- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

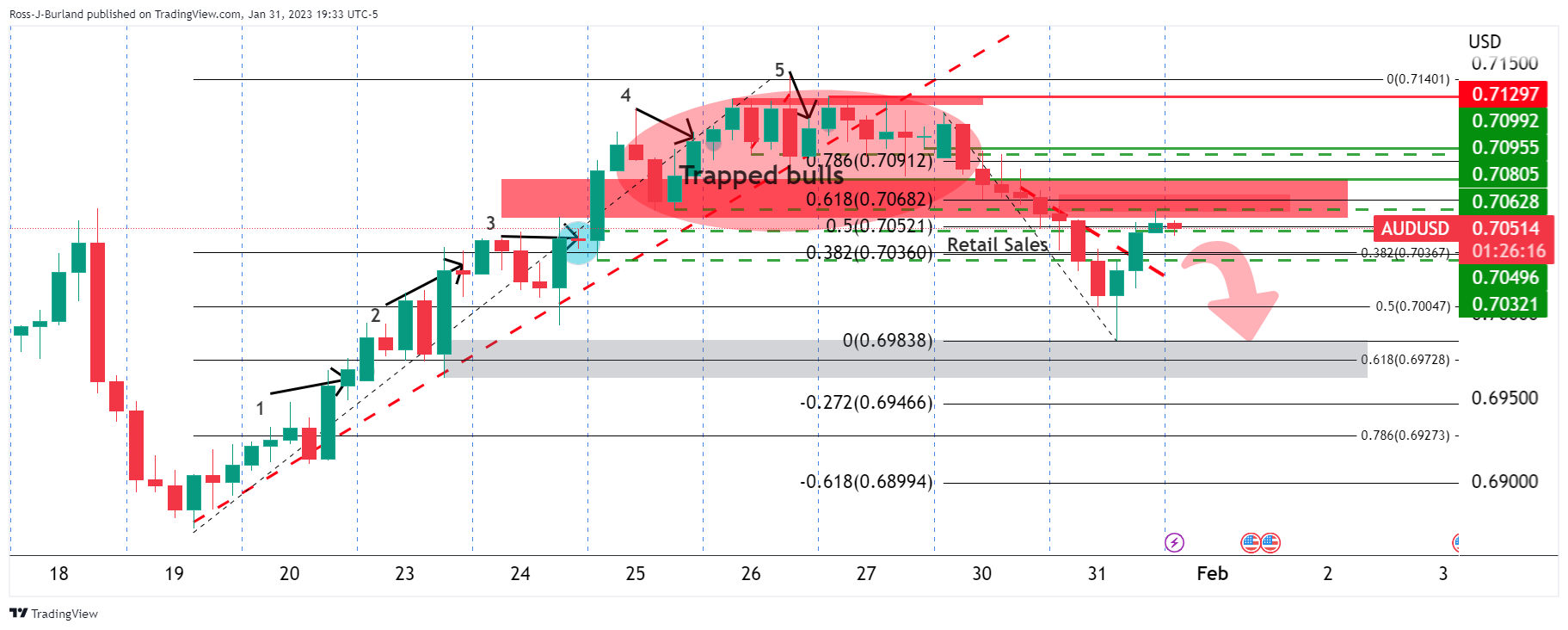

- AUD/USD bulls have taken the price into the 0.7150s and are on course for the 09.7200s.

- Central bank sentiment is underpinning the Aussie following the Federal Reserve.

AUD/USD is trading at 0.7144 and has ranged between 0.7128 and 0.7157 so far in the Asian session following the Federal Reserve rally after the central; bank had its rates raised by 25bps to a range of 4.50-4.75% and signalled further rate hikes are appropriate.

The statement acknowledged inflation has “eased somewhat” and dropped the references to supply/demand imbalances, high food and energy prices, and broader price pressures. However, Fed guidance is wisely erring on the side of caution. Nevertheless, the greenback was sold off with the Fed funds futures traders expecting the benchmark overnight interest rate to peak at 4.89% in June, before falling back to 4.39% by December. Nevertheless, the Fed's last "dot plot" in December showed that Fed officials expected the rate to rise above 5%.

With that being said, the greenback extended losses on Wednesday and fell to a nine-month low against a basket of currencies after Federal Reserve Chair Jerome Powell's dovish follow-up comments during the Q&A when he spoke of making progress in bringing down inflation pressures. He also noted progress on disinflation, which he said is in its early stages and said the Fed will continue to make decisions on a meeting-by-meeting basis. Powell repeated his code words for no pivot in 2023, but his acknowledgement of the start of the disinflationary process was taken as dovish by the markets and led to a decline in US treasury yields. Analysts at Rabobank said that they continue to think that inflation will be too persistent for the Fed to start cutting rates in 2023.''In fact, in our view the risks are still to the upside.''

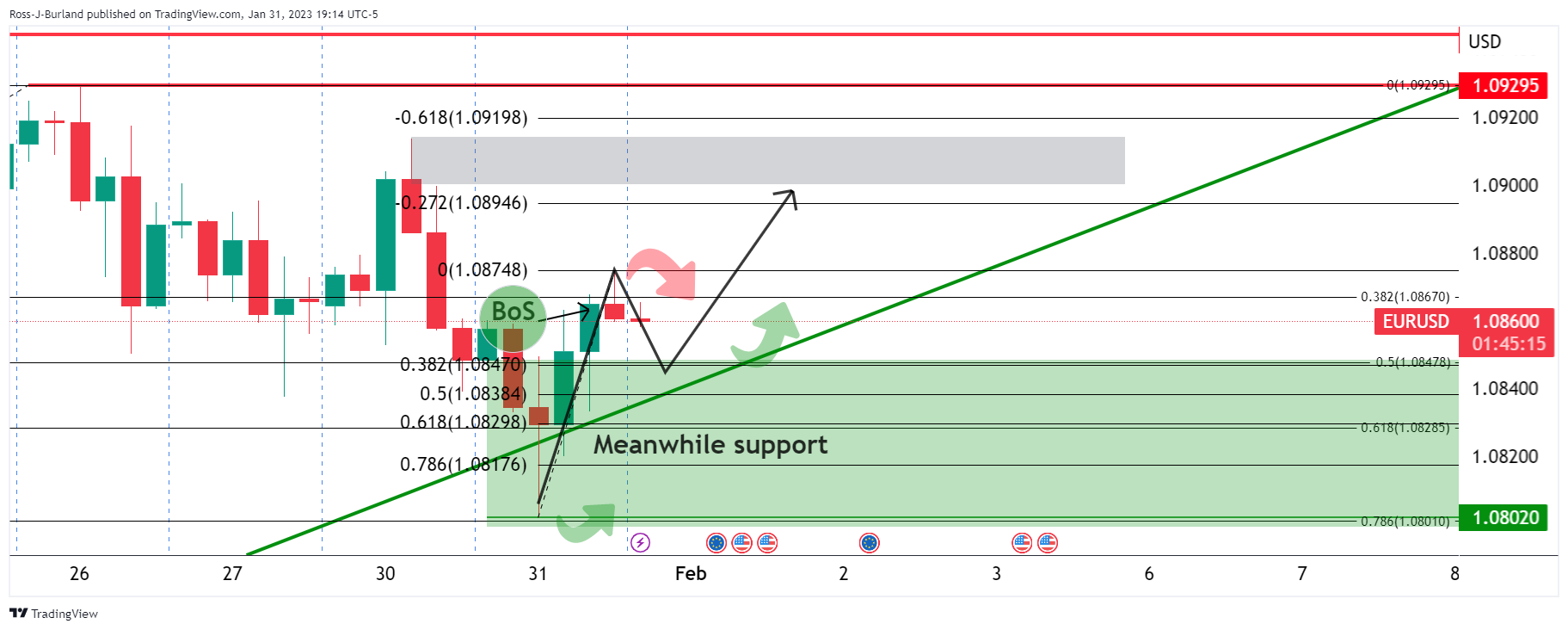

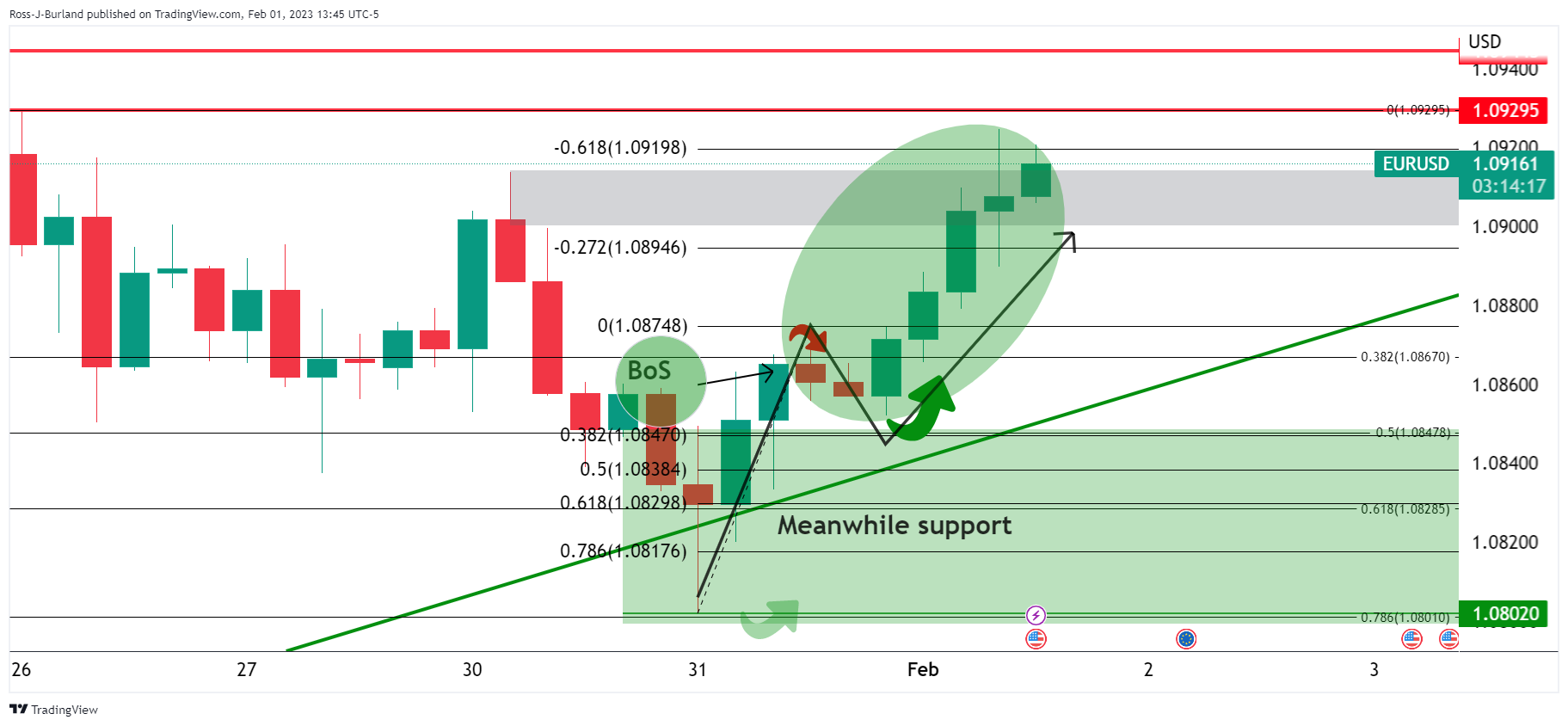

Meanwhile, looking at the Aussie, net AUD short positions were little changed for a second week having recently moved to their lowest level since October. Also, it is worth noting that the stronger-than-expected Australian Consumer Price Index inflation data has pushed back on recent speculation that the Reserve Bank of Australia could be nearing the peak of its interest rate cycle. '' The combination of the Fed and RBA sentiment is bullish for AUD and as the following technical analysis illustrates, there could be an advance towards 0.7280 on a break of 0.7250.

AUD/USD technical analysis

AUD/USD has broken structure around 0.7120/30 and is on the way towards the -272% ratio at 0.7206.

- US Dollar Index dropped the most in three weeks on Fed’s dovish hike.

- Fed matches 0.25% rate hike expectations but cited easing inflation to please DXY bears.

- Federal Reserve Chairman Powell’s readiness for rate cuts, if needed during late 2023 bolstered downside bias.

- Softer US data hints at further weakness but ECB, BoE could entertain traders.

US Dollar Index (DXY) holds lower grounds near 100.90 as traders lick their wounds near the lowest levels since April 2022 during Thursday’s Asian session. In doing so, the greenback’s gauge versus the six major currencies also portrays the market’s cautious mood ahead of the key central bank events and the US Nonfarm Payrolls (NFP).

DXY dropped the most in three weeks after the Federal Reserve’s (Fed) Monetary Policy Statement suggested that the inflation “has eased somewhat but remains elevated”. The same initially allowed the US Dollar bears to take entries even as the US central bank announced a 0.25% Fed rate hike while matching the market’s forecasts.

The US Dollar Index slump, however, took place after the Fed Chair Powell’s press as the policy hawk surprised markets by saying, “We can declare that a deflationary process has begun.” The policymaker also accepts the need for rate cuts during late 2023 if inflation comes down much faster. The policymaker also suggested that a couple more rate hikes are needed to reach it.

Also keeping the DXY bears hopeful were the mixed US data as ISM Manufacturing PMI dropped to the lowest levels since June 2020 while marking 47.4 figure for January, versus 48.0 expected and 48.4 prior. Further, the ADP Employment Change also declined to a one-year low with 106K the latest figure compared to the 178K market forecasts and the upwardly revised previous figure of 253K. On the contrary, JOLTS Job Openings rose to 11.012M in December, crossing 10.25M consensus and 10.44M prior readings.

Against this backdrop, Wall Street rallied and the US 10-year Treasury yields slumped the most in two weeks.

Having witnessed the Fed-inflicted losses, the DXY traders may wait for the monetary policy meetings of the European Central Bank (ECB) and the Bank of England (BoE). Also important to watch will be the US Preliminary Nonfarm Productivity for the fourth quarter (Q4), expected 2.4% versus 0.8% prior. Above all, Friday’s US jobs report for January will be crucial to follow for clear directions.

Technical analysis

A clear downside break of the May 2022 low of 101.30 keeps US Dollar bears hopeful of visiting the 100.00 psychological magnet.

- WTI crude oil licks its wounds around three-week low after falling the most in a month.

- Jump in EIA Crude Oil Stocks Change joined mixed clues surrounding global economic outlook to favor bears.

- OPEC+ left output policy intact, US Dollar slumped on Fed’s dovish hike.

WTI crude oil pares recent losses around the three-week low as it picks up bids to $77.10 during early Thursday in Asia. In doing so, the black gold price seems to cheer the broad US Dollar weakness during a quiet session, after falling the most since early January.

The energy benchmark’s previous slump could be linked to a surprise build in the inventories as the US Energy Information Administration said on Wednesday that the US crude oil and fuel inventories rose last week to their highest levels since June 2021 as demand remained weak. That said, the EIA Crude Oil Stocks Change for the week ended on January rose by 4.14M versus 0.376M expected and 0.533M prior.

While tracing the bearish inventories, the WTI crude oil ignores the fears of intact supply cuts from the major Oil producers. In its latest Joint Ministerial Monitoring Committee (JMMC) meeting, the Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, known collectively as OPEC+, left the oil output policy unchanged. That said, OPEC+ agreed to extend the output cuts of 2 million barrels per day, which was assented to in October 2022.

On the same line, the broad-based US Dollar weakness should have also favored the WTI crude oil buyers, but failed. That said, the US Dollar Index (DXY) dropped to a fresh low in late April 2022 after the US Federal Reserve (Fed) announced a dovish rate hike.

It’s worth noting that softer activity data from China Caixin Manufacturing PMI, US ISM Manufacturing PMI and the UK S&P/CIPS Global Manufacturing also weighed on the black gold prices.

Moving on, WTI traders should pay attention to the risk catalysts for fresh impulse. Also important will be the central bank meetings of the European Central Bank (ECB) and the Bank of England (BoE) as they both could affect the US Dollar and the Oil price as well. Furthermore, Europe’s discussions on the Oil price cap for Russian exports are also important to watch for clear directions.

Technical analysis

A daily closing below 50-DMA, around $77.75 by the press time, directs WTI crude oil towards a two-month-old support line, close to $75.25 at the latest.

- GBP/JPY prolonged its agony and dropped for the third time in the week below 160.00.

- GBP/JPY Price Analysis: Break below 159.50 exacerbated a fall towards 158.90, the week’s low.

The British Pound (GBP) failed to gain ground vs. the Japanese Yen (JPY) on Wednesday after the US Federal Reserve (Fed) hiked rates by 0.25%, a signal perceived by market participants as dovish. A reflection of that is Wall Street’s finishing with solid gains. At the time of writing, the GBP/JPY exchanges hand at 159.39 as the Asian session begins.

GBP/JPY Price Analysis: Technical outlook

Technically speaking, the GBP/JPY remains downward biased, as shown by the daily time frame. During the last six trading days, the GBP/JPY was range-bound within the 159.50-161.70 range, unable to gather direction upwards/downwards until Wednesday’s session, in which the pair clashed with the 20-day Exponential Moving Average (EMA) at 160.12, but retraced and dropped below 160.00.

Momentum indicators like the Relative Strength Index (RSI) turning bearish and the Rate of Chang (RoC) registering that sellers are gathering momentum would pave the way for further downside.

Therefore, the GBP/JPY first support would be the February 1 low of 158.90, after testing a one-month-old downslope resistance trendline, turned support. A breach of the latter and the next demand area would be the top of the previously mentioned trendline at 158.70, followed by the January 19 low at 157.56

On the other hand, the GBP/JPY could resume upwards once bulls reclaim the 20-day EMA at 160.12

GBP/JPY Key Technical Levels

- EUR/JPY is struggling to deliver a breakout of the Descending Triangle ahead of the ECB policy.

- The ECB might continue hiking interest rates despite the softened Eurozone HICP.

- Another 50 bps interest rate hike is expected from the ECB.

The EUR/JPY pair has struggled to surpass the critical resistance of 141.75 in the early Tokyo session. The cross is expected to remain sideways till the announcement of the interest rate decision by the European Central Bank (ECB).

On Wednesday, the preliminary headline Eurozone Harmonized Index of Consumer Prices (HICP) softened to 8.5% from the consensus of 9.0% due to easing energy prices. However, the ECB is expected to continue to remain hawkish as the road to price stability is far from over.

Analysts at Danske Bank expect ECB President Christine Lagarde to continue to sound very hawkish and signal that further rate hikes are coming, particularly giving guidance for another 50bps hike in March.

EUR/JPY is auctioning near the downward-sloping trendline of the Descending Triangle chart pattern on an hourly scale, which indicates a contraction in volatility. The downward-sloping trendline of the chart pattern is plotted from January 25 high at 142.29 while the horizontal support is placed from January 25 low at 140.75.

The 20-period Exponential Moving Average (EMA) at 141.40 is overlapping the EUR/JPY price, which indicates a consolidation ahead.

Also, the Relative Strength Index (RSI) (14) is still oscillating in the 40.00-60.00 range, which signifies an absence of a potential trigger.

For an upside move, the cross needs to surpass January 25 high at 142.29, which will drive the asset toward January 11 high at 142.61 followed by October 24 low at 143.72.

On the flip side, a break below January 25 low around 140.76 will be a breakdown of the chart pattern, which will drag the asset towards January 5 low at 140.14. A slippage below the same will expose the cross for more downside toward January 17 high at 139.62.

EUR/JPY hourly chart

-638108904932859037.png)

- NZD/USD crosses two-week-old resistance line to highlight trader’s bullish bias.

- Upbeat MACD, RSI adds strength to the run-up targeting fresh multi-month high.

- Convergence of 61.8% Fibonacci Expansion, June 2022 high appears a tough nut to crack for buyers.

- Sellers need 100-SMA breakdown to confirm further downside.

NZD/USD takes the bids to refresh the weekly high near 0.6520 during early Thursday’s Asian session. In doing so, the Kiwi pair extends its rebound from the 100-SMA to cross a downward-sloping resistance line from January 18.

Not only the successful recovery from the 100-SMA and the trend line breakout but bullish MACD signals and the upbeat RSI (14) also keep NZD/USD buyers hopeful.

As a result, the Kiwi pair is all set to poke the previous monthly high of 0.6530.

It’s worth noting, however, that a convergence of June 2022 high and 61.8% Fibonacci Expansion (FE) of its January 06-19 moves, near 0.6575, appears a strong resistance for the NZD/USD bulls to cross to keep the reins afterward.

On the flip side, pullback remains elusive unless the NZD/USD pair stays above the recent resistance-turned-support line near the 0.6500 round figure.

Even if the NZD/USD price drops below 0.6500 resistance-turned-support, the 100-SMA and the weekly low, respectively around 0.6440 and 0.6410, could challenge the pair’s further downside.

In a case where NZD/USD remains weak past 0.6410, the 200-SMA level near 0.6375 could act as the last defense of the bears.

NZD/USD: Four-hour chart

Trend: Further upside expected

- EUR/GBP stays on the front foot after rising the most in seven weeks.

- Euro cheers broad US Dollar weakness, pays little heed to softer Euro Area inflation.

- UK’s “Walkout Wednesday” and downbeat factory output add strength to the pair’s run-up.

- ECB, BoE both are likely to unveil 0.50% rate hike but the future of rate lifts will be the key to follow.

EUR/GBP bulls cheer the broad-based Euro (EUR) strength while refreshing the three-week high near 0.8900, taking rounds to 0.8890 by the press time of early Thursday’s Asian session. Additionally favoring the pair buyers could be the pessimism surrounding the UK workers’ strikes and downbeat factory output data. However, the cautious mood ahead of the monetary policy meeting of the European Central Bank (ECB) and the Bank of England (BoE) seems to probe the cross-currency pair’s further upside.

Also read: BoE Interest Rate Decision Preview: The last 50 bps hike but not the end yet

The Euro rallied the most in seven weeks against the British Pound (GBP) by spreading its broad-based gains from the US Dollar weakness. In doing so, the regional currency ignored downbeat inflation data at home. That said, the preliminary readings of the Euro area Harmonised Index of Consumer Prices (HICP) dropped to 8.5% YoY versus 9.0% expected and 9.5% prior. The Core HICP, however, came in unchanged at 5.2% compared to 5.1% market forecasts.

It should be noted that the US Federal Reserve’s (Fed) dovish hike could be held responsible for the US Dollar’s slump on Wednesday, which in turn allowed the EUR to rally against most counterparts.

Also fueling the EUR/GBP prices could be the mass strikes in the UK, as well as downbeat factory output. “Up to half a million British teachers, civil servants, and train drivers walked out over pay in the largest coordinated strike action for a decade on Wednesday, with unions threatening more disruption as the government digs its heels in over pay demands,” said Reuters.

On the other hand, the S&P Global/CIPS UK Manufacturing PMI confirmed a consecutive sixth monthly contraction in factory output with 47.0 figure versus 46.7 initial forecasts. “Weak demand from clients at home and abroad plus strong price inflation and a shortage of raw materials and staff all weighed on production. Brexit and port problems hurt exports while demand from China was particularly weak,” S&P Global said per Reuters.

On a broader front, Fed Chair Jerome Powell’s shift in favor of the rate cuts, if needed during late 2023, propelled bond-buying and equities, which in turn allowed the Euro to remain firmer ahead of the key ECB.

Moving on, market players will be more interested in the hints for slower rate hikes as both the central banks, namely the ECB and the BoE, are likely to announce 0.50% rate lift. It’s worth noting that the comparative economic soundness in the bloc and more hawkish comments from the ECB policymakers in the last couple of days favor the EUR/GBP bulls.

Also read: European Central Bank Preview: Lagarde needs to repeat her hawkish message

Technical analysis

Although the successful upside break of the 21-DMA, around 0.8815 by the press time keeps the EUR/GBP buyers hopeful, an upward-sloping resistance line from early November 2022, close to 0.8910 at the latest, appears a crucial hurdle for the pair traders to watch.

- USD/CHF has printed a fresh two-week low at 0.9070 as Fed scales down the policy tightening pace.

- The downbeat US Manufacturing PMI failed to impact the risk appetite theme.

- A spell of contraction in Swiss Real Retail Sales might force the SNB to avoid policy restrictions.

The USD/CHF pair has refreshed its two-week low at 0.9070 in the early Asian session. The downside pressure in the Swiss franc asset is built on a smaller interest rate hike announcement by the Federal Reserve (Fed). Fed chair Jerome Powell has stretched interest rates by 25 basis points (bps) to 4.50-4.75%, citing the requirement of maintaining policy significantly restrictive to address stubborn inflation.

The commentary from Fed’s Powell signifies that the Consumer Price Index (CPI) is clearly in a downtrend led by subdued consumer spending, a weak housing sector, and a slowdown in the United States' economic activities. However, the Fed will continue hiking interest rates to make monetary policy sufficiently restrictive as it needs more evidence to be confident inflation is on a downward path.

Despite Fed's hawkish guidance, the US Dollar Index (DXY) failed to hold the cushion of 101.00 and printed a fresh nine-month low at 101.64. S&P500 soared vigorously on a less-hawkish monetary policy by the Fed. The 500-US stock basket ignored the downbeat release of the United States ISM Manufacturing PMI (Jan). Manufacturing PMI dropped consecutively for the third time as higher interest rates by the Fed have resulted in lower consumer spending, which forced firms to avoid deploying full operational capacity. The economic data dropped to 47.4 lowest since May 2020 reading.

Apart from that, Automatic Data Processing (ADP) Employment data landed at 106K significantly lower than the estimates of 178K and the former release of 253K.

On the Swiss franc front, annual Real Retail Sales (Dec) data has contracted by 2.8% while the street was expecting an expansion of 2.6%. The economic data has been contracting consecutively for the past three months and is likely to force the Swiss National Bank (SNB) to avoid considering a restrictive stance on interest rates.

- USD/CAD licks its wounds after refreshing 11-week low.

- Bearish MACD signals, sustained trading below 21-DMA keeps sellers hopeful.

- 200-DMA, 1.3210 level act as the last defenses for the buyers.

USD/CAD jostles with a key support line after refreshing the multi-month low on the Federal Reserve’s (Fed) dovish hike, making rounds to 1.3290 during early Thursday morning in Asia. In doing so, the Loonie pair portrays sustained trading below the 21-DMA while also justifying the bearish MACD signals and downbeat RSI, not oversold.

It’s worth noting that an ascending trend line from June 2022, close to 1.3290 at the latest, challenges the pair sellers of late.

The major attention, however, should be given to the horizontal area comprising multiple levels marked since mid-July 2022 and the 200-DMA, between 1.3225 and 1.3210.

In a case where the USD/CAD pair stays weak below 1.3210, the 1.3200 round figure may act as an extra filter towards the south before directing prices towards the 1.3000 psychological magnet. It should be observed that June 2022 peak surrounding 1.3080 may offer an intermediate halt during the slump past 1.3200.

Meanwhile, USD/CAD recovery remains elusive until the quote remains below the 21-DMA hurdle of 1.3390.

Following that, the late January swing high near 1.3520 and the previous monthly top surrounding 1.3685 will be in focus.

Though, the USD/CAD bull-run needs validation from the December 2022 peak of 1.3705.

Overall, USD/CAD remains on the bear’s radar but the downside room appears limited.

USD/CAD: Daily chart

Trend: Limited downside expected

- The AUD/JPY cleared the 50/200/100-day Exponential Moving Averages (EMAs) on its way to 92.20s.

- AUD/JPY: A tweezers bottom candle chart pattern to pave the way for further upside.

The Australian Dollar (AUD) recovered some of its lost ground against the Japanese Yen (JPY) and rises, aligned with risk-perceived assets, bolstered by the US Federal Reserve (Fed) decision to raise rates by a quarter of a percentage, to 4.50% - 4.75% range, with the market’s perception of a dovish Fed. At the time of writing, the AUD/JPY exchanges hands at 91.99 after hitting a daily low of 91.21, above its opening price by 0.31%.

AUD/JPY Price Analysis: Technical outlook

After the Fed’s decision, the AUD/JPY pair rebounded off the day’s low at 91.21, as market sentiment remained sour ahead of the Fed’s meeting. Once the headlines crossed newswires and Powell’s presser began, the AUD/JPY edged up, clearing on its way north the 50, 200, and 100-day Exponential Moving Averages (EMAs), each at 91.31, 91.55, and 91.95, respectively.

As the New York session is about to end, an AUD/JPY close above the 100-day EMA will exacerbate a rally towards the January 26 swing high at 92.81. Once the spot price claims above the latter, the 93.00 figure would be next; after that, the December 13 daily high at 93.35 would be tested.

As an alternate scenario, the AUD/JPY first support would be the 200-day EMA at 91.55. Break below would send the pair sliding towards the 50-day EMA At 91.33, ahead of the February 1 low at 91.21.

AUD/JPY Key Technical Levels

- AUD/USD has displayed a vertical rally as the Fed has slowed the pace of policy tightening further.

- The Aussie asset has shifted above the 61.8% Fibo retracement at around 0.7100.

- Upward-sloping 20-EMA adds to the upside filters.

The AUD/USD pair printed a fresh seven-month high at 0.7145 in the late New York session. The Aussie asset displayed a perpendicular rally after the Federal Reserve (Fed) announced a 25 basis point (bps) interest rate hike to continue tightening monetary policy further to achieve price stability. Fed chair Jerome Powell is denied consideration of cutting rates this year as the central bank has a lot more to do to reach the 2% inflation target.

The US Dollar Index (DXY) is hovering around a fresh nine-month low at 100.64 and is expected to remain in the negative trajectory amid the risk appetite theme underpinned by the market participants.

AUD/USD has scaled above the 61.8% Fibonacci Retracement (placed from April 5 high at 0.7661 to October 13 low at 0.6170) at 0.7095, which supports the upside bias, placed on the daily scale. Upward-sloping 20-period Exponential Moving Average (EMA) at around 0.7000 is acting as major support for the Australian Dollar.

The Relative Strength Index (RSI) (14) is oscillating in the bullish range of 60.00-80.00, which indicates that the upside momentum has already been triggered.

For further upside, the Aussie asset needs to surpass June 9 high of around 0.7200, which will drive the asset toward June 7 high at 0.7247 followed by June 3 high at 0.7283.

On the contrary, a downside move below the psychological support of 0.7000 will drag the asset toward a 50% Fibo retracement at 0.6916. A slippage below the latter will drag the asset toward January 19 low at 0.6972.

AUD/USD daily chart

- EUR/USD bulls take a breather around multi-day top after rising the most in three months.

- Fed announced 0.25% rate hike as expected but Chairman Powell’s hint for rate cuts drowned US Dollar.

- Softer EU inflation, mixed US data failed to impress EUR/USD traders ahead of today’s ECB.

- ECB is likely announcing 0.50% rate hike, focus on easing of rate lifts.

EUR/USD bulls cheer the Federal Reserve’s (Fed) acceptance of easing price pressure, as well as Chairman Jerome Powell’s readiness for rate cuts if needed, by rising the most since November 2022 to poke the highest levels in 10 months, making rounds to 1.0990 at the latest. While the Fed-inspired rally appeared impressive, the major currency pair’s more moves appear to less likely ahead of the European Central Bank (ECB) monetary policy announcement, up for publishing during Thursday’s European session.

The Fed finally accepted that the inflation pressure in the US are abating of late while altering the Monetary Policy Statement wording to suggests that it “has eased somewhat but remains elevated”. The same initially allowed the US Dollar bears to take entries even as the US central bank announced a 0.25% Fed rate hike while matching market’s forecasts.

The greenback’s notable slump, however, took place after the Fed Chair Powell’s press as the policy hawk surprised markets by saying, “We can declare that a deflationary process has begun.” The policymaker also accepting the needs for rate cuts during late 2023 if inflation comes down much faster. The policymaker also suggested that a couple more rate hikes are needed to reach it.

It’s worth noting that the softer Eurozone inflation and the mixed US data previously challenged EUR/USD traders. That said, the preliminary readings of Euro area Harmonised Index of Consumer Prices (HICP) dropped to 8.5% YoY versus 9.0% expected and 9.5% prior. The Core HICP, however, came in unchanged at 5.2% compared to 5.1% market forecasts.

On the other hand, US ISM Manufacturing PMI dropped to the lowest levels since June 2020 while marking 47.4 figure for January, versus 48.0 expected and 48.4 prior. Further, the ADP Employment Change also declined to the one-year low with 106K be the latest figure compared to the 178K market forecasts and upwardly revised previous figure of 253K. On the contrary, JOLTS Job Openings rose to 11.012M in December, crossing 10.25M consensus and 10.44M prior readings.

Amid these plays, Wall Street rallied and the US 10-year Treasury yields slumped the most in two weeks.

Moving on, ECB is the key for the EUR/USD pair not only because it is up for announcing the 50 bps rate hike but also because the market doesn’t believe in the hawkish rhetoric of the policymakers and aim for hints of easy rates.

Also read: European Central Bank Preview: Lagarde needs to repeat her hawkish message

Technical analysis

A clear upside break of the seven-week high ascending trend line, close to 1.0960, directs EUR/USD towards March 2022 peak surrounding 1.1185.

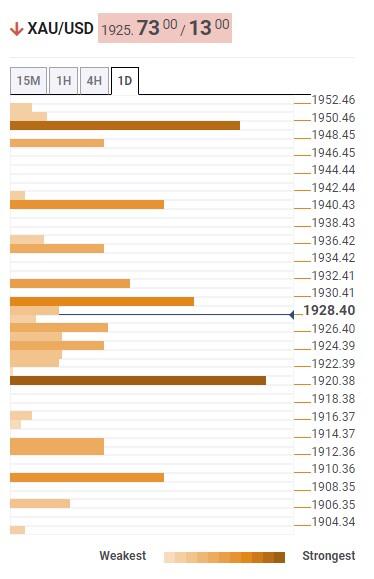

- Gold price jumps on dovish Federal Reserve tilt.

- The US Dollar drops as markets price in a pivot at the Federal Reserve.

Gold price shot higher to a fresh bull cycle high on the back of the Federal Reserve's dovish tilt that markets have priced in, smelling a 'Fed-pivot' around the corner, bullish for the Gold price.

At the time of writing, the Gold price is trading at $1,950 and has rallied from a low of $1,920.58 reaching as high as $1,954.64. The Fed terminal rate has fallen to under 4.9% amid Federal Reserve's chair Powell's comments that followed the eighth rate hike in a year. However, the Federal Reserve slowed its pace to a quarter of a point in a nod to an improved inflation outlook, underpinned by Federal Reserve's chairman, Jerome Powell, when he took questions from the press.

Federal Reserve Jerome Powell's key comments

"We can now say for the first time that the disinflationary process has started".

-

Powell speech: Very difficult to manage the risk of doing too little on rates

-

Powell speech: Disinflationary process is in early stages

-

Powell speech: History cautions against prematurely loosening policy

-

Powell speech: Well-anchored longer-term inflation expectations not grounds for complacency

-

Powell speech: Will likely have to maintain restrictive stance for some time

-

Powell speech: Very difficult to manage the risk of doing too little on rates

-

Powell speech: Policymakers did not see this as a time to pause

-

Powell speech: Will not be appropriate to cut rates this year according to our current outlook

Meanwhile, the Federal Reserve was retaining its prior language in the statement and Fed fund futures are still pricing in rate cuts this year, with the Fed funds rate seen at 4.486% by end of December, unchanged prior to the Fed decision. The March Federal Reserve meeting is priced in at 85% for 25 bps with the remainder at no change.

United States data supports higher Gold price

In data from the United States, The January ADP jobs report undershot expectations, with private sector jobs up 106k in January, versus 253k previously (and 180k expected) and this data will still cast some doubt over forecasts for a firm January Nonfarm Payrolls print. The US ISM Manufacturing index fell further in January, dropping to 47.4 (48.4 previously). That’s the third month in a row of contraction (below 50).

Gold price technical analysis

The Gold price is now carving out a fresh high on the front side of the dominant trendline. To the downside, bears need to get below $1,920 again to cement a bearish bias for the foreseeable future while bulls need to stay above $1,950 and then get over $1,980:

- GBP/USD has scaled firmly to near 1.2400 as Fed has announced a 25 bps interest rate hike.

- The USD Index has shifted below 101.00 for the first time in nine months amid a risk-on mood.

- To tame double-digit inflation, the BoE is set to announce a tenth consecutive interest rate hike.

The GBP/USD pair has displayed a juggernaut rally to near the round-level resistance of 1.2400 in the late New York session. The Cable has been infused with an adrenaline rush after the interest rate decision by the Federal Reserve (Fed) chair Jerome Powell met expectations. Fed chair Jerome Powell has pushed interest rates to the 4.50-4.75% range by announcing a 25 basis point (bps) hike as the central bank needs more evidence to be confident that inflation is on a downward path.

The US Dollar Index (DXY) has surrendered the critical support of 101.00 for the first time in the past nine months. The USD Index has refreshed its nine-month low at 100.64 despite the Fed having denied the speculation of pausing further restrictions on monetary policy this year. Meanwhile, S&P500 has settled Wednesday’s trading session on a bullish note. The 500-US stock basket recovered initial losses and ended the session with significant gains, portraying a significant improvement in the risk appetite of the market participants.

A smaller interest rate hike by the Fed has strengthened the demand for US government bonds, which led to a decline in the 10-year US Treasury yields to near 3.42%. The US Treasury yields nosedived despite the Fed clearing that the context of cutting interest rates this year is not in the picture.

Well, after sheer volatility in the FX domain inspired by Fed’s interest rate policy, investors are shifting their focus towards the interest rate policy by the Bank of England (BoE), which is scheduled for Thursday. BoE Governor Andrew Bailey looks set to announce a tenth consecutive interest rate hike to tame the double-digit inflation figure. According to a poll from Reuters, Investors are mostly betting on another half percentage-point increase to 4.0% and that Bank Rate will peak at 4.5% soon.

What you need to take care of on Thursday, February 2:

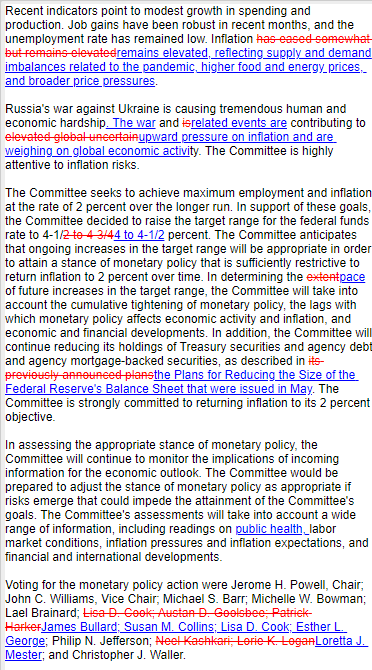

The US Dollar plummeted following the US Federal Reserve’s monetary policy decision. The central bank decided to hike its benchmark rate by 25 basis points (bps) as widely anticipated by market players. The statement showed that policymakers changed the wording on inflation, noting that it “has eased somewhat but remains elevated,” although there were no other relevant changes to the document. Furthermore, it noted that the Committee believes that “ongoing increases in the target range will be appropriate” to return inflation to 2%, hinting at more rate hikes in the docket.

US Fed Chair Jerome Powell started his statement by repeating the Fed is strongly committed to reaching its 2% inflation target. He also repeated that job gains have been robust, and the unemployment rate has remained low. However, he later added that, for the first time, “we can declare that a deflationary process has begun.” On the appropriate restrictive level, Powell said that a couple more rate hikes are needed to reach it. Finally, he ended up admitting that rate cuts could take place this year “if inflation comes down much faster.” Following the event, the US Fed Terminal Rate fell to under 4.9%, while the end-2023 Fed Funds Rate fell below 4.4%, as markets are still pricing in rate cuts for this year.

European inflation eased more than anticipated in January, according to preliminary estimates. The Harmonized Index of Consumer Prices (HICP) rose at an annualized pace of 8.6%. The news helped EUR/USD to overcome the 1.0900 threshold ahead of the US Federal Reserve’s announcement, with the pair ending the American session near a multi-month high of 1.1000 afterwards. The European Central Bank will announce its monetary policy decision on Thursday.

The GBP/USD pair struggled throughout the day to extend gains beyond 1.2300, as investors await the Bank of England monetary policy decision. The BoE is set to raise rates by another 50 basis points, while market players will be looking for clues about an easy pace of tightening from March on. It settled at 1.2370, up on the broad US Dollar weakness.

Commodity-linked currencies benefited from the positive tone of Wall Street, with AUD/USD hovering around 0.7140 and USD/CAD down to 1.3280. Finally, USD/JPY trades at around 128.90.

Spot gold soared and currently hovers at around $1,950 a troy ounce.

Crude oil prices edged lower as the OPEC+ meeting began, with no production changes on the agenda. A build in US inventories as reported by EIA also weighed on crude prices, as US stockpiles were up by 4.14 million in the week ended January 27. At the time being, WTI trades at around $76.90 a barrel.

Fed remains hawkish with 25 bps hike, how will Bitcoin price react?

Like this article? Help us with some feedback by answering this survey:

- NZD/USD pops on a troubled US Dollar hit by dovish tilt at the Fed.

- Markets smell a pivot coming and price in lower rates, weighing in the greenback.

NZD/USD has popped on the back of the market smelling a pivot at the Federal Reserve with the Fed terminal rate has fallen to under 4.9% amid chair Powell's comments. At the time of writing, NZD/USD is trading at 0.6500 and has rallied from a low of 0.6416 to a high of 0.6505 so far.

The Federal Reserve's dovish tilt, despite inflation, ''running very hot'', has weighed heavily on the greenback as traders move into risk-positive asset classes, such as commodities and stocks, supporting the high beta NZD. The Federal has increased interest rates for the eighth time in a year but slowed its pace to a quarter of a point in a nod to an improved inflation outlook. There was an initial bid in the greenback but it soon turned sour for the US Dollar bulls and the sell-off gathered pace as the cracks in Fed's chairman's, Jermoe Powell, comments started to reveal a dovish shift at the Fed.

Fed chair key comments

"We can now say for the first time that the disinflationary process has started".

-

Powell speech: Very difficult to manage the risk of doing too little on rates

-

Powell speech: Disinflationary process is in early stages

-

Powell speech: History cautions against prematurely loosening policy

-

Powell speech: Well-anchored longer-term inflation expectations not grounds for complacency

-

Powell speech: Will likely have to maintain restrictive stance for some time

-

Powell speech: Very difficult to manage the risk of doing too little on rates

-

Powell speech: Policymakers did not see this as a time to pause

-

Powell speech: Will not be appropriate to cut rates this year according to our current outlook

NZD now depends on RBNZ

Analysts at ANZ Bank said that ''with local markets firmly embracing “just” a 50bp RBNZ hike later this month, the NZD’s prospects are somewhat capped, but if the USD continues to crumble, that’s an offset. So there are plenty of balls in the air, and we remain attuned to volatility rather than directionality.''

''Yesterday’s NZ labour market report for Q4 still portrayed a labour market beyond ‘maximum sustainable employment’. However, the data were weaker across the board than the Reserve Bank of New Zealand expected back in November, with unemployment rising slightly, jobs growth slowing sharply, and wages (while still very strong) coming in below their expectation,'' the analysts added. ''Combine a softer employment report with Q4’s weaker-than-expected non-tradables inflation print last week, and we think there’s strong evidence that the RBNZ should downshift to a 50bp OCR hike at their 22 February meeting.''

- USD/JPY was rejected at the 20-day EMA and collapsed as the Federal Reserve increased rates by 25 bps.

- Federal Reserve officials stated that more increases would be appropriate in 25 bps increments.

- Powell’s disinflationary comments tumbled US Treasury bond yields and sent the US Dollar into a tailspin.

USD/JPY is plummeting sharply after the US Federal Reserve decided to slow down the pace of rate increases and hiked rates by 0.25% on their first monetary policy meeting of 2023. Therefore, the US 10-year Treasury bond yield is plunging more than ten bps toward 3.40% as the market responds to the Fed’s decision and Powell’s speech. At the time of writing, the USD/JPY exchanges hands in a volatile session at around 128.50-129.20.

Some remarks of the Federal Reserve Chair Jerome Powell

At the time of typing, the US Federal Reserve Chair Jerome Powell’s press conference continues, and the US Dollar continues to weaken across the board.

In his press conference, Powell said it would be premature to declare victory on inflation and said that the job is not fully done. He acknowledged that “it’s a good thing that disinflation so far has not come at expense of the labor market.”

Powell added that the Federal Open Market Committee (FOMC) has not decided on a terminal rate, and if data becomes weaker, then the central bank would become data-dependant. He added the Fed has no desire to overtighten, but if they do, they have the tools to work on it.

When asked about discussions in the meeting, Powell said they were talking about a couple more rate hikes to get to an “appropriately restrictive stance.”

Summary of the Fed’s monetary policy statement

On Wednesday, the Federal Reserve policymakers decided unanimously to hike rates by 0.25%, lifting the Federal Funds rate (FFR) at around 4.50% - 4.75%. Additionally, they pushed back against the market’s expectations for a Fed pivot and said additional rate hikes would be appropriate. Policymakers forward guided the market, adding that future rate hikes would be in 25 bps increments, dropping the reference to the “pace” of additional rate hikes.

Fed officials acknowledged that inflation has “eased somewhat but remains elevated.” Participants added that indicators point to modest growth in spending and production and commented that the labor market remains robust. Fed members stated, “in determining the extent of future rate hikes, it will take into account cumulative tightening, policy lags, and economic and financial developments.”

USD/JPY reaction to the headline

The USD/JPY 15-minute chart shows the pair tumbled below 129.50 and broke support levels, like the S2 and the S3 daily pivot points, each at 129.32 and 128.90. Then, it continued towards the day’s low at 128.54, reversing its course and reclaiming the S3 pivot point. Then the USD/JPY tested the 20-EMA at 129.21 before resuming its downtrend. The USD/JPY, the first support level, would be the S3 pivot at 128.90, followed by the daily low at 128.54, and then the S4 daily pivot at 128.48.

- USD/CAD breaks below 1.3300 momentarily as a dovish tilt at the Fed is priced in.

- Bears enthused by Fed's Powell arguing that the disinflationary process has started.

USD/CAD is under pressure and scoring fresh multi-day lows to 1.3274 so far from a high of 1.3379 and is down some 0.2%. The Federal Reserve's dovish tilt, despite inflation, ''running very hot'', has seen the market move out of the greenback and into risk-positive asset classes, such as commodities and stocks, supporting the Loonie.

pivot, with more rate hikes in the pipeline before a pause ''to get the job done.'' The central bank raised interest rates for the eighth time in a year but slowed its pace to a quarter of a point in a nod to an improved inflation outlook. However, the sell-off in the US Dollar gathered pace as the cracks in Fed's chairman's, Jermoe Powell, comments started to reveal a dovish shift at the Fed.

Jerome Powell's key comments

"We can now say for the first time that the disinflationary process has started".

Powell speech: Very difficult to manage the risk of doing too little on rates

Powell speech: Disinflationary process is in early stages

Powell speech: History cautions against prematurely loosening policy

Powell speech: Well-anchored longer-term inflation expectations not grounds for complacency

Powell speech: Will likely have to maintain restrictive stance for some time

Powell speech: Very difficult to manage the risk of doing too little on rates

Powell speech: Policymakers did not see this as a time to pause

Powell speech: Will not be appropriate to cut rates this year according to our current outlook

USD/CAD technical analysis

as the chart above shows, that was dran before the Fed, we have already seen the bears chip away at the 1.3305 structure, and this is technically already broken, exposing the 1.3220s and then the 1.3150s. On the upside, we have 1.3380s that guard the 1.3450/80s.

The move following the Fed is digging in at the structure in possible preparation for a downside extension.

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"My own assessment is that positive growth will continue but at subdued pace."

"The global picture is improving a bit."

"Labor market also remains very, very strong."

"As inflation comes down, sentiment will improve."

"State and local governments are flush, so that will also support."

"Lots of spending coming in construction pipeline."

"Those factors will support positive growth this year."

"We will look at incoming inflation reports."

"We will also be looking at the next Employment Cost Index report, yesterday's one was constructive as it showed wages coming down."

"As accumulated evidence on inflation comes in, that will be reflected in policy over time."

"Financial markets have a very different job to us, our focus is on bringing down inflation."

"We are strongly resolved that we will complete this task."

"Goods inflation has come down pretty fast."

"This is not a standard business cycle, it's unique."

"We can have no certainty in our forecasts."

"Will not be appropriate for us to cut rates this year according to our current outlook."

"If inflation comes down faster, then we will see it, will incorporate into policy."

- EUR/USD has rallied on the back of a less hawkish Fed Powell.

- The market is pricing in rate cuts, this is weighing in the greenback.

EUR/USD has rallied as the market jumps on a dovish tilt at the Federal Reserve, despite inflation ''running very hot''. However, the Federal Reserve chairman is speaking to the press and he has put no timeline on a pivot, with more rate hikes in the pipeline before a pause ''to get the job done.''

At the time of writing, EUR/USD is taking in the upper quarter of the 1.09 area with printing a high of 1.0985 made so far. The Euro rallied from a low of 1.0852 on the day, completing its daily ATR and bulls keep moving in with eyes on the 1.1000 psychological mark. The Fed terminal rate has fallen to under 4.9% amid chair Powell's comments:

Watch live: Fed Powell's presser

Fed Press Conference: Chairman Jerome Powell speech live stream – February 1

Fed Powell's comments so far

Powell speech: Very difficult to manage the risk of doing too little on rates

Powell speech: Disinflationary process is in early stages

Powell speech: History cautions against prematurely loosening policy

Powell speech: Well-anchored longer-term inflation expectations not grounds for complacency

Powell speech: Will likely have to maintain restrictive stance for some time

EUR/USD H4 chart

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"Policymakers did not see this as a time to pause."

"Taking pauses in between moves is not something the Committee is talking about in any detail."

"Before a rate hike every other meeting was the norm but we have not yet decided path ahead."

"Overall my own view is we will not have sustainable return to 2% core ex housing sector inflation without increased labor slack."

"Most forecasters would say unemployment will probably rise a bit."

"There is a path to getting inflation to 2% without a significant economic decline."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"Very difficult to manage the risk of doing too little on rates."

"We don't want inflation springing back."

"We have no desire to overtighten, but we have tools that would work on that if we do."

"It would be very premature to declare victory on inflation."

"Until we see all aspects of inflation coming down, we still have a lot of work to do."

"We can now say for first time that disinflationary process has started, we see it in goods sector."

"But that's around 1/4 of the PCE Price Index."

"We see disinflation in the pipeline for housing."

"We expect to see that disinflation process will be seen soon in the core services ex-housing, but we don't see it yet."

"Labor market will probably important to bring that aspect of inflation down."

"We're talking about a couple more rate hikes to get to appropriately restrictive stance."

"We are not very far from that level."

"Policy is restrictive, trying to judge about how much is restrictive enough."

- AUD/USD snaps three days of losses as the Federal Reserve increased rates by 25 bps.

- Federal Reserve officials stated that more increases would be appropriate.

- US central bank policymakers decided that future rate hikes would be in 25 bps increments.

AUD/USD pares some of its earlier losses, aiming higher after the US Federal Reserve (Fed) lifted rates by 25 bps as expected by market participants, though emphasized that further increases would be appropriate, putting expectations for a Fed pivot in the backseat. At the time of writing, the AUD/USD is trading volatile in the 0.7040-0.7115 range.

Remarks of the Federal Reserve’s monetary policy statement

On Wednesday, the Federal Reserve policymakers decided unanimously to hike rates by 0.25%, lifting the Federal Funds rate (FFR) at around 4.50% - 4.75%. Additionally, they pushed back against the market’s expectations for a Fed pivot and said additional rate hikes would be appropriate. Policymakers forward guided the market, adding that future rate hikes would be in 25 bps increments, dropping the reference to the “pace” of additional rate hikes.

Fed officials acknowledged that inflation has “eased somewhat but remains elevated.” Participants added that indicators point to modest growth in spending and production and commented that the labor market remains robust. Fed members stated, “in determining the extent of future rate hikes, it will take into account cumulative tightening, policy lags and economic and financial developments.”

Now that the Fed’s decision is in the rearview mirror, traders can for the Federal Reserve Chair Jerome Powell’s press conference here: Fed Press Conference: Chairman Jerome Powell speech live stream – February 1

AUD/USD reaction to the headline

The AUD/USD 15-minute chart portrays the pair trading nearby a busy confluence of the 20, 50, 100, and 200-Exponential Moving Averages (EMAs). Even though AUD/USD’s price action remains volatile due to the importance of the Fed’s decision, it failed to crack the day’s low at 0.7036. Also, it’s aiming toward printing a new session high above the 0.7100 area, testing the R2 daily pivot point at around 0.7115-20. The break above will expose the 0.7200 mark.

On the flip side, the AUD/USD first support level would be the daily pivot at 0.7034, followed by the S1 pivot at 0.7000.

- GBP/USD has rallied around Fed' Powell's presser and opening statement.

- The US Dollar is volatile around the event.

GBP/USD has rallied to a high of 1.2361 so far despite a hawkish Federal Reserve chairman Jerome Powell turning the screw with regard to inflation targets following the Fed's interest rate decision. The central bank raised interest rates for the eighth time in a year but slowed its pace to a quarter of a point in a nod to an improved inflation outlook.

Fed statement

Key notes:

- FOMC policy vote was unanimous, to continue balance sheet reduction as planned.

- Reaffirms policy framework, and inflation target.

The Fed is retaining its prior language in the statement and Fed fund futures are still pricing in rate cuts this year, with the Fed funds rate seen at 4.486% by end of December, unchanged prior to the Fed decision. The March meeting is priced in at 85% for 25 bps with the remainder at no change.

Fed Powell's presser

Key notes so far:

-

Powell speech: History cautions against prematurely loosening policy

-

Powell speech: Well-anchored longer-term inflation expectations not grounds for complacency

-

Powell speech: Will likely have to maintain restrictive stance for some time

-

Fed Press Conference: Chairman Jerome Powell speech live stream – February 1

The disinflation process is underway and this is propelling the greenback lower.

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"It is a good thing that disinflation so far has not come at expense of labor market."

"But this disinflationary process is in early stages."

"In housing services, we expect inflation to continue moving up but then moving down as new leases come in lower."

"But in core services ex-housing we don't see disinflation yet."

"It's gratifying to see disinflationary process underway, with continued strong labor market."

"Employment Cost Index and Average Hourly Earnings have abated somewhat, although still fairly elevated."

"We see wages moving down."

"By many many indicators job market is still very strong."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"Seeing effects of policy on demand in housing, but will take time for full effects to be realized."

"Will take time for full effects of our actions to be realized."

"These lags fed into our decision to raise by 25 bps today."

"In light of cumulative tightening and lags, Fed continued step-down from last year's fast pace."

"A slower pace allows us to better assess progress toward our goals."

"We will continue to make decisions meeting by meeting."

"Our focus in on using our tools to bring inflation down."

"Reducing inflation is likely to require below trend growth, some softening in labor market."

"History cautions against prematurely loosening policy."

"We will stay the course until job is done."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"Wage growth is elevated."

"Job market is extremely tight, job gains have been robust."

"Labor market continues to be out of balance."

"Pace of job gains has slowed and nominal wage growth too, but labor market still out of balance."

"Labor demand substantially exceeds supply."

"Inflation is well above our goal."

"Inflation data over past 3 months show welcome reduction in pace of increases but we need substantially more evidence to be confident inflation is on a downward path."

"Longer-term inflation expectations remain well anchored but that's not grounds for complacency."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023.

Key quotes

"We have taken forceful actions over past year."

"We have covered a lot of ground, full effects yet to be felt."

"We have more work to do."

"We continue to anticipate ongoing increases will be appropriate to get to sufficiently restrictive stance."

"We will likely have to maintain restrictive stance for some time."

"Economy slowed significantly last year."

"Consumer spending appears to be subdued."

"Housing activity continues to weaken."

Jerome Powell, Chairman of the Federal Reserve System, will be delivering his remarks on the monetary policy outlook at a press conference following the meeting of the Board of Governors. Powell's speech will start at 19:30 GMT.

Follow our live coverage of the market reaction to Powell's press conference.

Fed hikes policy rate by 25 bps to 4.5-4.75% as expected.

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

- Gold price seesaws in a $10 range after the Federal Reserve hiked rates by 25 bps.

- Federal Reserve officials stated that more increases would be appropriate.

- US central bank policymakers decided that future rate hikes would be in 25 bps increments.

Gold price rises following the US Federal Reserve (Fed) decision to slow the pace of interest rate increases and lifted the Federal Funds rate (FFR) by 25 bps to the 4.50% – 4.75% area. At the time of writing, the XAU/USD is trading volatile but above its opening price, at around the $1920-$1930 range.

Summary of the monetary policy statement

In its monetary policy statement, Fed officials voted unanimously to raise rates by 25 bps, emphasizing that additional rate hikes would be appropriate, pushing against the financial market’s expectations for a Fed pivot.

Policymakers acknowledged that inflation has “eased somewhat but remains elevated.” The Fed added that indicators point to modest growth in spending and production and commented that the labor market remains robust. Officials added, “in determining the extent of future rate hikes, it will take into account cumulative tightening, policy lags and economic and financial developments.”

Fed officials commented that future rate hikes would be in 25 bps increments, dropping the reference to the “pace” of additional rate hikes.

Now that the Fed’s decision is in the rearview mirror, traders prepare for the Federal Reserve Chair Jerome Powell’s press conference at around 19:30 GMT.

Gold’s reaction to the headline

As shown in Gold’s 15-minute chart, In its initial reaction, the XAU/USD edged towards the daily pivot, though slightly above it, around $1920, and pushed upwards, clearing the 200, 100, 50, and 20-Exponential Moving Averages (EMAs). It should be said that XAU/USD’s is seesawing around $1920-$1930, and it would remain volatile during the press conference of Jerome Powell.

- EUR/USD is biased to the downside as it takes out the near-term structure around 1.0905 after the Fed interest rate decision.

- The Fed chairman Jerome Powell will be the next event that would be expected to cause more volatility and determine the direction of the Euro ahead of the ECB.

EUR/USD is bouncing around 1.0900 after the Federal Reserve raised interest rates for the eighth time in a year, but slowed its pace to a quarter of a point in a nod to an improved inflation outlook.

Federal Reserve statement

Key notes:

- FOMC policy vote was unanimous, to continue balance sheet reduction as planned.

- Reaffirms policy framework, and inflation target.

The Fed is retaining its prior language in the statement and Fed fund futures are still pricing in rate cuts this year, with the Fed funds rate seen at 4.486% by end of December, unchanged prior to the Fed decision. The March meeting is priced in at 85% for 25 bps with the remainder at no change.

Next up will be Jerome Powell who speaks to the press.

Watch live: Jerome Powell's presser

EUR/USD technical analysis

As per the pre-Fed analysis made ahead of the Tokyo open on Tuesday, EUR/USD Price Analysis: Bulls eye a move to test 1.0900/20, the price has broken the structure, leaving the bias to the upside for the sessions ahead of the Federal Reserve.

EUR/USD H4 chart, prior analysis:

It was stated that the support came in near a 38.2% Fibonacci retracement of the prior bullish 4-hour impulse where a correction could be expected to decelerate. This comes in at 1.0850. On the upside, 1.0900 came in at the target with 1.0920 above there as a potential liquidity zone into the Fed.

EUR/USD update

The price behaved accordingly and was pumped up to sweep liquidity through 1.0900 as forecasted, conveniently poised for either a sell-off around the Fed or a continuation of the move having already broken resistance structure.

EUR/USD post-Fed interest rate decision and statement

Before the announcement and statement, the price was sitting in a 50% mean reversion area on the hourly chart, on the front side of the bullish dynamic support. Given it had already broken structure to the upside, bulls were in place in anticipation of a move up. This left a bearish case for a test of major structure at 1.0888 and a subsequent move lower, trapping the breakout longs. On the other hand, a dovish outcome would have been perceived as bearish for the US Dollar and leave 1.0950 exposed in a -61.8% extension of the recent correction of the prior bullish impulse.

EUR/USD after the Fed, initial knee-jerk reaction

EUR/USD was offered to 1.0891 (breaking through technical structure again) on the knee-jerk of the Federal Reserve announcement. The price then attempted a move higher in volatility around the decision to hike just 25 basis points, touching a fresh higher for the day of 1.0925. It has now made a fresh session low of 1.0891 at the time of writing as the bears move in for the kill. This leaves the bias to the downside into the Fed chair's presser. However, should he fail to convince markets should he attempt to push back prospects of a pivot later this year, then the Euro could take off and break the 1.0920s resistance as explained above on the charts with 1.0950 eyed.

The US Federal Reserve on Wednesday announced that it raised the policy rate, federal funds rate, by 25 basis points to the range of 4.5-4.75% following the first policy meeting of 2023. This decision came in line with the market expectation.

Follow our live coverage of the Fed's policy announcements and the market reaction.

In the policy statement, the Fed noted that 'ongoing increases' in rates will be appropriate and added that inflation remains elevated despite having eased somewhat.

Market reaction

The US Dollar Index edged slightly higher with the immediate reaction but quickly erased its gains as investors await FOMC Chairman Jerome Powell's press conference. As of writing, the index was down 0.26% on the day at 101.82.

Key takeaways from policy statement, via Reuters

"In determining the extent of future rate hikes, will take into account cumulative tightening, policy lags, and economic and financial developments."

"Recent indicators point to modest growth in spending and production."

"Job gains have been robust in recent months, unemployment rate has remained low."

"Russia's war against Ukraine is contributing to elevated global uncertainty, Fed remains highly attentive to inflation risks."

"Will continue reducing the balance sheet as planned."

"Vote in favor of policy was unanimous."

- USD/CAD bears chipped away at the 1.3305 structure before bulls moved in to test bears at the 1.3350s.

- The Fed will determine when the price heads towards 1.3320s and then the 1.3150s or, on the upside, we have 1.3380s that guard the 1.3450/80s.

As per the prior analysis, USD/CAD Price Analysis: Bears seek a break of key support while on the front side of bear trend, bulls have moved in to test the critical resistance area near the 1.3350s ahead of the Federal Reserve's interest rate decision.

For the US Dollar, this event will be important and it could catch a bid if the outcome is far more hawkish than what would be otherwise anticipated. A pushback against the sentiment of a pivot could stir up some demand for the greenback which sees a higher USD/CAD but anything to the contrary would likely see 1.3300 come under pressure with the price already jammed in on the front side of the bearish trendline following a failed breakout.

USD/CAD, prior analysis daily charts

Zoomed in ...

It was stated, that with the breakout failure, the bears remained in control.

USD/CAD H1 chart

However, in the Asian session, when the analysis was drawn on the above charts, it was also explained that the bulls could be seeking a move to test the commitments of the bears again following the failed breakout with the 50% mean reversion resistance eyed.

USD/CAD update

The bulls moved in as anticipated and now the price will be determined by the Federal Reserve event. In this regard, we have the levels marked as follows:

We have already seen the bears chip away at the 1.3305 structure, and this is technically already broken, exposing the 1.3320s and then the 1.3150s. On the upside, we have 1.3380s that guard the 1.3450/80s.

- The USD/CHF is trapped within a 140 pip area, trendless and fluctuating around the 20-day EMA.

- USD/CHF Price Analysis: The pair is neutral downwards, and it could test the YTD low during the session.

The USD/CHF remains subdued in Wednesday’s North American session, with markets awaiting the Federal Reserve’s (Fed) decision regarding its monetary policy. At the time of typing, the USD/CHF exchanges hands at around 0.9150s, almost flat.

USD/CHF Price Analysis: Technical outlook

The pair remains consolidated in the 0.9140 to 0.9280 area for the tenth consecutive day, though the USD/CHF fell and hit a new weekly lof of 0.9136 before recovering some ground, resting at around the 0.9150 area. Nevertheless, the USD/CHF bears remain in charge, as the daily EMAs sits above the spot price, while oscillators like the Relative Strength Index (RSI) and the Rate of Change (RoC) suggest the neutral-downward bias remains intact.

The USD/CHF support areas would be the day’s low at 0.9136, followed by the 0.9100 figure. Once broken it will exacerbate a USD/CHF fall to the YTD low of 0.9085, followed by the 0.9000 psychological figure.

On the other hand, if the USD/CHF reclaims 0.9200, then the 20-day EMA would be up for grabs at 0.9220. Once done, the USD/CHF could aim towards the January 31 daily high at 0.9288, on its way to the 0.9300 psychological barrier.

USD/CHF Key Technical Levels

- Silver fails to hold to its earlier gains above the 20-day EMA, with traders eyeing $23.00.

- Silver Price Analysis: Consolidated, slightly skewed downwards, as oscillators turned bearish.

Silver price struggles at the 20-day Exponential Moving Average (EMA) at $23.66 and is dropping toward the lows of the day, at around $23.40s, as investors prepare for the US Federal Reserve’s (Fed) monetary policy decision. Therefore, XAG/USD traders are squaring their positions, awaiting Jerome Powell and his colleagues. At the time of writing, the XAG/USD exchanges hands at $23.44, below its opening price by 1.12%.

Silver Price Analysis: XAG/USD Technical Outlook

Silver remains pressured ahead of the FOMC’s decision, trapped within Tuesday’s price action, which witnessed a test of the 50-day Exponential Moving Average (EMA) at $23.11, though it was quickly rejected, achieving a daily close above the 20-day EMA. However, Wednesday’s story is different. The XAG/USD fell below Monday’s low of $23.54, eyeing to extend its losses toward the $23.00 figure.

Momentum indicators, like the Relative Strength Index (RSI), turned bearish, while the Rate of Change (RoC), suggests that sellers are gathering momentum.

Given the backdrop, the XAG/USD first support would be the $23.00 psychological level. A breach of the latter and the year-to-date (YTD) low at $22.76 is on the cards.

As an alternate scenario, the XAG/USD’s reclaiming the 20-day EMA will expose the $24.00 figure. Once cleared, Silver would test the YTD high at $24.54, followed by a rally to the $25.00 mark.

Silver Key Technical Levels

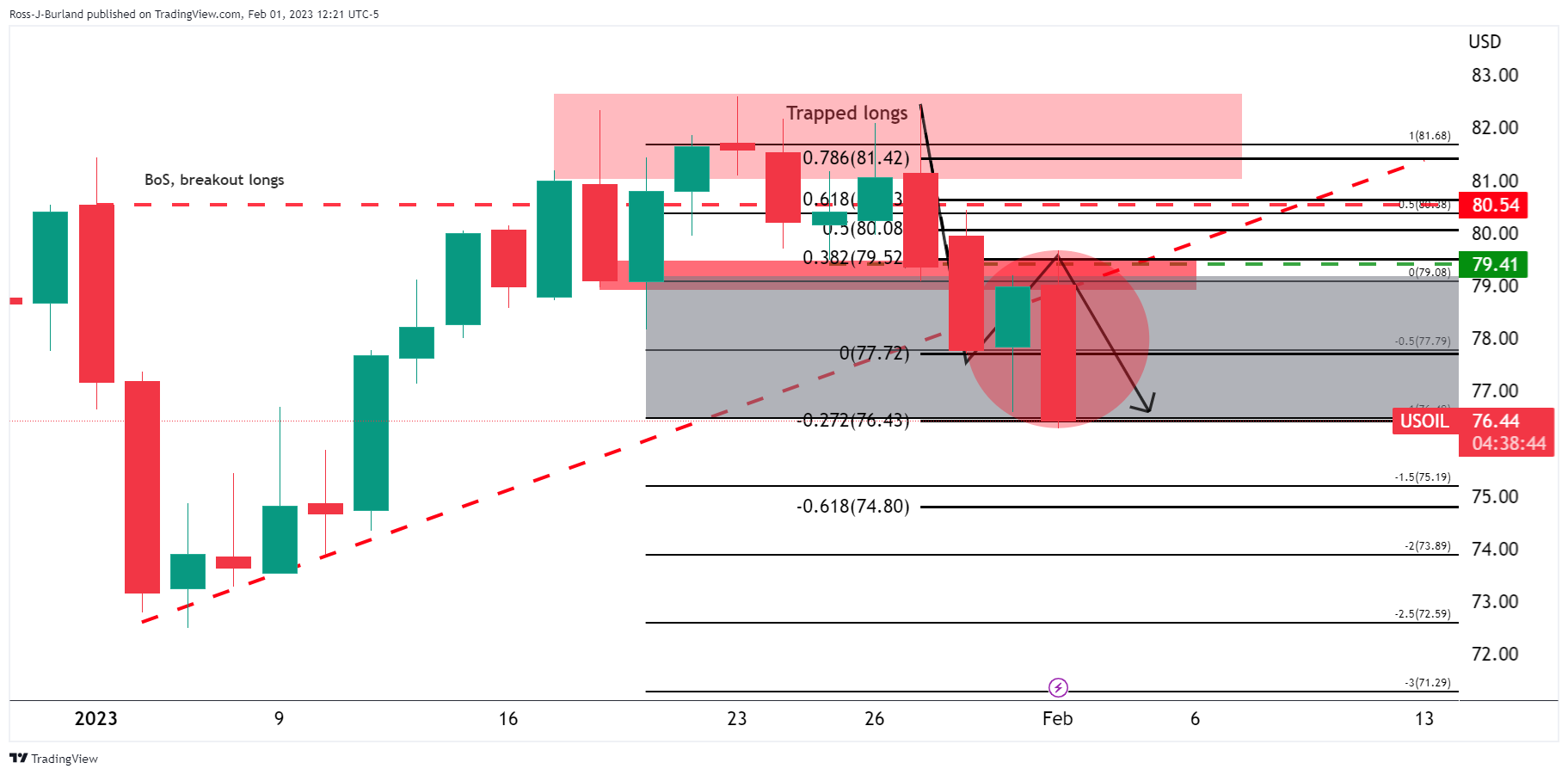

- WTI bears break the hourly structure at $77.70 and the focus is on the downside.

- Bulls eye a higher resistance up at 61.8% Fibonacci retracement level near $78.50. While below there, the bias is to the downside.

- Bears can target between $75.36 and $74.88 on a break of $75.50.

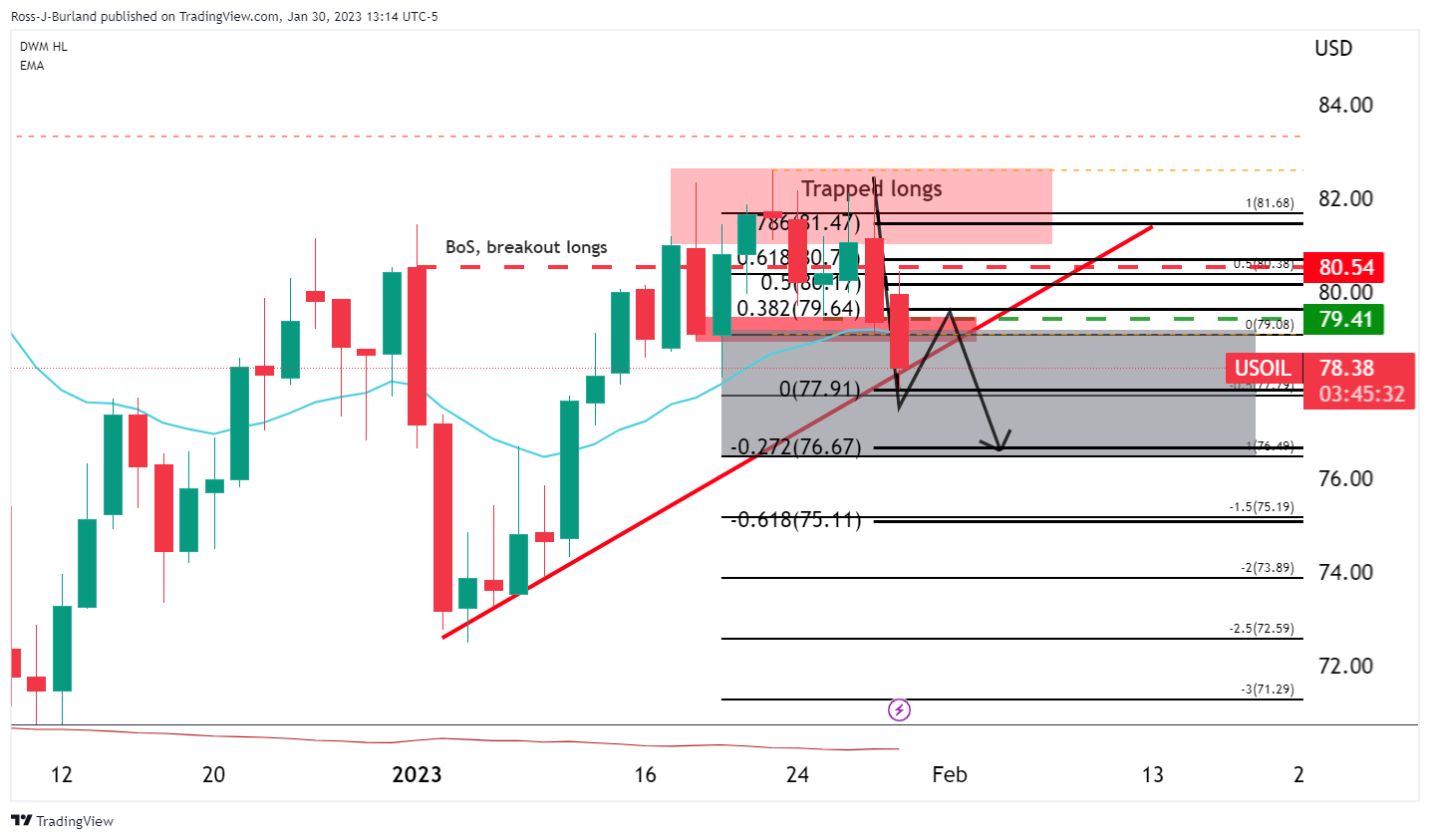

As per the prior analysis, WTI bears taking control into the Fed, eyes on $75.00bbl, the price of oil has indeed dropped towards the target areas as forecasted at the start of the week, pulling away from the trapped volume that had accumulated around $79.40/50. The following illustrates the price action and gives an update with prospects of a correction before the next move lower.

WTI, prior technical analysis

It was suggested that ''a correction into resistance could entice trapped longs to get out of losing or breakeven positions and subsequently the shorts coming onto the market around 38.2% Fibonacci correction could see a move out of the consolidation below the trapped volume and into a 100% measured target towards $75.00 over the course of the coming week.''

WTI Update

As illustrated, the price sank into the target area following a correction into where shorts were looking to get in at a premium. The subsequent move has fulfilled the 100% measured move and $75.00 beckons:

WTI H1 charts

Zoomed in ...

The greyed areas are price imbalances while the red marking is a resistance zone that has a confluence with the 61.8% Fibonacci retracement level near $78.50. While below there, the bias is to the downside. However, a more shallow correction may be all that is needed towards the 38.2% Fibo at $77.70. Either way, bears can target between $75.36 and $74.88 on a break of $75.50.

- Gold price shifted negatively as time for the US Federal Reserve decision approaches.

- ADP Employment Change was lower than estimates; would it be a prelude for Friday’s NFP?

- US factory activity in the United States remains in contractionary territory.

Gold price retraces from the day’s high and failed to hold to earlier gains after a busy US economic calendar released its first tranche of data, which was worse than estimated. In addition, a soft US Dollar (USD), capped the XAU/USD’s fall, while US Treasury bond yields continued to push downwards. At the time of writing, the XAU/USD exchanges hands at around $1925.

US economic data was mixed ahead of the FOMC’s meeting

Wall Street remains depressed ahead of the Fed’s monetary policy decision. US economic data showed that the labor market continues to ease as the ADP National Employment Change, which reports private hiring revealed that companies hired 106K employees, well below the 178K foreseen. Later, the JOLTs Job Openings report showed that vacancies rose to 11.01M exceeding estimates of 10.25M.

In addition, factory activity was updated by two firms, showing that manufacturing activity remains in contractionary territory. The S&P Global Manufacturing PMI for January jumped by 49.9 above the 46.8 estimates, better than expected but at recessionary territory. Elsewhere, the ISM Manufacturing PMI for January plunged to 47.4, below December’s 48.4, and dropped for the third straight month pushing the index to its lowest level since May 2020.

Aside from this, Gold traders remained laser-focused on the US Federal Reserve decision. Traders expect a 25 bps rate hike and further guidance from the US central bank. At around 13:30 GMT, the Fed Chair Jerome Powell would hit the podium, and each word would be scrutinized as investors expect a Fed pivot, from hiking rates, to cutting them by the second half of 2023.

Gold Technical Analysis

In the last five trading days, XAU/USD has failed to crack the $1950 psychological barrier, reaching a YTD high of 1949.16. on January 26. Since then, the XAU/USD dropped toward the 20-day Exponential Moving Average (EMA) at $1902.38 and gained traction toward the $1930 area, unable to re-test the YTD highs. That could be attributed to traders booking profits or awaiting Powell and Co.’s decision.

Gold’s key resistance levels lie at the current week’s high of $1934..47, followed by the YTD high at $1949.16, and then the $2000 mark. On the other hand, XAU/USD’s demand areas would be the 20-day EMA at $1904.83, followed by the January 18 swing low of $1896.74.

Gold is having a difficult time gathering further bullish momentum. Economists at Credit Suisse expect the yellow metal to stage a consolidantion phase.

Short-term momentum is turning lower

“Gold has stalled in the short-term just ahead of our tactical objective at the 78.6% retracement of the 2022 fall and April 2022 high at $1,973/98, with a fresh cap still expected here. Short-term momentum is also turning lower, reinforcing the case for a lengthier pause.”

“From a more medium-term perspective, only above the $2,070/72 record highs of 2020 and 2022 would suggest we are seeing a significant and meaningful long-term break higher, with resistance levels then seen at $2,300, then $2,500. This is not our base case for now though.”

“Support is seen at $1,897 initially, below which can see a pullback to the 55DMA, currently seen at $1,829.”

The greenback continues to weaken in the new year. Economists at the National Bank of Canada still anticipate a policy change from the FOMC in the first quarter of 2023, which would set the stage for a more prolonged decline.

Inflation easing more than expected

“Markets are embracing our longheld forecast that the US central bank will be forced to lower interest rates in H2 2023. It would be a mistake for the Fed to persists in raising its key rate well beyond the current level and holding it there for an extended period if inflation continues to surprise on the downside.”

“We still anticipate a policy change from the FOMC in the first quarter of 2023, which would set the stage for a more prolonged decline in the greenback. That said, the Dollar looks oversold at this stage and we think a temporary rebound is possible in the coming weeks, as we have not yet confirmed a change in the Fed's policy direction.”

- A volatile session is expected with the FOMC meeting.

- USD/MXN continues to consolidate near 18.75, below the 20-day SMA.

- A break above 18.90 could trigger more gains for the US Dollar.

The USD/MXN is falling on Wednesday, following the release of US economic data and ahead of the Federal Reserve decision. A 25 basis points rate hike is priced in and the key diver for action would be the outlook presented in the statement and in Powell’s comments. Volatile hours are expected across the FX board.

The daily chart shows the bias in USD/MXN is still to the downside, although losses continue to be limited by 18.75 and technical indicators do not offer clear signs with RSI flat and Momentum approaching 0 from the downside but about to turn south again. A consolidation below the 18.75 area should open the doors to a bearish extension targeting 18.62 initially. The next support is located at 18.55.

Hours ago, the USD/MXN peaked at 18.86, slightly below the 20-day Simple Moving Average, today at 18.88. The area around 18.90 has become a critical short-term resistance area. If the US dollar breaks and holds above, a recovery to 19.00 and more, seems likely. The next resistance stands at 19.10.

Technical levels

EUR/USD’s listless price action continues. Economists at Société Générale expect the pair to slow the pace of its advance.

Inflation outlook ensures a hawkish ECB

“Energy subsidies have supported European growth at the expense of increased public sector debt, and a mild winter has significantly reduced the near-term threat of energy shortages. The growth outlook helps the Euro, and the inflation outlook ensures a hawkish ECB.”

“The impact of the ECB stepping back from the bond market while governments borrow more is to suck European investors back into European government bonds as yields rise. That is Euro supportive. From here though, the pace of Euro gains should slow, at least for now.”

- GBP/USD remains firm ahead of the US Federal Reserve’s decision.

- A busy US economic calendar did little to help the US Dollar, which remained pressured amidst a risk aversion scenario.

- UK’s PMI improved but remained in contractionary territory for the sixth straight month, ahead of Thursday’s BoE meeting.

The GBP/USD snaps three days of consecutive losses and rises by a decent 0.22% on Wednesday amidst a risk-off impulse in the financial markets courtesy of a looming US Federal Reserve (Fed) decision. Except for the US Dollar (USD), most safe-haven peers remain on the front foot. Hence, the GBP/USD exchanges hands at around the 1.2320s area, slightly above the 20-day Exponential Moving Average (EMA).

Data from the United States is mainly ignored by traders eyeing the Fed

The Pound Sterling (GBP) holds to early gains following a tranche of US economic data release. The ADP National Employment Change report reports private hiring increased by 106K last month, below the 178K foreseen. Of late, the S&P Global Manufacturing PMI for January rose by 46.9 above 46.8 estimates, indicating that factory activity is beginning to improve, though at a slower pace.

A later report by the Institute for Supply Management (ISM) revealed that the PMI for January sank further, dropping to 47.4 from 48.4 in December for the third consecutive month and pushing the index to its lowest level since May 2020. At the same time, the JOLTs report showed that openings rose to 11.01 M in December, above estimates of 10.25 M.

Even though most of the US data released was worse than expected, the GBP/USD could not gain traction to test the daily high of 1.2345.

Across the pond, the UK economic docket presented the S&P Global/CIPS Manufacturing PMI for January, surprisingly above estimates of 46.7, came at 47 but remained at contractionary territory for a sixth consecutive month. The positive news of the report was that costs are slowing and supply chain pressures are easing.

In Brexit news, sources reported that the EU has reportedly accepted a UK customs proposal allowing goods to flow unchecked from Great Britain to Northern Ireland, while goods set for export into the Republic of Ireland would undergo checks in Northern Irish ports. There had been reports that both sides wanted a deal before April 25. It should be noted that despite Brexit headlines crossing the screens, the GBP barely reacted to that news.

Aside from this, the Bank of England is expected to raise rates on Thursday by 50 bps at its first monetary policy meeting of 2023.

GBP/USD Technical Analysis

Technically speaking, the GBP/USD has resumed its uptrend, at risk of central bank decisions, increasing the volatility from today until Friday of the current week. On the downside, the 20-day EMA at 1.2286 would be the first critical support, opening the door for further downside once cleared. The confluence of the 50 and 100-day EMAs, around 1.2139, would be difficult to surpass. On the other hand, the GBP/USD first resistance would be 1.2400, followed by the strong 1.2500 mark.

Economists at Rabobank expect the Fed to hold rates at their peak level until 2024. Thus, the US Dollar is set to to find support, though this may not be this week.

Labour market conditions remain tight

“In our view, the Fed is likely to hold rates at their peak until 2024 in order to squeeze out too high services sector inflation. Assuming the market adjusts in line with our outlook, the USD is likely to find support, though this may not be this week.”

“Given the market’s recent tendency to look through hawkish Fed commentary, there is no guarantee that similar overtones by the FOMC today will find much carry through unless they are backed-up by stronger than expected economic data.”