DXY bulls.

- Absence of US default fears jostles with fresh banking woes to challenge risk appetite.

US Dollar Index (DXY) stays defensive near 104.00 amid early Tuesday, after a volatile week-start that initially portrayed a run-up to 104.40 before marking a no-change day in the end.

The greenback’s gauge versus six major currencies dropped the previous day amid downbeat US data and Treasury bond yields. In doing so, the DXY also bears the burden of an absence of the Federal Reserve (Fed) talks amid the pre-FOMC blackout ahead of next week’s monetary policy meeting.

Talking about the data, US ISM Services PMI declined to 50.3 for May versus 51.5 expected and 51.9 prior whereas growth of the Factory Orders also deteriorated during the stated month to 0.4% versus 0.5% market forecasts and 0.9% previous readings. It should be noted that the final readings of S&P Global Composite PMI and Services PMI also marked softer figures for May.

With the softer US statistics, the market’s bets on the Fed’s June rate hike dropped from around 80% in the middle of the last week to nearly 25%. The same could have joined an absence of the Fed talks to weigh on the US Treasury bond yields and the US Dollar.

It should be noted, however, that International Monetary Fund (IMF) Managing Director Kristalina Georgieva suggested during the weekend that the Fed needs to do more to tame inflation, which in turn probed the Gold buyers.

Elsewhere, concerns about the need for the US large banks to hold more capital to battle the landing crisis contrasted with the policymakers’ ability to avoid the debt-ceiling expiration and confused the market players, as well as the DXY traders.

Moving on, a light calendar and the Fed blackout may keep troubling the momentum traders. That said, the US Consumer Price Index for May, due on June 13, is the next major US economic release before the Federal Open Market Committee (FOMC) monetary policy meeting on June 13-14.

Technical analysis

Monday’s “Gravestone Doji” bearish candlestick on the DXY’s daily chart drags it to the 100-day Exponential Moving Average (EMA) support of around 103.35.

- The Euro gained against the GBP on Monday for a second consecutive session.

- UK reported upbeat PMI revisions and while the EU reported weaker figures.

- The Euro held its foot on the back of hawkish comments from ECB’s Lagarde.

At the beginning of the week, the EUR/GBP gained traction, closing near 0.8615 as the Euro gained traction on the back of hawkish comments from European Central Bank (ECB) president Christine Lagarde. On the other hand, the Sterling, traded weak against most of its rivals, despite strong PMI revisions.

Hawkish comments from Lagarde gave the Euro impulse

According to S&P Global and Hamburg Commercial Bank (HCOB), the Composite PMI from the European Union (EU) decreased to 52.8 in May, which was lower than both the consensus estimate of 53.3 and the initial reading of 53.3. Similarly, the Services PMI was revised downward to 55.1 from 55.9.

However, the Euro managed to hold its ground on the back of Christine Lagarde's comments at the beginning of the American session, showing concern with persistent inflationary pressures. Rising German yields, with 10-year and 2-year bonds, were up by over 3%, signalling market anticipation of the ECB's proactive measures to tackle inflation concerns.

On the British side, the May final estimates of the S&P Global/CPIS, the Composite Purchasing Managers' Index (PMI), saw an upward revision, reaching 54 from the initial reading of 53.9. Similarly, the Services PMI was revised upwards to 55.2 from the previous figure of 55.1.

Levels to watch

Technically speaking, the EUR/GBP maintains a bearish outlook for the short term, as per indicators on the daily chart. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) are both showing weakness, standing deep in negative territory. The pair trades below its main moving averages, indicating that the sellers have the upper hand.

In case the pair sees more downside, support levels line up at the 0.8600 zone and below around the 0.8580 area and the multi-month low at the 0.8565 level. Furthermore, a move above 0.8620 would pave the way towards the 0.8650 area and the 20-day Simple Moving Average at 0.8665.

- AUD/USD grinds near the highest level in a fortnight after three-day uptrend.

- Convergence of 50-DMA, 50% Fibonacci retracement guards immediate upside.

- Upbeat oscillators, recovery from falling wedge’s bottom line keeps Aussie buyers hopeful.

- RBA is expected to keep current monetary policy unchanged amid market’s indecision.

AUD/USD bulls take a breather around 0.6620, making rounds to a two-week high amid Tuesday’s sluggish session as Aussie pair traders await the Reserve Bank of Australia’s (RBA) Interest Rate Decision. In doing so, the quote remains sidelined after rising in the last three consecutive days, following a bounce off the yearly falling wedge’s bottom line.

Also read: Reserve Bank of Australia Preview: AUD/USD ready for another hike?

The Aussie pair’s rebound from the support line of a falling wedge established since late December 2022 crossed 61.8% Fibonacci retracement of October 2022 to February 2023 upside and teased the buyers in the last few days. Adding strength to the upside momentum are the recently bullish MACD signals and upbeat RSI (14) line to keep buyers hopeful.

With this, the AUD/USD pair is all set to confront a convergence of the 50% Fibonacci retracement level and the 50-DMA, around 0.6660. However, any further upside beyond the same hinges on the RBA’s capacity to lure the bulls.

Following that, the aforementioned falling wedge bullish chart pattern’s top line, close to 0.6730 at the latest, becomes crucial to watch for clear directions.

Should the quote rises past 0.6730, the odds of witnessing a run-up towards crossing the previous monthly high of around 0.6720 can’t be ruled out.

On the contrary, pullback moves may initially aim for the 61.8% Fibonacci retracement level, also known as the golden Fibonacci ratio, close to 0.6545 at the latest.

However, the AUDUSD bears need validation from the wedge’s bottom line, surrounding 0.6495 by the press time.

AUD/USD: Daily chart

Trend: Further upside expected

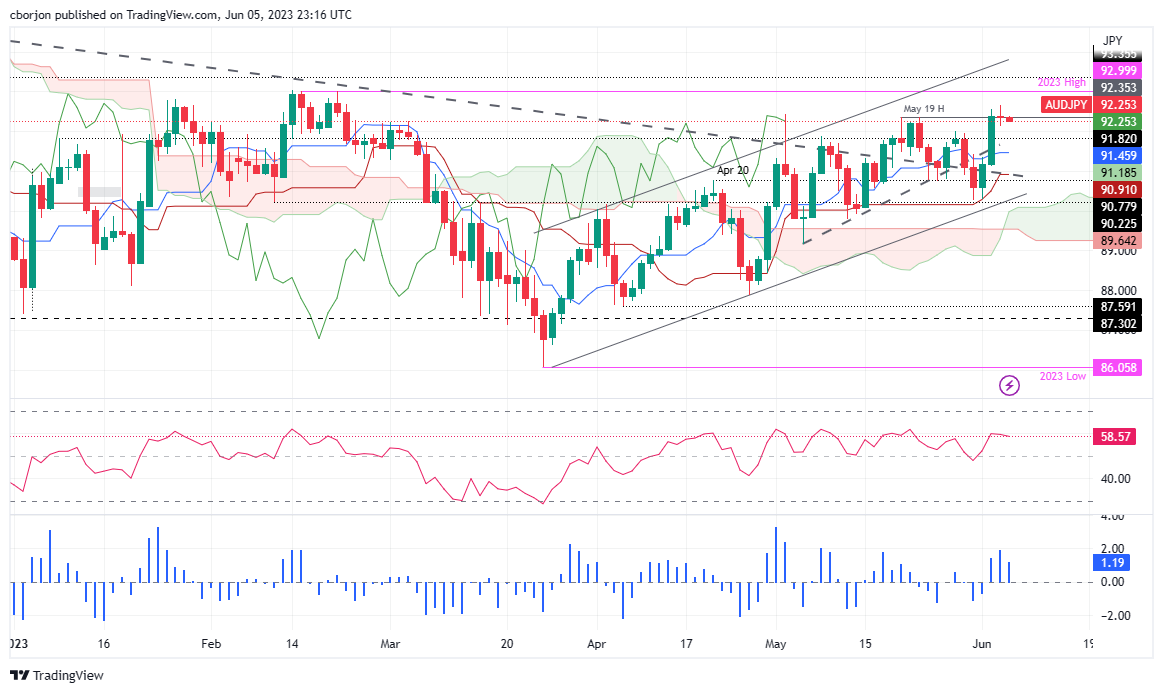

- AUD/JPY experiences a risk-off impulse amid decelerating US business activity and RBA’s monetary policy.

- Despite a lingering upward bias, market sentiment may shift due to the pair’s sensitivity to risk changes, potentially leading to violent swings.

- A balance of technical indicators suggests that AUD/JPY could target a lower range, with resistance remaining at the four-month and year-to-date highs.

AUD/JPY forms a doji, as shown by the daily chart, after hitting a fresh four-month high at 92.66, hovering nearby the 92.30s area, after trading within the 9213/66 range on Monday. A risk-off impulse was the main reason behind price action, with US business activity decelerating, while expectations for the Reserve Bank of Australia (RBA) to keep unchanged its interest rates at the upcoming monetary policy on Tuesday pressures the Aussie (AUD).

AUD/JPY Price Analysis: Technical outlook

From a daily chart perspective, the AUD/JPY is still upward biased, but given the nature of being used as a currency pair that reflects market sentiment, a risk-off impulse could shift the bias of the AUD/JPY. As long as the AUD/JPY remains above the Ichimoku cloud, the pair is upwards, but the Chikou Span, piercing May 2 candlestick chart at around 92.25, could trigger a sell signal, which could lower the price.

The Relative Strength Index (RSI) indicator is still bullish, but the three days Rate of Change (RoC) portrays that buying pressure is easing. Therefore, the AUD/JPY could aim toward the Tenkan-Sen Line at 91.46, as an initial target, in the near term, followed by the confluence of a support trendline and the Kijun Sen at 90.91.

Conversely, the AUD/JPY first resistance would be the four-month high at 92.66 before testing the YTD high at 92.99. A breach of the latter will expose the last year’s YTD high of 98.59.

AUD/JPY Price Action – Daily chart

- GBP/USD stays defensive after pushing back Cable bears the previous day.

- Softer US data fails to impress Pound Sterling bulls amid mixed concerns about BoE.

- UK’s higher inflation clues jostle with British growth fears to prod GBP/USD bulls.

- Absence of Fed talks, major UK data adds strength to cable pair’s sluggish move.

GBP/USD struggles for clear directions around 1.2435-40 amid early Tuesday in Asia, despite bouncing off a short-term key support line the previous day. In doing so, the Cable pair portrays the market’s indecision while also fails to cheer the downbeat US data amid mixed concerns about the Bank of England’s (BoE) next step.

On Monday, market players witnessed downbeat US statistics, as well as improved prints of the UK S&P Global/CIPS PMIs. However, the same initially underpinned the GBP/USD to rebound from a three-month-old rising support line before the recession woes and indecision at the BoE weighed on the Pound Sterling.

That said, US ISM Services PMI declined to 50.3 for May versus 51.5 expected and 51.9 prior whereas growth of the Factory Orders also deteriorated during the stated month to 0.4% versus 0.5% market forecasts and 0.9% previous readings. It should be noted that the final readings of S&P Global Composite PMI and Services PMI also marked softer figures for May.

On the other hand, final readings of the UK S&P Global/CIPS Services PMI and Composite PMI for May improved to 54.0 and 55.2 versus 53.9 and 55.1 initial expectations. Recently, UK BRC Like-for-Like Retail Sales growth slide to 3.7% YoY for May versus 5.2% prior. Furthermore, the latest survey from Barclays mention that the UK May Consumer Spending rose 3.6% YoY as higher food prices limit discretionary spending.

Following the data, Reuters said, “Recent data indicates previous BoE hikes are beginning to slow the UK economy, which could reignite UK recession fears and thus pressure more MPC members to vote for steady rates to help jumpstart the economy, removing the primary stimulus sterling strength.”

Elsewhere, US receding hawkish bets on the Federal Reserve (Fed) and concerns about the need for the US large banks to hold more capital to battle the landing crisis contrast with the policymakers’ ability to avoid the debt-ceiling expiration.

It should be noted that the latest political jitters in the UK, especially after the late May local elections, also prod the GBP/USD buyers.

Amid these plays, the US benchmark yields dropped on Monday while Wall Street closed in the red, with mild losses. That said, the US Dollar Index (DXY) dropped and reversed the early-day gains to end in the red with minor losses around 104.10.

To sum up, the inflation woes appear to lack the strength to keep the GBP/USD pair firmer as the market fears the UK recession and further challenges for the BoE hawks.

Moving on, a light calendar and the absence of the Fed talks keep the GBP/USD pair at the mercy of the risk catalysts.

Technical analysis

GBP/USD fades bounce off a three-month-old ascending support line, around 1.2375 by the press time, amid failure to cross a horizontal resistance zone comprising multiple levels marked since mid-April, close to 1.2545-50 at the latest.

- EUR/USD fades the week-start rebound amid sluggish oscillators.

- Failure to cross the key upside hurdles during previous week’s recovery lures Euro sellers.

- One-week-old ascending support line, 78.6% Fibonacci retracement limit short-term downside.

EUR/USD retreats towards 1.0700 amid the early hours of Tuesday’s Asian session after a volatile day. That said, the Euro pair initially cheered the downbeat US data before paring the gains and closing the day around the week-start levels.

That said, the major currency pair’s latest pullback could be linked to the sluggish RSI (14) line surrounding the 50.0 levels suggesting the continuation of a lower grind. On the same line could be the MACD signals which are bearish but losing the momentum strength of late.

As a result, the EUR/USD pair’s slow grind toward the south can’t be ruled out, which in turn highlights a one-week-old rising support line, close to 1.0675 at the latest, as immediate support to watch for the Euro sellers.

Following that, the 78.6% Fibonacci retracement level of the pair’s March-April rise, near 1.0635, will gain the EUR/USD bear’s attention.

Although the likely oversold RSI around 1.0635 will prod the Euro sellers around then, any further downside could make the pair traders vulnerable to refreshing the yearly low of around 1.0480.

Alternatively, a fortnight-long descending resistance line precedes the 100-SMA level, respectively near 1.0760 and 1.0770, limiting the short-term downside of the EUR/USD pair.

In a case where the Euro buyers remain in the driver’s seat past 1.0770, the 50% Fibonacci retracement level of the quote’s aforementioned upside, near 1.0805, will be in the spotlight.

EUR/USD: Four-hour chart

Trend: Further downside expected

- GBP/JPY fell to a daily low of 172.85 as it seems to be correcting overbought conditions.

- UK reported strong PMIs revisions.

- British yields to limit Sterling’s losses.

During Monday’s session, the Sterling Pound weakened across the board, trading in the 174.36 - 172.85 range and failing to capitalize on rising British bond yields following strong UK PMI revisions. On the other hand, the Japanese Yen traded mixed against its rivals and continues to gain traction on rumours of authorities from Japan intervening in the markets.

The UK reported strong PMI revisions, with eyes on the next BoE decision

According to the latest May reports by S&P Global/CPIS, the Composite Purchasing Managers' Index (PMI) was upwardly revised to 54 from the preliminary reading of 53.9. Likewise, the Services PMI was revised to 55.2 from 55.1.

As a reaction, the British bond yields saw gains across the curve while the British Financial Times Stock Exchange 100 Index (FTSE), indicating that markets seem to be waiting for more action from the Bank of England (BoE). In that sense, the 10-year bond yield increased to 4.26%, reflecting a gain of 1.13% on the day. Similarly, the 2-year yield stands at 4.49%, indicating an increase of 1.18%. The 5-year yield also saw an upward movement, reaching 4.21%, with a gain of 1.13% respectively.

On the other hand, as more interest rate hikes and stocks tend to be negatively correlated, the FTSE lost more than 0.1% following the release of the data. However, inflation and labour market data that will be released throughout June will continue to model the expectations for the following BoE interest rate decision and hence direct the movements of the GBP price dynamics.

Levels to watch

According to the daily chart, the GBP/JPY holds a neutral to bullish outlook for the short term. The bulls have lost some steam as buyers seem to be taking profits. In addition, the Relative Strength Index (RSI) despite getting rejected at the overbought threshold, stays flat in positive territory while the Moving Average Convergence Divergence (MACD) fell slightly to negative territory.

In case the buyers regain momentum, a move above the 173.50 zone would suggest a continuation of the bullish trend for the GBP/JPY, with the next resistances at the 173.95 zone and 174.00 level. On the other hand, immediate support is seen at the 172.40 level, followed by the psychological mark at 172.00 and the 171.80 area.

-638216011358063981.png)

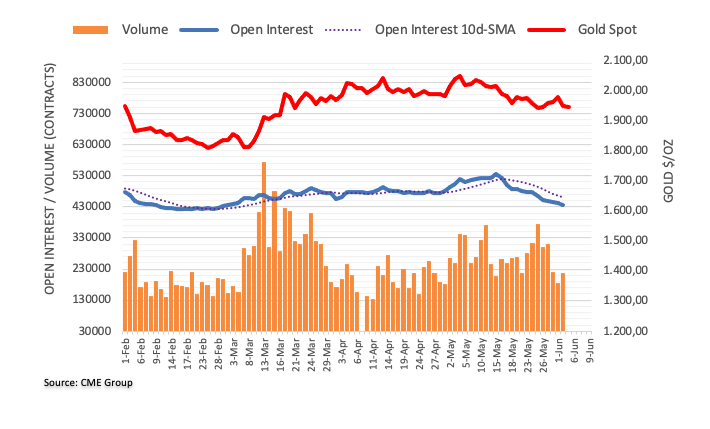

- Gold Price defends the week-start bounce off short-term key support confluence, seesaws of late.

- XAU/USD benefits from softer United States PMI data, Factory Orders amid downbeat US Dollar and Treasury bond yields.

- Risk catalysts eyed amid an unimpressive economic data line for the Gold traders.

Gold Price (XAU/USD) stays on the front foot around $1,961, after an upbeat start of the week, as the bullion traders seek more clues to extend the latest rebound during early Tuesday in Asia. That said the precious metal cheered downbeat United States statistics and dicey markets to regain upside momentum the previous day. Adding strength to the XAU/USD rebound was its inability to crack the short-term key support confluence surrounding $1, 940 (stated in the technical analysis).

Gold Price rises on downbeat US data, easing hawkish Federal Reserve bets

Gold Price began the week on a front foot, after snapping a three-week downtrend, as weak United States data weigh on the Federal Reserve (Fed) bets and the US Dollar on Monday. That said, On Monday, US ISM Services PMI declined to 50.3 for May versus 51.5 expected and 51.9 prior whereas growth of the Factory Orders also deteriorated during the stated month to 0.4% versus 0.5% market forecasts and 0.9% previous readings. It should be noted that the final readings of S&P Global Composite PMI and Services PMI also marked softer figures for May.

Following the data, the market’s bets on the Fed’s June rate hike dropped from around 80% in the middle of the last week to nearly 25%. The same could have joined an absence of the Fed talks to weigh on the US Treasury bond yields and the US Dollar. That said, the US Dollar Index (DXY) dropped and reversed the early-day gains to end in the red with minor losses around 104.10.

It should be noted, however, that International Monetary Fund (IMF) Managing Director Kristalina Georgieva suggested during the weekend that the Fed needs to do more to tame inflation, which in turn probed the Gold buyers.

China data, United States banking concerns also favor XAU/USD bulls

Apart from the softer US data and yields, upbeat statistics from China, one of the world’s biggest Gold consumers, also allowed the XAU/USD to remain firmer. On the same line were concerns about the US banks.

That said, China’s Caixin Services PMI matches 57.1 market forecasts for May versus 56.4 previous readings.

Elsewhere, chatters were making rounds that the large banks in the United States need to hold more capital to avoid the risk of default seemed to have dented the market sentiment. While portraying the same, Wall Street benchmarks closed in the red, which in turn joined downbeat US data and allowed the Gold price to remain firmer.

Looking forward, a lack of major data/events on Tuesday may help the Gold buyers to take a breather. However, growing pessimism among the Fed hawks can keep the XAU/USD bulls hopeful.

Gold Price technical analysis

Gold Price (XAU/USD) repeatedly bounces off a convergence of the 100-DMA and an upward-loping support line from early November 2022, around $1,940 by the press time.

Adding strength to the XAU/USD recovery expectations is the near-50.0 level of the Relative Strength Index (RSI) line, placed at 14, as well as an impending bearish signal on the Moving Average Convergence and Divergence (MACD) indicator.

Even so, the 50-DMA hurdle of around $1,990 and the $2,000 round figure challenge the Gold buyers before giving them control.

On the contrary, the Gold Price daily closing below $1,940 support confluence can quickly fetch the metal towards the $1,900 round figure.

In a case where the Gold Price remains bearish past $1,900, the early March swing high of around $1,860 and the yearly low marked in February near $1,804 will be in the spotlight.

Overall, the Gold price is likely to remain firmer unless breaking the $1,940 level.

Gold price: Daily chart

Trend: Further upside expected

- NZD/USD is firming into the 0.6070s in early Asia ahead of the RBA.

- US Dollar fell on Monday on a poor data outcome.

NZD/USD is trading away from the lows of Monday after a parabolic rally that occurred in the New York session. NZD/USD is starting the day in the 0.6070s as traders await the Reserve Bank of Australia´s meeting.

NZD/USD rallied on the back of a drop in the US Dollar after the weaker ISM services print. ´´The May ISM Services index fell 1.6pts to 50.3, below consensus of a lift to 52.4. That is the survey’s lowest reading since the initial onset of the pandemic, except for December last year which was affected by severe weather conditions,´´ analysts at ANZ Bank explained. ´´The print will undoubtedly fan expectations that the largest sector of economic activity may finally be responding to Fed tightening.´´

As for the US Dollar, the index cut early gains to trade little changed around 104 on Monday. The data dented the US Dollar that had otherwise enjoyed the Nonfarm Payrolls and a remarkable 339K jobs in May. However, the Unemployment Rate rose by 0.3 percentage points to 3.7% and hourly wage growth slowed. Around 80% of market participants expect the Fed to leave rates steady when it meets next week.

Additionally, the analysts at ANZ Bank also explained that a rate hike from the RBA today is a risk, and they think´´ the RBNZ will deliver two more hikes by August, so expect volatility given the market is hedging its bets 50/50 each way.´´

- USD/CHF takes a hit as weaker-than-expected US economic data spur recession fears, driving the Swiss Franc up.

- From a technical perspective, the USD/CHF pair is neutrally biased, awaiting a fresh catalyst for definitive market direction.

- Amid mixed signals from market oscillators, expectations of a hawkish Swiss National Bank may provide a catalyst for further USD/CHF downside.

USD/CHF slips after clashing with the 100-day Exponential Moving Average (EMA) at 0.9125, dropping below the 0.9100 mark, sponsored by a soft US Dollar (USD). Weaker-than-expected US economic data stirred recession fears amongst investors. Therefore, the Swiss Franch (CHF) rises, as shown by the USD/CHF pair trading at 0.9063, down 0.27%.

USD/CHF Price Analysis: Technical outlook

From a daily chart perspective, the USD/CHF is neutrally biased, waiting for a fresh catalyst that could give direction to the USD/CHF pair. Meanwhile, the USD/CHF is trapped on the upside by the 100-day Exponential Moving Average (EMA) at 0.9123; on the flip side, the 50-day EMA is at 0.9037.

In bullish territory, the Relative Strength Index (RSI) indicator aims downwards, while the 3-day Rate of Change (RoC), even though in bearish territory, climbs toward the neutral area. Mixed signals between oscillators might prevent traders from opening new long/short positions. But, expectations for a hawkish Swiss National Bank (SNB) could open the door for further downside.

The USD/CHF first support would be the 50-day EMA. A breach of the latter will expose the 20-day EMA at 0.9027, followed by the 0.9000 psychological support, before diving toward February 16, 2021, Low of 0.8926.

USD/CHF Price Action – Daily chart

The most significant event during the Asian session will be the Reserve Bank of Australia's meeting, where there may be an announcement of another interest rate hike. Ahead of the meeting, Japan will report on House Spending, ANZ will release the Commodity Price Index, and Australia will release Q1 Current Account Balance data.

Here is what you need to know on Tuesday, June 6:

On Monday, economic data from the US weighed on the US dollar, trimming Friday's gains. Last week's upbeat employment data had boosted the Greenback, but on Monday, the numbers came in the opposite direction and weighed on the currency. The Dow Jones lost 0.59%, and the Nasdaq declined 0.09%.

Data released on Monday showed that the US service sector continued to expand, albeit at a more moderate pace than in April, with the ISM Services PMI declining to 50.3 in May from 51.9 in April. This reading came in below the market expectation of 51.5. The Employment index dropped below 50, and the Prices Paid index fell from 59.6 to 56.2. The report presents evidence of easing inflation and softer activity, offering arguments for those Federal Reserve (Fed) officials who favor a pause at the June meeting. US yields dropped after the report and then trimmed losses. The DXY finished around 104.00, far from the 104.40 (June 5 high).

The Japanese yen was the best performer among majors, boosted by a decline in government bond yields and by a drop in equity prices in Wall Street. USD/JPY pulled back from near 140.50 to 139.20. Japan will release Overall Household Spending on Tuesday.

Economic data from the Eurozone came in below expectations (EZ PPI, Sentix Investor Confidence, and HCOB PMI). After the figures, European Central Bank President Christine Lagarde said that there is no clear evidence that underlying inflation has peaked. EUR/USD rebounded from 1.0680, boosted by a weaker US dollar, to 1.0720. On Tuesday, German April Retail Sales are due.

USD/CHF dropped, closing slightly above 0.9050. The Consumer Price Index rose 0.3% in May in Switzerland, and the annual rate dropped from 2.6% to 2.2%.

AUD/USD rose for the third consecutive day but again faced resistance at 0.6640. The Reserve Bank of Australia (RBA) will announce its decision on Tuesday. Market consensus points to the central bank remaining on hold with the cash rate at 3.85%, but it seems like a close call as analysts warn that a 25 basis points rate hike is possible.

Analysts at Rabobank wrote:

It is our house view that the RBA will keep policy steady on June 6. This would allow policy makers to absorb the Q1 GDP report which is due for release on June 7 and give them more time to assess the impact of the policy tightening to date. That said, we do expect more policy tightening later in the year and there are good reasons to suspect that this week’s policy decision will be a close call

NZD/USD rose modestly but maintained its position well above 0.6000. The ANZ Commodity Price Index is due on Tuesday, and the RBA's decision is important for the Kiwi.

USD/CAD moved sideways around 1.3440, looking steady ahead of Wednesday's Bank of Canada meeting. The Loonie had rallied earlier on Monday amid a rise in crude oil prices but then pulled back.

Oil prices finished flat after experiencing significant gains following Saudi Arabia's announcement of an extra cut in production in July. The WTI barrel finished under $72.00. Gold bounced from the $1,940 area to $1,965, boosted by the weaker US dollar and lower yields.

Bitcoin tumbled and dragged other cryptocurrencies down after the Securities and Exchange Commission sued Binance, alleging that the company operated an illegal exchange. BTC/USD lost 6% and dropped to $25,600.

Like this article? Help us with some feedback by answering this survey:

- AUD/USD is moving into the necklines of the W-formations.

- AUD/USD traders await the RBA key event.

AUD/USD is higher by some 0.18% on the day and met support on Monday that attracted buyers to test the prior day´s high of 0.6638. This has occurred as the market gets set for the Reserve Bank of Australia meeting today.

´´Following this week's data we now expect the RBA's target cash rate to peak at 4.35% with a 25bps hike with another in August,´´ analysts at TD Securities explained.

´´Given the monthly April inflation print showed the Bank departing further from its Q2'23 trimmed mean f/c and the higher than expected Fair Wage Commission decision, there is now a strong case for the Bank to move sooner rather than later.´´

Meanwhile, analysts at Rabobank argued that while the market has already assessed that the risks of a RBA rate hike have risen, a policy move would likely result in upside pressure on AUD/USD.

´´Although the AUD may edge a little lower on a steady policy announcement, we would expect that the downside would be limited given our house view that the RBA will be leaving the door open to another rate hike later in the year,´´ the analysts explained.

That said, their expectation that the USD is likely to remain well supported in the coming months suggests that AUD/USD may struggle to break above the 0.66-0.67 area.

As for the US Dollar, the index cut early gains to trade little changed around 104 on Monday on the back of Factory Orders that rose 0.4% in April, well below what had been expected. Additionally, ISM Services PMI fell sharply to the lowest in five months in May.

The data dented the US Dollar that had otherwise enjoyed the Nonfarm Payrolls and a remarkable 339K jobs in May. However, the Unemployment Rate rose by 0.3 percentage points to 3.7% and hourly wage growth slowed. Around 80% of market participants expect the Fed to leave rates steady when it meets next week.

AUD/USD technical analysis

The W-formations are pulling the price into the necklines. There are targets set higher with the 0.6670s eyed.

- EUR/JPY lost ground on Monday’s session, but managed to remain above 149.00.

- Eurozone May PMIs were revised lower.

- The Euro finds support on ECB Lagarde’s hawkish comments.

The EUR/JPY retreated to the 149.70 regions at the start of the week while the Euro traded mixed against its major rivals following disappointing PMIs from the EU (European Union). On the other hand, the Japanese Yen, held strong against most of its rivals as the prospects of Japanese authorities intervening in the markets helps limit deeper losses for the JPY.

EU reported weak PMIs but Lagarde’s comments limit the Euro’s losses

The S&P Global and Hamburg Commercial Bank (HCOB) showed that de Composite PMI dropped to 52.8 vs the consensus of 53.3 and the preliminary reading of 53.3. In addition, the Services PMI was also revised downwards to 55.1 from 55.9. Other data showed that the Sentix Investor confidence for June, slid to -17 (MoM) falling short of the -9.2 expected. April’s Producer Price Index (PPI) was confirmed at -3.2% (MoM) matching the consensus.

On the other hand, the European Central Bank (ECB) president, Christine Lagarde's hawkish comments stating that underlying inflationary pressures remain high and there is no clear evidence of inflation peaking, limits the European currency losses. In addition, the euro is supported by rising German yields, indicating market expectations of proactive measures from the ECB to address inflation concerns. In that sense, the 10-year and 2-year bond yields saw more than 3% increases standing at 2.39% and 2.94% respectively.

Levels to watch

Technically speaking, the EUR/JPY holds a neutral to bullish outlook for the short term as the bulls are struggling to maintain their dominance, but technical indicators are still favourable, suggesting that the market may still have some upside potential. The Relative Strength Index (RSI) remains above its midline while the Moving Average Convergence Divergence (MACD) turned somewhat flat.

In case the EUR/JPY exchange rate continues to gain traction, the following resistance line up at the 149.80 zone followed then by the 150.00 psychological area and the 150.50 level. On the other hand, the 20-day Simple Moving Average (SMA) at 149.05 level remains the key support level for the pair. If broken, the 148.50 area and 148.00 zone could come into play.

-638215918766829049.png)

- USD/MXN falls close to 0.50% amid declining US bond yields, on US recession fears.

- Despite an unchanged interest rate from the Mexican central bank, the Mexican Peso teeters towards year-to-date lows.

- USD/MXN is downward biased, potentially testing the current YTD low and the 2016 yearly low, suggesting bearish market sentiment.

USD/MXN drops close to 0.50% as the week begins, undermined by falling US bond yields, courtesy of mixed data, even though last week’s job report in the United States (US) cemented the case for one more rate hike by the US Federal Reserve (Fed). The Mexican Peso (MXN) threatens to fall toward new year-to-date (YTD) lows, albeit the central bank of Mexico held rates unchanged at its last meeting. The USD/MXN is trading at 17.4629 after hitting a high of 17.5971.

USD/MX pair weakens as US bond yields fall, concerns over potential US recession mount as further rate hikes by the Fed hinted

Wall Street is trading with losses as market sentiment deteriorated, as data from the Institute for Supply Management (ISM) revealed that service business activity remains in expansionary territory but slowing down. That, alongside a contractionary figure in manufacturing, sparked fears of an upcoming recession in the United States. Another piece of the puzzle added to recessionary anxiety is that Factory Orders released by the US Census Bureau weakened from 0.6% in April to 0.4% in the last month, excluding transportation, improved from a -0.7% drop to -0.2% in March.

Consequently, the greenback remains under pressure, as shown by the US Dollar Index (DXY). The DXY, a basket of six currencies that measures the performance of the USD, drops 0.04%, down at 103.995, weighed by falling US bond yields.

Hence, the USD/MXN has fallen from around the 17.59s area, even though that consumer confidence in Mexico was 44.4 in May. Contrarily, gross fixed income climbed 0.5% in March from February, as revealed by the Instituto National de Estadistica, Geografia e Informatica (INEGI) on Monday.

USD/MXN Price Analysis: Technical outlook

USD/MXN remains downward biased, though consolidated at around the 17.60/17.40 figure, during the last six trading days, unable to reclaim the 20-day Exponential Moving Average (EMA) at 17.6896, which could exacerbate a rally toward the 50-day EMA at 17.8995, ahead of re-testing the 18.00 handle. USD/MXN path of least resistance is downward and might test the current YTD low of 17.4238. A breach of the latter will expose the 2016 yearly low of 17.0509 before diving to 17.0000.

- USD/CAD bulls 38.2% ratio as first stop.

- Beyond daily resistance, bulls eye the1.3560s.

USD/CAD is been in the hands of the bulls at the start of the week while the yield on benchmark government debt climbed and despite a surprise in the US economic data front. Nevertheless, the technical outlook remains bullish as for the following analysis:

USD/CAD daily chart

The market swept the equal lows and subsequently, bulls moved in at a discount at the end of the three-day drop. This has occurred while an M-formation has been left on the charts. The bulls look to the Fibonacci scale whereby the 38.2% ratio meets with the prior structure and offers a compelling target for the bulls.

USD/CAD H1 chart

On the hourly chart, The price is sideways and bulls need to get above 1.3460 to break the resistance structure. In doing so, there are prospects of a move all the way through the 38.2% ratio into the 1.3560s.

- Gold bears got rejected at the 100-day SMA at $1,940.

- US Service PMIs from ISM and S&P Global came in weak in May.

- US bond yields decline across the board following the disappointing data.

During Monday’s session, Gold price gained bullish momentum and reached the $1,960 level after bottoming at the 100-day Simple Moving Average at the $1,940 zone. This increase was triggered by the release of disappointing ISM Services PMI data for May, which fueled a US Dollar sell-off on the back of failing US bond yields.

US yields decline across the board after disappointing US data

The US Institute for Supply Management (ISM) reported a Service PMI of 50.3 in May, falling short of the expected 51.5 and down from 51.9 the previous month. Furthermore, the S&P Global Composite final estimate for the same month declined to 54.3, lower than the anticipated 54.5, following the previous reading of 55.1. Meanwhile, the final revision of the service sector PMI came in at 54.9, slightly lower than the preliminary reading of 55.1.

Following the release, investors are perceiving a stronger case of a no-hike by the Federal Reserve (Fed) in the June 13-14 meeting. In that sense, the CME FedWatch Tool indicates there is a higher likelihood (77%) of the Fed not raising interest rates in their upcoming June, with expectations of maintaining the target rate at 5.25%.

Those dovish bets on the Fed were reflected in the drop of the US bond yields. The 10-year bond yield is trading at 3.67%, while the 2-year yield stands at 4.50% and the 5-year yield sits at 3.85%. As the US bond rates could be seen as the opportunity cost of holding the non-yielding gold, the yellow metal gained traction.

Levels to watch

According to the daily chart, the XAU/USD holds a neutral short-term outlook as the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) suggest that the sellers are struggling to maintain their dominance while the bulls are starting to gain momentum. Both indicators remain in negative territory but hint at bearish impulse exhaustion.

If the XAU/USD continues to move higher, the next resistances to watch are at the $1,960 zone, followed by the 20-day Simple Moving Average (SMA) at $1,977 and the $1,990 area. On the other hand, supports are seen at the 100-day SMA at $1,940, and then the $1,930 and $1,920 zones.

-638215885220520442.png)

- The oil price is on the backside of the trend and this leaves the outlook meanwhile bullish.

- WTI bulls are lurking within the Fibonacci scale.

Crude prices jumped today after Saudi Arabia said it would cut its crude production by -1.0 million bpd starting in July. However, weaker-than-expected global economic news raised concerns about energy demand, and crude prices fell back from their best levels. WTI is trading back to $74.50 and within the day´s range of between $74.92 and $72.07 the low. The following illustrates the technical outlook at this juncture:

WTI daily chart

The double bottom is a bullish feature on the longer-term charts with the price coiled within a falling bullish wedge formation.

WTI H1 chart

The price has pulled back into the gap but remains on the backside of the prior bearish trendline. This leaves scope for a move up from within the Fibonacci scale in due course.

- XAG/USD reclaims the 100-day EMA at $23.47 after dipping to a daily low, showcasing a subtle comeback.

- Despite the recovery, the market remains neutral to downward biased as XAG/USD fails to reconquer the April 25 daily low.

- Technical indicators suggest a battle between sellers and incoming buyers, hinting at volatility in the XAG/USD market.

XAG/USD stages a comeback though it remains slightly below its opening price, reclaimed the 100-day Exponential Moving Average (EMA) at $23.47 after hitting a daily low of $23.25. At the time of writing, XAG/USD exchanges hands at $23.55, down 0.14%

XAG/USD Price Analysis: Technical outlook

From a daily chart perspective, the XAG/USD is neutral to downward biased, as price action has failed to reconquer the April 25 daily low of $24.49, which could pave the way for further upside. In addition, the Relative Strength Index (RSI) indicator at bearish territory suggests that sellers are in charge, while the 3-day Rate of Change (RoC) indicates that buyers are moving in, cushioning the XAG/USD’s fall.

For a bearish resumption, XAG/USD must fall below the 100-day EMA at $23.47 to force a downward move to the $23.00 figure. A breach of the latter will expose the 200-day Exponential Moving Average (EMA) at $22.86.

Conversely, if XAG/USD buyers reclaim the 20-day EMA at $23.76, a rally toward the $24.00 is on the cards. But on its way north lies the 50-day EMA at $23.89.

XAG/USD Price Action – Daily chart

- NZD/USD jumped to its highest level since May 26 around 0.6085 after bottoming at November lows last week

- US ISM Services PMI fell to 50.3 in May.

- S&P Global Composite PMI retreated to 54.3.

The NZD/USD traded with gains at the beginning of the week near 0.6070, fueled by poor economic data from the US, which sparked a US Dollar sell-off. In reaction to the data, markets are perceiving a stronger case for the Federal Reserve (Fed) not hiking rates in the upcoming meeting on June 13-14 making the US bond yields decline.

US bond yields decline following weak economic data

The US Institute for Supply Management (ISM) Service PMI came in at 50.3 in May vs the 51.5 expected and decelerated from its previous figure of 51.9. In addition, the S&P Global Composite final estimate for the same month slid to 54.3 vs the 54.5 expected from the last reading of 55.1. Meanwhile, the service sector PMI final revision printed at 54.9 vs the preliminary reading of 55.1.

Following the disappointing data, US bond yields have declined throughout the yield curve. The 10-year bond yield has fallen to 3.69%. Similarly, the 2-year yield stands at 4.48%, while the 5-year yield sits at 3.83%, which weighs on the US Dollar.

According to the CME FedWatch Tool, investors are currently assigning a 77.10% probability to the Federal Reserve maintaining the target rate at 5.25% and not implementing an interest rate hike in the upcoming June 13-14 meeting. However, it is worth highlighting that the Fed's primary objective of achieving full employment and price stability remains steadfast. As a result, the release of the May Consumer Price Index (CPI) on June 13 will play a crucial role in shaping the FOMC's (Federal Open Market Committee) expectations and considerations for future interest rate decisions and hence impacting the US Dollar price dynamics.

Levels to watch

Technically speaking, the NZD/USD maintains a neutral to a bearish outlook for the short term, as per indicators on the daily chart. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD), despite standing in negative territory, show a loss of momentum, suggesting that sellers seem to have run out of steam.

On the upside, upcoming resistance for NZD/USD is seen at the daily high of 0.6085, followed by the psychological mark at 0.6100 and June 2 high around 0.6115. On the other hand, if the Kiwi retakes the downside, immediate support levels are seen at the daily low at 0.6040, followed by the psychological mark at the 0.6000 level and the cycle low at 0.5985.

- GBP/USD rate hovers above the 1.2400 mark after the last week’s USD boost from stronger-than-expected jobs data.

- US economic indicators reveal a mixed story, with weakening factory orders and a fall in Non-Manufacturing PMI.

- UK outpaces expectations with S&P Global Services and Composite PMIs, adding pressure on the Bank of England to address inflation concerns.

GBP/USD trims some of its losses but remains trading below its opening price; after the latest week, robust jobs reports boosted the American Dollar (USD), but Monday’s agenda capped the USD gains. Therefore, the GBP/USD is exchanging hands at 1.2440, 0.04% below its opening price but higher than the day’s low of 1.2368.

GBP/USD slashes early losses on weakening US factory orders and falling Treasury bond yields, limiting US Dollar gains as the UK PMI beats estimates

Last week, the US Bureau of Labor Statistics (BLS) revealed May’s data, showing the creation of more than 300K jobs, thought flashed the Unemployment Rate at 3.7%, sought by the US Federal Reserve (Fed), as a sign the economy is cooling and unexpectedly boosted the US Dollar (USD), as the GBP/USD retreated last Thursday¿s gains.

But on Monday, the story is different as Factory Orders in the US weakened, from 0.6% to 0.4% in May, less than estimations. Core Orders, excluding transportation, plummeted 0.2% but improved compared with March’s 0.7% drop. At the same time, the Institute for Supply Management (ISM) revealed that the Non-Manufacturing PMI fell to 50.9 from April’s 51.9, portraying that the economy is weakening.

After the data was released, the greenback weakened, as shown by the US Dollar Index (DXY), which tracks the buck’s value vs. a basket of peers. The DXY d down 0.09%, at 103.947, failing to crack the 104.000 mark, weighed by falling US Treasury bond yields. The US 10-year Treasury bond yield drops two basis points, at 3.677%.

On the UK front, the S&P Global Services and Composite PMIs beat estimates, with the Services Index registering a 55.2, exceeding forecasts of 55.1, though less than April’s 55.9. However, price input pressures rose the most in three months, with wages being the main reason. That would keep the Bank of England (BoE) pressured to deliver further tightening as inflation proves to be stickier than expected.

GBP/USD Price Analysis: Technical outlook

Given the fundamental backdrop, the GBP/USD is neutral to upward biased. In fact, today’s price action forming a gravestone doji or a hammer would put the 1.2500 figure into play. Still, traders must reclaim the 20-day Exponential Moving Average (EMA) resistance at 1.2442, followed by 1.2450. Once cleared, that could pave the way towards 1.2500. Conversely, the GBP/USD first support would be the 1.2400 figure, followed by the current week’ slow of 1.2368.

- Euro rises on weakening US factory orders and a mixed ISM reading, with EUR/USD trading above the opening price.

- Wall Street displays mixed sentiment as fears of recession loom following 7th straight month of contracting Manufacturing PMI.

- Hawkish comments from ECB officials, boost the Euro against the backdrop of a sluggish US economy.

EUR/USD erases some of its previous losses, sponsored by weaker orders in factories in the United States (US), alongside mixed ISM readings. European Central Bank President Christine Lagarde and other policymakers’ hawkish comments also lifted the Euro (EUR). The EUR/USD is trading at 1.0710, above its opening price by 0.01%.

Factory orders in the US falter while European Central Bank hints at continued interest rate hikes, sending the EUR/USD higher

Market sentiment is fragile, as shown by Wall Street trading mixed. Factory Orders in the United States slowed down in April, from 0.6% in the prior month, to 0.4%, beneath expectations for a solid 0.8% figure. Excluding transportation, plunged -0.2%, a slight improvement from March -0.7% fall. That, alongside further economic data from the US, underpinned the EUR/USD, which gained 27 pips in the latest 50 minutes of trading, claiming the 1.0700 mark.

The Institute for Supply Management (ISM) revealed that the Non-Manufacturing PMI, also known as the Services PMI, dropped to 50.3 in May from April 51.9, clung to expansionary territory amidst a slowdown in orders. Given that the PMI decelerated, increased fears for a possible recession after the last week’s Manufacturing PMI contracted for the seventh straight month.

Meanwhile, the US Dollar Index (DXY), a measure of the buck’s value vs. a basket of currencies, pairs earlier losses at 104.060, positive by 0.02%, capping the EUR/USD’s rally amidst falling US Treasury bond yields. The US 10-year benchmark note rate sits at 3.693%, almost flat.

On the European front, business activity in May, particularly the S&& Global Services PMI, decelerated but offset the plunge in manufacturing activity. Meanwhile, ECB speakers crossed newswires, led by its President Lagarde, who said that the central bank would stop all reinvestments in APP. Lagarde added that although there are signs of moderation, “there is no clear evidence that underlying inflation has peaked,” told European lawmakers.

At the same time, her colleague Joachim Nagler added the ECB needs to keep raining rates beyond the summer. Money market futures have priced in a 25 bps rate hike by the ECB, contrarily to the US Federal Reserve (Fed), which is seen pausing in June, but if data proves them wrong, another interest rate increase is expected in July.

EUR/USD Price Analysis: Technical outlook

From a technical perspective, the EUR/USD is neutral to downward biased, though testes briefly the 200-day Exponential Moving Average (EMA) at 1.0687, though bounced for the third time. Nevertheless, the Relative Strength Index (RSI) and the 3-day Rate of Change (RoC) are bearish, suggesting sellers remain in charge.

Downside risks lie at the 1.0700 figure. Break below will expose the 200-day EMA, followed by the May 31 low of 1.0635. on the flip side, the EUR/USD first resistance would be the 100-day EMA at 1.0769, the 20-day EMA at 1.0788, and the 1.0800 figure.

- US Dollar weakens across the board following lower-than-expected ISM Service PMI.

- US yields decline sharply after data, benefiting the Yen.

- USD/JPY extends reversal from six-day highs.

The USD/JPY experienced a sharp drop below 140.00 after the release of US economic data that weighed on the US Dollar. Within a few minutes, the pair lost more than 50 pips, reaching a fresh daily low at 139.25. It remains near the lows, under pressure.

Data triggers more losses in USD/JPY

The May S&P Global Services PMI was revised down from 55.1 to 54.9. More importantly, the ISM Services PMI for May came in at 50.3, the lowest level since May 2020, falling short of expectations of 51.5 and below April's figure of 51.9. The Prices Paid Index also fell from 59.6 to 56.2, and the Employment Index dropped to 49.2, indicating contraction.

In addition, a separate report showed that Factory Orders rose by 0.4% in April, below the market consensus of 0.5%.

These figures triggered weakness in the US Dollar across the board. The US Dollar Index dropped from 104.30, hitting daily lows below 104.00. US Treasury yields also turned negative, with the 10-year sliding from 3.75% to 3.66% and the 2-year from 4.55% to 4.43%.

The rally in Treasuries boosted the Japanese Yen, which is also benefiting from the slide in equity prices on Wall Street. As a result, the yen is one of the top performers so far on Monday.

USD/JPY fails to hold above 140.00

The USD/JPY reached a high of 140.45 on Monday, which was the highest level it had seen since May 30th. However, it began to pull back and accelerated its descent after the release of US data. The pair was unable to maintain a level above 140.00.

On the 4-hour chart, the USD/JPY has fallen below its 20-period Simple Moving Average (SMA). Immediate support is at 139.20, followed by the 138.95/139.00 zone. If the pair continues to decline, attention will turn to last week's low at 138.40. A recovery above 139.60 could alleviate the bearish pressure.

Technical levels

- US ISM Services PMI edged lower in May.

- US Dollar Index retreated below 104.00 with the initial reaction.

The business activity in the US service sector continued to expand, albeit at a more moderate pace than in April, with the ISM Services PMI declining to 50.3 in May from 51.9 in April. This reading came in below the market expectation of 51.5.

Further details of the publication revealed that the Prices Paid Index edged lower to 56.2 from 59.6 and the Employment Index dropped to 49.2 from 50.8.

Commenting on the data, "there has been a pullback in the rate of growth for the services sector. This is due mostly to the decrease in employment and continued improvements in delivery times (resulting in a decrease in the Supplier Deliveries Index) and capacity, which are in many ways a product of sluggish demand," said Anthony Nieves, Chair of the Institute for Supply Management (ISM) Services Business Survey Committee."

"The majority of respondents indicate that business conditions are currently stable; however, there are concerns relative to the slowing economy," Nieves added.

Market reaction

The US Dollar lost its strength after this report and the US Dollar Index turned negative on the day slightly below 104.00 with the initial reaction.

- USD/TRY advances to the 21.30 region on Monday.

- Investors appears skeptics after the appointment of M. Simsek.

- Türkiye headline CPI rose below 40% YoY in May.

There seems to be no respite for the weakness of the Turkish lira. That said, USD/TRY clocked a new record high well north of the 21.0000 mark on Monday.

USD/TRY: Further upside looks likely

USD/TRY maintains its firm bullish bias for yet another session and this time breaks above the 21.0000 mark with marked conviction, as investors remain highly apathetic following the announcement of new members of Erdogan’s cabinet.

Recently appointed Treasury and Finance Minister M. Simsek said over the weekend that returning to "rational ground" is necessary to ensure predictability in the economy and emphasized that the new government's primary objective will be to enhance social welfare.

It is worth noting that the lira has already lost more than 14% since January.

In the docket, inflation figures in Turkey tracked by the headline CPI rose at an annualized 39.59% in May and 0.04% vs. the previous month. It was the first reading below 40% since December 2021. In addition, the Core CPI (CPI excluding energy, food, non-alcoholic beverages, alcoholic beverages, tobacco, and gold) rose 46.62% YoY.

What to look for around TRY

USD/TRY maintains its upside bias well in place, always underpinned by the relentless meltdown of the Turkish currency.

In the meantime, investors are expected to closely monitor upcoming decisions on monetary policy, particularly after President R. T. Erdogan named former economy chief M. Simsek as the new finance minister following the cabinet reshuffle in the wake of the May 28 second round of general elections.

The appointment of Simsek has been welcomed with optimism by market members in spite of the fact that it is not yet clear whether his orthodox stance on monetary policy can survive within Erdogan’s inclination to battle inflation via lower interest rates.

In a more macro scenario, price action around the Turkish lira is supposed to continue to spin around the performance of energy and commodity prices - which are directly correlated to developments from the war in Ukraine, broad risk appetite trends, and dollar dynamics.

Key events in Türkiye this week: CPI, Producer Prices (Monday) – Industrial Production (Friday).

Eminent issues on the back boiler: Persistent skepticism over the CBRT credibility/independence. Absence of structural reforms. Bouts of geopolitical concerns.

USD/TRY key levels

So far, the pair is gaining 1.70% at 21.2381 and faces the next hurdle at 21.3119 (all-time high June 5) followed by 22.00 (round level). On the downside, a break below 19.5366 (55-day SMA) would expose 19.2216 (100-day SMA) and finally 18.8743 (200-day SMA).

- EUR/GBP scales higher for the second straight day and recovers further from the YTD low.

- Hawkish remarks by ECB officials underpin the shared currency and remain supportive.

- The setup supports prospects for additional gains towards the 0.8670 support breakpoint.

The EUR/GBP cross gains positive traction for the second successive day on Monday and recovers further from a fresh YTD low, around the 0.8565 region touched last week. The cross maintains its strong bid tone through the mid-European session and is currently placed near a three-day high, around the 0.8625-0.8630 region.

The shared currency's relative outperformance comes amid the recent hawkish remarks by several European Central Bank (ECB) officials, backing the case for additional rate hikes in the coming months. In fact, ECB policymaker Boštjan Vasle said on Friday that more rate hikes are needed to get inflation to the 2% target as core inflation remains high and persistent. Separately, ECB Governing Council member, Gabriel Makhlouf noted that the central bank has not reached the moment where it can say let's now stop.

Adding to this, ECB President Christine Lagarde, speaking at the Hearing before the Committee on Economic and Monetary Affairs (ECON) of the European Parliament, reiterated that price pressure remains strong in the Euro area. Lagarde added that there is no clear evidence that underlying inflation has peaked and that wage pressures have strengthened further. This overshadows last week's softer Eurozone CPI figures and continues to underpin the Euro, which, in turn, acts as a tailwind for the EUR/GBP cross.

The British Pound, on the other hand, struggles to attract any buyers as the market already seems to have priced in the prospects for another interest rate hike by the Bank of England (BoE). This, in turn, favours bullish traders and backs the case for a further near-term appreciating move for the EUR/GBP cross. Hence, some follow-through strength back towards testing a strong horizontal support breakpoint, around the 0.8670 region, looks like a distinct possibility. The said area should act as a pivotal point for short-term traders.

Technical levels to watch

- Gold price is making efforts for recovery from $1,940.00 as the focus shifts to US Services PMI.

- After the release of downbeat Manufacturing PMI, weak service sector performance could propel volatility in the USD Index.

- The yields offered on 10-year US government bonds are holding gains above 3.74%.

Gold price (XAU/USD) has defended its downside after a fresh four-day low around $1,940.00 in the New York session. The precious metal is expected to deliver a power-pack action as the United States ISM agency is going to release Services PMI numbers for May.

After the release of the downbeat Manufacturing PMI last week, a downbeat performance from the service sector could propel volatility in the US Dollar Index (DXY). US factory activity reported a seventh straight contraction as firms are failing to cater to their fixed and working capital requirements amid higher interest rates by the Federal Reserve (Fed) and tight credit conditions by US regional banks.

According to the preliminary report, US Services PMI is seen declining to 51.5 vs. the prior release of 51.9. New Orders Index that conveys forward demand is seen advancing to 56.5 against the former release of 56.1.

At the press time, the USD Index has faced marginal pressure while attempting to cross the immediate resistance of 104.40. After the release of upbeat US Nonfarm Payrolls data, it is critical to discuss about interest rate policy from Fed. The investing community will get more clarity after getting inflation figures for May ahead.

Meanwhile, S&P500 are expected to open on a mildly bullish note. US equities are expected to continue Friday’s optimism amid consistent macros. The yields offered on 10-year US government bonds are holding gains above 3.74%.

Gold technical analysis

Gold price witnessed an intense sell-off after a mean-reversion move to near the 200-period Exponential Moving Average (EMA) at $1,977.32 on a four-hour scale. The precious metal is declining toward the key support plotted from March 22 low at $1,934.34.

The Relative Strength Index (RSI) (14) is hovering near the 40.00 threshold. Bearish momentum will get triggered on a breakdown into the 20.00-40.00 range.

Gold four-hour chart

- AUD/USD reverses an intraday dip on Monday, though lacks any follow-through buying.

- Bets for another 25 bps Fed rate hike in June underpin the USD and cap gains for the pair.

- Traders look to the US ISM Services PMI for some impetus ahead of the RBA on Tuesday.

The AUD/USD pair attracts some dip-buying near the 0.6580 area and climbs to the top end of its intraday trading range during the early North American session on Monday. The pair currently trades just above the 0.6600 mark and remains well within the striking distance of a nearly two-week high touched on Friday.

A private-sector survey showed on Monday that China's services activity picked up in May and raises hopes of a recovery in the world's second-largest economy. Adding to this, speculations that the Reserve Bank of Australia (RBA) could tighten its policy further lend some support to the China-proxy Aussie. The upside for the AUD/USD pair, however, seems limited, at least for the time being, as traders seem reluctant to place aggressive bets ahead of the RBA meeting on Tuesday. Apart from this, a strong follow-through US Dollar (USD) buying further contributes to capping the major.

In fact, the USD Index (DXY), which tracks the Greenback against a basket of currencies, builds on Friday's post-NFP goodish rebound from over a one-week low and continues gaining traction for the second successive day amid expectations for additional rate hikes by the Federal Reserve. In fact, the current market pricing indicates a 30% chance of another 25 bps lift-off at the end of a two-day FOMC monetary policy meeting on June 14. This remains supportive of a further rise in the US Treasury bond yields, which underpins the buck and holds back the AUD/USD bulls from placing fresh bets.

Heading into the key central bank event risk, the aforementioned mixed fundamental backdrop warrants some caution before positioning for an extension of the AUD/USD pair's recent recovery from the multi-month low touched last week. In the meantime, traders on Monday will take cues from the release of the US ISM Services PMI. This, along with the US bond yields, will influence the USD price dynamics and produce short-term trading opportunities around the major.

Technical levels to watch

While speaking at the Hearing before the Committee on Economic and Monetary Affairs (ECON) of the European Parliament in Brussels, European Central Bank (ECB) President Christine Lagarde reiterated that price pressure remain strong in the Euro area.

Additional takeaways

"Underlying inflationary pressures remain high."

"No clear evidence that underlying inflation has peaked."

"Wage pressures have strengthened further."

"Decisions will continue to be based on our assessment of the inflation outlook in the light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission."

"Our rate hikes are being transmitted forcefully to financing conditions."

"Full effects of our monetary policy measures are starting to materialise."

"Effects of monetary policy tightening on real activity and inflation can be expected to strengthen in the coming years."

Market reaction

EUR/USD showed no immediate reaction to these comments and was last seen losing 0.3% on the day at 1.0680.

- USD/CAD is oscillating in a narrow range around 1.3450 as the BoC policy comes under the picture.

- The upside in the Lonnie asset is restricted by upbeat oil prices while the downside is being supported by a solid US Dollar.

- The BoC is expected to keep interest rates steady at 4.5% as Canada’s inflation has been steadily declining.

The USD/CAD pair is consistently showing back-and-forth action around 1.3430 in the early New York session. The Loonie asset is struggling to deliver a decisive move as investors are shifting their focus toward the interest rate decision by the Bank of Canada (BoC), which will be announced on Wednesday.

S&P500 futures are showing nominal gains before the opening of the American session. The overall market mood is quite upbeat as the Federal government has successfully eradicated the case of a default by the United States economy.

The US Dollar Index (DXY) has registered a fresh day's high at 104.40. Investors are gung-ho for the USD Index as consistent higher additions of fresh payrolls in the US labor market is supporting hopes of the continuation of the policy-tightening spell by the Federal Reserve (Fed).

It is worth noting that the Loonie asset is inside the woods despite sheer strength in the USD Index, which indicates that the Canadian Dollar is also strong.

The trigger that has been supporting the Canadian Dollar is the upbeat oil prices after the announcement of fresh oil production cuts seldom by Saudi Arabia. Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, said on Sunday, “Saudi Arabia to make extra 1 million b/d output cut from July.” He further added the Kingdom will extend its 500k barrels per day (b/d) voluntary cut until the end of 2024.

Investors should note that Canada is the leading exporter of oil to the United States and higher oil prices are supporting the Canadian Dollar.

This week, the interest rate policy by the BoC will be keenly watched. BoC Governor Tiff Macklem is expected to keep interest rates steady at 4.5% as Canada’s inflation has been steadily declining. In April, Canada’s inflation was recorded at 4.4%.

US ISM Services PMI Overview

The Institute of Supply Management (ISM) will release the Non-Manufacturing Purchasing Managers' Index (PMI) - also known as the ISM Services PMI – at 14:00 GMT this Monday. The gauge is expected to come in at 51.5 for May, down a little from 51.9 in the previous month. Given that the Fed looks more at inflation than growth, investors will keep a close eye on the Prices Paid sub-component, which is anticipated to fall from 59.6 in April to 57.8 during the reported month.

How Could It Affect EUR/USD?

Ahead of the key release, the prospects for another 25 bps rate hike by the Federal Reserve (Fed) in June push the US Dollar (USD) higher for the second successive day and drag the EUR/USD pair back blow the 1.0700 mark. A stronger US ISM Services PMI, along with higher-than-expected Prices Paid Index, will reaffirm market expectations, which should provide an additional boost to the Greenback and pave the way for a further depreciating move for the major.

In contrast, any immediate market reaction to the disappointing headline print is more likely to remain limited amid a further rise in the US Treasury bond yields. This, in turn, favours the USD bulls and suggests that the path of least resistance for the EUR/USD pair is to the downside. That said, a generally positive risk tone could act as a headwind for the safe-haven buck and help limit deeper losses for the major, at least for the time being.

Eren Sengezer, Editor at FXStreet, offers a brief technical outlook and writes: “EUR/USD broke below the 20 and the 50-period Simple Moving Averages (SMA) on the four-hour chart and the Relative Strength Index (RSI) indicator on the same chart dropped below 50, reflecting the bearish bias in the short term.

Eren also outlines important technical levels to trade the EUR/USD pair: “The upper-limit of the descending regression channel aligns as immediate support at 1.0680. In case EUR/USD returns within that channel by confirming that level as resistance, 1.0650 (mid-point of the channel, end-point of the latest downtrend) aligns as strong support before bears could target 1.0600 (psychological level, lower-limit of the descending channel).”

“On the upside, a four-hour close above 1.0720 (50-period SMA) could discourage sellers. In that scenario, 1.0750 (Fibonacci 23.6% retracement level of the latest downtrend) and 1.0780 (100-period SMA) align as next hurdles,” Eren adds further.

Key Notes

• EUR/USD Forecast: Euro could stretch lower in case 1.0680 support fails

• EUR/USD remains offered and below 1.0700 ahead of data, Lagarde

• EUR/USD: Dollar attention to the Fed?

About the US ISM manufacturing PMI

The Institute for Supply Management (ISM) Manufacturing Index shows business conditions in the US manufacturing sector. It is a significant indicator of the overall economic condition in the US. A result above 50 is seen as positive (or bullish) for the USD, whereas a result below 50 is seen as negative (or bearish).

- GBP/JPY has extended its downside to near 173.58 amid solid hopes of a BoJ’s stealth intervention.

- BoJ Ueda is consistently pumping liquidity into the economy to keep inflation steadily above 2%.

- Higher food inflation and labor shortages have remained major catalysts behind sticky UK inflation.

The GBP/JPY pair has picked significant offers and has extended its reversal move to near 173.58 in the late European session. A fresh seven-year high made by the cross has been followed by profit-booking as the Bank of Japan (BoJ) is expected to make a stealth intervention in the currency market to provide some cushion to the Japanese Yen, which is facing the heat of expansionary monetary policy.

According to the latest Reuters report, bets against the Japanese Yen have risen to $8.6 billion equivalent, which was a similar level when Japan’s authorities intervened last year.

To keep Japan’s inflation steadily above 2%, BoJ Governor Kazuo Ueda is consistently pumping liquidity into the economy so that the overall demand can be improved. Japan’s inflation has been imported cost-push driven, which lacks the traits of remaining steady. Steady inflation should be fueled by solid overall demand and higher wages and for which BoJ Ueda has been maintaining an ultra-dovish policy.

Later this week, Japan’s Q1 Gross Domestic Product (GDP) will remain in the spotlight. As per the preliminary report, Thursday’s GDP data is expected to expand by 0.5% vs. prior expansion of 0.4% on a quarterly basis. Annualized Q1 GDP is seen steady at 1.6%.

The Pound Sterling has shown a clear exhaustion in the upside momentum despite the Bank of England (BoE) being bound to raise interest rates further to keep pressure on United Kingdom’s stubborn inflation. Higher food inflation and labor shortages have remained major catalysts behind sticky UK inflation for more than the past year.

Investors should note that BoE Governor Andrew Bailey has already raised interest rates consecutively 12 times and more interest rate hikes cannot be ruled out to bring down price pressures.

- EUR/USD resumes the downside following Friday’s tops.

- A deeper correction could revisit the 1.0630 zone.

EUR/USD adds to Friday’s marked pullback and drops to the 1.0680 area on Monday.

The pair remains well under pressure and the continuation of the selling bias should put a potential test of the May low at 1.0635 (May 31) back on the radar in the short-term horizon. If spot clears the 1.0600 support it could then open the door to a deeper decline to the March low at 1.0516 (March 15).

A deeper pullback to the 2023 low at 1.0496 (January 6) would likely need a sharp deterioration of the outlook, which appears not favoured for the time being.

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0503.

EUR/USD daily chart

- USD/CHF scales higher for the second straight day and draws support from a stronger USD.

- Bets for another 25 bps Fed rate hike lift the US bond yields higher and underpin the buck.

- A positive risk tone dents demand for the safe-haven CHF and also lends support to the pair.

The USD/CHF pair gains positive traction for the second successive day on Monday and maintains its bid tone heading into the North American session. The pair is currently placed just above the 0.9100 mark, with bulls awaiting a sustained move beyond the 100-day Simple Moving Average (SMA) before placing fresh bets.

The post-NFP US Dollar (USD) rebound from over a one-week low remains uninterrupted on the first day of a new week amid expectations that the Federal Reserve (Fed) could hike interest rates again to contain stubbornly high inflation. In fact, the current market pricing indicates around a 30% chance of another 25 bps lift-off at the next policy meeting on June 13-14 and the bets were reaffirmed by robust US monthly employment details released on Friday. This, in turn, remains supportive of a further rise in the US Treasury bond yields, which continues to underpin the Greenback and acts as a tailwind for the USD/CHF pair.

The Swiss Franc (CHF), on the other hand, is pressured by a generally positive tone around the equity markets, which tends to drive flows away from traditional safe-haven currencies. The market sentiment remains well supported by the latest optimism over the passage of legislation to lift the government's $31.4 trillion debt ceiling and avert an unprecedented American default. Adding to this, a private-sector survey showed on Monday that China's services activity picked up in May and further boosts investors' confidence, which, in turn, dents the CHF's safe-haven demand and lends additional support to the USD/CHF pair.

The markets, meanwhile, have pushed back their expectations for an imminent pause in the Fed's rate-hiking campaign to July and eased off on bets for rate cuts later in the year. This, in turn, favours the USD bulls and supports prospects for a further near-term appreciating move for the USD/CHF pair. A sustained move and acceptance above the 100-day SMA will reaffirm the positive outlook, setting the stage for an extension of the recent upward trajectory witnessed over the past month or so. Traders now look to the release of the US ISM Services PMI for some impetus and grab short-term opportunities on Monday.

Technical levels to watch

- GBP/USD has delivered a breakdown below 1.2400 as investors get hopeful for a hawkish Fed policy post robust US NFP.

- Considering the persistence of UK inflation, the BoE might fail to halve inflation by year-end as promised by UK PM Rishi Sunak.

- GBP/USD witnessed intense selling pressure after failing to surpass the 61.8% Fibo retracement at 1.2583.

The GBP/USD pair has slipped sharply below the round-level support of 1.2400 in the European session. The Cable is facing immense selling pressure as the US Dollar has been strengthened after robust payroll additions in the United States in May fetched interest rate hike bets into the picture.

Additions of fresh Employment in May were extremely solid despite the Federal Reserve (Fed) consistently raising interest rates and US regional banks have inculcated more filters into their credit disbursement mechanism to maintain their asset quality amid a turbulent environment.

The Pound Sterling is failing in holding its feet despite the Bank of England (BoE) being expected to raise interest rates further amid a tight labor market and persistent food inflation. Considering the persistence in United Kingdom inflation, BoE Governor Andrew Bailey might fail to halve inflation by year-end as promised by UK Prime Minister Rishi Sunak.

GBP/USD witnessed intense selling pressure after failing to surpass the 61.8% Fibonacci retracement (plotted from May 10 high at 1.2680 to May 25 low at 1.2308) at 1.2583. At the press time, the Cable dropped below the 23.6% Fibo retracement at around 1.2400. The asset has also surrendered the support from the upward-sloping trendline placed from May 25 low at 1.2308.

The Relative Strength Index (RSI) (14) is hovering near 40.00. A breakdown below the same would activate the bearish momentum.

Should the asset break below May 31 low at 1.2348, US Dollar bulls would drag the asset toward May 25 low at 1.2308. Slippage below the latter would expose the asset to April 03 low at 1.2275.

On the flip side, a confident break above May 16 high at 1.2547 will drive the Cable towards May 10 low at 1.2603 followed by May 10 high at 1.2680.

GBP/USD four-hour chart

- DXY adds to Friday’s gains well north of the 104.00 barrier.

- Further upside is seen revisiting the May top around 104.80.

DXY’s rebound picks up pace and tests 2-day highs past the 104.00 hurdle on Monday.

Considering the current price action, further advances could initially see the May top of 104.79 (May 31) revisited in the relatively near term. From here, the index could target the minor hurdle at the round level of 105.00 ahead of the crucial 200-day SMA, today at 105.56.

Looking at the broader picture, while below the 200-day SMA, the outlook for the index is expected to remain negative.

DXY daily chart

- EUR/JPY extends the rebound and revisits the 150.00 region.

- Further up emerges the late month tops just above 151.00.

EUR/JPY climbs further and reclaims the area beyond the key 150.00 barrier at the beginning of the week.

Further recovery appears a plausible near-term scenario. That said, a convincing move north of 150.00 should retest the weekly high at 151.07 (May 29) ahead of the 2023 top at 151.61 (May 2).

So far, further upside looks favoured while the cross trades above the 200-day SMA, today at 144.01.

EUR/JPY daily chart

- US Dollar preserves its strength at the beginning of the week.

- US Dollar Index stays in positive territory above 104.00.

- ISM Services PMI report for May could influence US Dollar's performance on Monday.

The US Dollar (USD) holds its ground to start the new week. The US Dollar Index (DXY), which tracks the USD's valuation against a basket of six major currencies, stays in positive territory above 104.00 after having gained more than 0.5% on the back of the upbeat May jobs report from the US on Friday.

In the second half of the day, the USD's valuation could be effected by the ISM's Services PMI report for May. Markets expect the data to reveal an ongoing expansion in the service sector's business activity, while forecasting another month of strong input inflation. It's also worth noting that the US Census Bureau will release the Factory Orders data for April.

Daily digest market movers: US Dollar builds on Friday's gains

- The monthly data published by the US Bureau of Labor Statistics (BLS) showed on Friday that Nonfarm Payrolls rose 339,000 in May. This reading surpassed the market expectation of 190,000 by a wide margin. April's reading of 253,000 also got revised higher to 294,000.

- Underlying details of the labor market report revealed that the Unemployment Rate climbed to 3.7% from 3.4% in the same period. The Labor Force Participation rate remained unchanged at 62.6%, while annual wage inflation, as measured by the change in Average Hourly Earnings, edged lower to 4.3% from 4.4%.

- Commenting on the US jobs report, "is the US economy experiencing a soft landing? According to the latest Nonfarm Payrolls, the job market is slowing down to a "Goldilocks level" – not too hot nor too cold," said FXStreet Analyst Yohay Elam. "For markets, it means ongoing growth but with lower inflation and interest rates. For the US Dollar, it means the path of least resistance is down."