- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- DXY remains sidelined around multi-year high, probes four-day uptrend.

- 10-year, 2-year yield curve propels recession fears, FOMC Minutes highlights hawkish Fed bets.

- Softer US statistics, lack of major data/events in Asia allow bulls to take a breather.

- US ADP Employment Change to decorate calendar, risk catalysts are more important for clear directions.

US Dollar Index (DXY) bulls take a breather around 20-year, seesaws around 107.05-10 after the four-day uptrend. That said, the quote’s latest inaction challenges bulls during Thursday’s Asian session. However, the bears need validation from the US ADP Employment Change data and risk catalysts.

That said, the greenback gauge rallied to the highest levels in two decades as softer data couldn’t probe the USD bulls amid hawkish Fed Minutes and yields curve inversion, not to forget economic pessimism in Eurozone.

US ISM Services PMI for June dropped to 55.3 versus 55.9 in May. The actual figure, however, came in better than the market expectation of 54.5. It’s worth noting that the US JOLTS Job Opening for May declined to 11.25 million versus 11.00 million expected and 11.68 million prior.

That said, the US 10-year Treasury yields bounced off a three-week low to 2.93% but the higher print of the 2-year bond coupon, around 2.99%, which in turn hints at the global recession fears. International Monetary Fund (IMF) Managing Director Kristalina Georgieva also said, per Reuters, “Global economic outlook has 'darkened significantly' since last economic update.” the IMF chief also added, “Cannot rule out the possible global recession in 2023.”

Germany and Italy have already signaled early signs of economic slowdown and the bloc’s Retail Sales also dropped to 0.2% in May versus 4.0% recorded in April and 5.4% estimated. Also negative for the old continent were chatters that the European Central Bank’s (ECB) crisis-fighting scheme risks being tied up in legal and political knots, per the Financial Times (FT).

Amid these plays, the Wall Street benchmarks closed with mild gains whereas the S&P 500 Futures remain directionless around 3,850 by the press time.

Moving on, DXY traders should pay attention to the monthly print of the US ADP Employment Change for June, expected 200K versus 128K prior, as it becomes the early signal for Friday’s Nonfarm Payrolls (NFP). Additionally important will be the recession signals and other second-tier US data, like weekly jobless claims and monthly trade numbers.

Also read: ADP Net Employment Change June Preview: Can employment stave off a recession?

Technical analysis

US Dollar Index is gradually rising towards September 2002 high near 109.80 until it stays above the previous resistance line from May 13, close to 106.30 by the press time.

- Investors should brace for a volatility contraction on Falling Wedge formation.

- The kiwi bulls have defended the weekly lows at 0.6146 for the second time.

- The antipodean is struggling to surpass the 20-period EMA at 0.6253.

The NZD/USD pair is oscillating in a narrow range of 0.6139-0.6158 in the Asian session. The kiwi bulls have defended the weekly lows at 0.6146 for the second time on Wednesday. Broadly, the asset has turned sideways and may display a volatility expansion on the availability of a potential trigger.

On an hourly scale, the formation of the Falling Wedge is indicating a lackluster performance by the major going forward. The upper portion of the chart pattern is placed from June 16 high at 0.6396 while the lower portion is plotted from June 14 low at 0.6196. Usually, the above-mentioned chart pattern leads to a bullish reversal after the upside break of the upper portion of the former.

The downward-sloping trendline placed from Monday’s high at 0.6253 will act as a major hurdle for the counter.

The antipodean is struggling to surpass the 20-period Exponential Moving Average (EMA) at 0.6156, which signals that the short-term trend is still not lucrative for the kiwi bulls.

Meanwhile, the Relative Strength Index (RSI) (14) is focusing surviving the attacks and holding the 40.00 mark to keep bulls alive.

A decisive move above Wednesday’s high at 0.6176 will drive the asset towards the round-level resistance at 0.6200, followed by June 22 low at 0.6244.

On the flip side, the greenback bulls could regain control if the major drop below Tuesday’s low at 0.6124. An occurrence of the same will drag the asset towards 25 May 2020 low at 0.6084. A violation of 0.6084 will expose the asset to more downside potential towards the psychological support of 0.6000.

NZD/USD hourly chart

-637927482986577745.png)

“The Bank of Canada (BOC) is set to raise its overnight rate by a hefty 75 basis points (bps) this month and by another 50 in September, front-loading a campaign to take monetary policy to where it will restrain the economy,” according to a Reuters poll of 29 economists.

Key findings

But the June 30-July 6 survey suggests the BoC will halt earlier than the Fed, pausing throughout next year in part as deeply indebted Canadian households are more vulnerable to higher borrowing costs.

Still, over 90% of respondents, 27 of 29, said the BoC, which already delivered back-to-back 50 basis point hikes at its previous two meetings, will deliver a 75 basis point hike to 2.25% on July 13 following a similar move at the Fed's June meeting.

The BoC will hike again by 50 basis points in September, according to a significant majority of economists, taking the overnight rate to 2.75%. That is well into a neutral range - where the economy is neither stimulated nor restricted by policy - estimated at 2-3% by economists in the poll.

Most respondents said the BoC will dial down the size of its hikes to 25 basis point increments or lower in October and December, taking the rate to 3.25% by year-end, in line with interest rate futures. But over one-quarter of poll respondents predicted the year-end rate to be higher than that.

The BoC is expected to pause throughout next year even as the Fed carries on raising rates.

Inflation was expected to cool significantly from a near 40-year high of 7.7% in May to 2.2% by the fourth quarter of next year, according to the poll, as recession risks rise.

All economists but one responding to an additional question said the cost of living crisis would not ease significantly for at least six months.

Also read: USD/CAD retreats towards 1.3000 as oil recovers, focus on US ADP Employment

- GBP/JPY grinds higher after bouncing off the lowest levels in three weeks.

- Bullish candlestick, rebound from 100-DMA favor buyers amid steady RSI.

- 50-DMA guards immediate upside amid bearish MACD signals.

GBP/JPY defends the previous day’s rebound from the 100-DMA as it picks up bids around 162.15 during Thursday‘s Asian session. In doing so, the cross-currency pair also justifies the ‘Dragonfly Doji’ candlestick marked on Wednesday.

Given the RSI (14) favoring the recent rebound from a three-week low, backed by bullish candlestick formation and a U-turn from the 100-DMA, GBP/JPY is likely approaching the 50-DMA hurdle surrounding 162.80.

However, a convergence of the 21-DMA and a downward sloping resistance line from June 22, near 164.80, appears the key resistance level to watch.

Should the GBP/JPY prices rally beyond 164.80, the odds of witnessing a north-run towards the previous monthly peak of 168.73 can’t be ruled out.

On the contrary, pullback moves remain unimportant beyond the 100-DMA support level of 160.90.

Following that, an upward sloping trend line from early March, near 159.50, will be crucial to watch for the GBP/JPY bears.

In a case where the quote provides a daily closing below 159.50, a slump towards May’s low of 155.59 becomes imminent.

GBP/JPY: Daily chart

Trend: Limited upside expected

- USD/CAD extends pullback from multi-year high, pressured of late.

- Oil prices print corrective pullback despite recession fears, API inventory build.

- Softer US data probes USD bulls ahead of key data/events, FOMC Minutes favored greenback buyers.

- US ADP Employment Change, Canada trade and Ivey PMI data to decorate calendar.

USD/CAD remains pressured around 1.3030, extending the previous day’s pullback from the highest levels since late 2020, as traders pare USD gains amid a quiet Asian session on Thursday. It’s worth noting that the bounce in the prices of Canada’s main export item, WTI crude oil also weighs on the Loonie pair.

USD/CAD printed mild gains on Wednesday, despite the broad US dollar strength and the weakness in the oil prices, as it retreated from the key resistance line around the multi-day high marked on Tuesday.

Also favoring the pullback could be the softer US data. That said, US ISM Services PMI for June dropped to 55.3 versus 55.9 in May. The actual figure, however, came in better than the market expectation of 54.5. It’s worth noting that the US JOLTS Job Opening for May declined to 11.25 million versus 11.00 million expected and 11.68 million prior.

While the softer US data initially allowed the bears to take a breather, the Federal Open Market Committee (FOMC) Minutes favored the pessimism as the Fed policymakers appear determined to announce another 75 basis points (bps) of a rate hike. That said, the latest Fed Minutes highlighted the need for the “restrictive stance of policy” while also saying, “even more restrictive stance could be appropriate if elevated inflation pressures were to persist”.

It should be noted that the WTI crude oil prices eyes to regain the $100.00 level, around $95.80 by the press time while bouncing off a three-month low of $93.20. In doing so, the black gold ignores the market’s fears of economic slowdown and a build in the US inventories, as per the weekly oil stockpile data from the American Petroleum Institute.

Against this backdrop, the US 10-year Treasury yields bounced off a three-week low to 2.93% but the higher print of the 2-year bond coupon, around 2.99%, hints at the global recession fears. The Wall Street benchmarks, however, closed with mild gains.

Given the market’s indecision, traders will pay attention to the monthly readings of Canada trade numbers and the Ivey Purchasing Managers Index for fresh impulse. However, major attention will be given to the US ADP Employment Change for June, expected 200K versus 128K prior, for clear directions.

Also read: ADP Net Employment Change June Preview: Can employment stave off a recession?

Technical analysis

Considering the USD/CAD pair’s sustained pullback from the two-month-old resistance line, around 1.3080 by the press time, the quote is likely to revisit the 10-DMA support of 1.2927.

- AUD/USD is facing volatility contraction as the DXY has turned sideways.

- The aussie bulls have failed to capitalize on the 50 bps rate hike announcement by the RBA.

- This week, the US employment data will be the major trigger for the FX domain.

The AUD/USD pair is juggling minutely above 0.6780 in the early Tokyo session. It looks like the pair is following the footprints of the lackluster US dollar index (DXY) and is witnessing volatility contraction. There is severe pessimism in the FX domain and risk-perceived currencies are falling like a house of cards. However, the aussie bulls have defended their weekly lows of 0.6764 for the second time on Wednesday.

The antipodean has failed to capitalize on the elevation of the interest rate by the Reserve Bank of Australia (RBA). On Tuesday, RBA Governor Philip Lowe hiked its Official Cash Rate (OCR) by 50 basis points (bps). Now, the RBA’s OCR stands at 1.35% after a consecutive half-a-percent rate hike. The RBA is very much focused to bring price stability to its economy as the inflation rate has reached 5.1%, recorded in the first quarter of CY2022.

Meanwhile, the US dollar index (DXY) is displaying back and forth moves above 107.00. The DXY has renewed its 19-year high at 107.26 after the release of the hawkish minutes. Only one Federal Open Market Committee (FOMC) member voted against the rate hike announcement by 75 bps.

Now, investors are shifting their focus entirely to the US employment data, which is due on Friday. As per the market consensus, the US economy added 270k jobs in June, higher than the former release of 390k. However, the Unemployment Rate may remain stable at 3.6%.

- Gold prices are likely to witness more downside on a firmer DXY.

- Hawkish FOMC minutes have brought an intense sell-off in gold prices.

- The US NFP is seen lower at 270k in relation to the prior release.

Gold price (XAU/USD) has turned into a consolidation phase after displaying a sheer downside move to near $1,732.00 in the New York session. On a broader note, the precious metal is in the grip of bears and possesses the downside potential if it violates the crucial support of $1,730.00.

The precious metal is attracting offers as the release of the Federal Open Market Committee (FOMC) minutes on Wednesday infused fresh blood into the US dollar index (DXY). The minutes were extremely hawkish as only one FOMC member was not in support of 75 basis points (bps) interest rate hike. Also, the Federal Reserve (Fed) is ‘unintentionally committed’ to bringing price stability and will elevate interest rates further to the same extent if high inflation persists further.

The DXY has refreshed its 19-year high at 107.26 and more gains are on the way ahead of the US Nonfarm Payrolls (NFP). A preliminary estimate for the economic data is 270k, lower than the prior print of 390k. In today’s session, the spotlight will remain on the Automatic Data Processing (ADP) Employment Change, which may improve to 200k, higher than the prior print of 128k.

Gold technical analysis

On the daily scale, the gold prices are declining towards the horizontal support placed on the 8 March 2021 low at $1,676.87. The 50- and 200-period Exponential Moving Averages (EMAs) have displayed a death cross at $1,850.00, which adds to the downside filters. Meanwhile, the Relative Strength Index (RSI) (14) has shifted into a bearish range of 20.00-40.00, which signals more downside ahead.

Gold daily chart

- GBP/USD refrains from portraying the political crisis at home by posting mild losses at two-year low.

- Over 30 UK diplomats have resigned, 1922 Committee of backbench Tory MPs eye second no-confidence vote.

- Recession fears, hawkish Fed bets exert downside pressure but softer US data probed bears.

- US ADP Employment Change to decorate calendar, UK politics, Brexit drama more important for clear directions.

GBP/USD holds onto the late Wednesday’s bounce-off two-year low around 1.1925 as traders seek fresh clues during Thursday’s initial Asian session. The Cable pair dropped to the lowest levels since March 2020 the previous day as the UK’s political crisis joined Brexit woes and broad recession fears. However, the market’s anxiety ahead of today’s key data/events, as well as softer US statistics, appears to have probed the bears of late.

With over 30 resignations of the British diplomats, including the Chancellor, Health Minister and Tory Party Vice-Chairman, UK Prime Minister Boris Johnson is under immense pressure to step down, even if he rejects such push by some of the remaining Conservatives.

Recently, Michael Gove, one of the most senior ministers in the British government, earlier told Prime Minister Boris Johnson he must quit.

Elsewhere, EU Commissioner for Interinstitutional Relations and Foresight Maroš Šefčovič said on Wednesday that the UK bill on altering the Northern Ireland Protocol is unacceptable.

On a broader front, the US 10-year Treasury yields bounced off a three-week low to 2.93% but the higher print of the 2-year bond coupon, around 2.99%, which in turn hints at the global recession fears. International Monetary Fund (IMF) Managing Director Kristalina Georgieva also said, per Reuters, “Global economic outlook has 'darkened significantly' since last economic update.” the IMF chief also added, “Cannot rule out the possible global recession in 2023.”

It should be noted that US ISM Services PMI for June dropped to 55.3 versus 55.9 in May. The actual figure, however, came in better than the market expectation of 54.5. It’s worth noting that the US JOLTS Job Opening for May declined to 11.25 million versus 11.00 million expected and 11.68 million prior.

The Federal Open Market Committee (FOMC) Minutes also favored the market pessimism as the Fed policymakers appear determined to announce another 75 basis points (bps) of a rate hike. That said, the latest Fed Minutes highlighted the need for the “restrictive stance of policy” while also saying, “even more restrictive stance could be appropriate if elevated inflation pressures were to persist”.

Looking forward, qualitative catalysts are likely to entertain GBP/USD traders ahead of the US ADP Employment Change for June, expected 200K versus 128K prior.

Also read: ADP Net Employment Change June Preview: Can employment stave off a recession?

Technical analysis

A two-month-old support line near 1.1765 seems to restrict short-term GBP/USD downside amid oversold RSI conditions. The corrective pullback, however, needs to cross the monthly resistance line, near 1.2090 by the press time, to recall the buyers.

- EUR/USD remains sidelined after declining to the lowest levels since December 2002.

- Fears of economic slowdown at home amid energy crisis, geopolitical tussles favor bears.

- Softer US data couldn’t help as FOMC Minutes appear hawkish.

- ECB Monetary Policy Meeting Accounts, US ADP Employment Change for June will be crucial to track.

EUR/USD turned out to be the weakest among the G10 currency pairs on Wednesday before bears took a breather around the nearly 20-year low of 1.0161 during the initial hour of Thursday’s Asian session. Apart from the broad pessimism surrounding economic growth and central bankers’ aggression, the energy crisis in the bloc exerted additional downside pressure on the quote ahead of the key data/events.

Germany and Italy have already signaled early signs of economic slowdown and the bloc’s Retail Sales also dropped to 0.2% in May versus 4.0% recorded in April and 5.4% estimated. Also on the negative side were chatters that the European Central Bank’s (ECB) crisis-fighting scheme risks being tied up in legal and political knots, per the Financial Times (FT) also weighing on the EUR/USD prices.

On the other hand, US ISM Services PMI for June dropped to 55.3 versus 55.9 in May. The actual figure, however, came in better than the market expectation of 54.5. It’s worth noting that the US JOLTS Job Opening for May declined to 11.25 million versus 11.00 million expected and 11.68 million prior.

While the softer US data initially allowed the bears to take a breather, the Federal Open Market Committee (FOMC) Minutes favored the pessimism as the Fed policymakers appear determined to announce another 75 basis points (bps) of a rate hike. That said, the latest Fed Minutes highlighted the need for the “restrictive stance of policy” while also saying, “even more restrictive stance could be appropriate if elevated inflation pressures were to persist”.

Elsewhere, International Monetary Fund (IMF) Managing Director Kristalina Georgieva said, per Reuters, “Global economic outlook has 'darkened significantly' since last economic update.” the IMF chief also added, “Cannot rule out the possible global recession in 2023.”

Amid these plays, the US 10-year Treasury yields bounced off a three-week low to 2.93% but the higher print of the 2-year bond coupon, around 2.99%, hints at the global recession fears.

Moving on, risk catalysts are likely to entertain EUR/USD traders ahead of the ECB Monetary Policy Meeting Accounts (mostly known as ECB Minutes), as well as the US ADP Employment Change for June, expected 200K versus 128K prior.

Also read: ADP Net Employment Change June Preview: Can employment stave off a recession?

Technical analysis

Having dropped below the key 1.0360-50 support zone comprising multiple lows marked since May, EUR/USD appears vulnerable to witness further downside towards the 78.6% Fibonacci Expansion (FE) of late March-May downside, near 1.0130. However, any further declines won’t hesitate to recall the 1.0000 psychological magnet back to the chart.

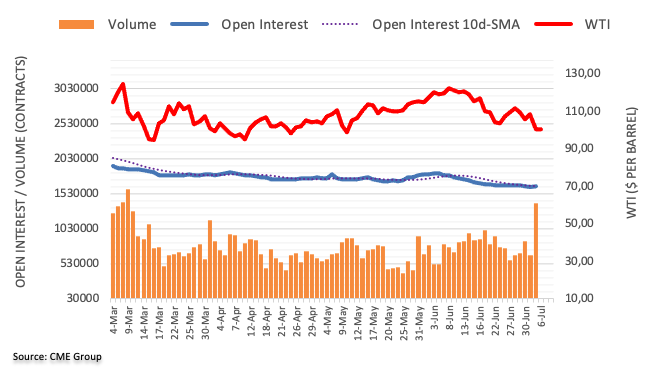

- WTI attempts to recover from the bottom of the barrel.

- The supply remains tight but the uncoiling process could come underway.

West Texas Intermediate (WTI) crude oil was lower again overnight as recession worries continue to weigh on the black gold. At the time of writing, WTI is trading at $98.11 after recovering from the lows of $95.09.

The bears moved in overnight when investors took to the sidelines in anticipation of the Federal reserve minutes and presumed hawkishness from the central bank. The pessimists are expecting that higher rates will lead to a global recession. The consensus is forcing a bid into the bond markets and sending the greenback to fresh 20-year highs.

''The minutes of the US Fed’s June meeting (where they hiked 75bps) reveal a central bank laser focussed on defending its inflation target,'' analysts at ANZ Bank explained.

''There is clearly a concern amongst the FOMC about inflation expectations becoming unanchored,'' the analysts added. ''They noted “that a significant risk… was that elevated inflation could become entrenched if the public began to question the resolve of the Committee to adjust the stance of policy as warranted”. The Fed is understandably eager to reinforce to the public that they’ve got this, and hiking 75bps (and signalling many more hikes to come) certainly reinforces the message.''

Meanwhile, for related updates in the oil market, the analysts noted that ''Kazakhstan is the latest producer to be running into issues. The Caspian Pipeline Consortium, which exports Kazakh crude from a key terminal on the Black Sea, was ordered to halt loadings for 30 days due to a violation of a spill-prevention plan''.

Supply remains tight and little progress has been made toward solving structural supply challenges. Analysts at TD Securities argued that ''even a slow rate of demand growth can endanger energy supply. In this context, Brent crude and distillates prices are also exhibiting strong asymmetry towards upside moves in demand, which could point to an uncoiling process should commodity demand rebound.''

- USD/CHF is juggling around 0.9700 as investors await employment data.

- The Swiss Unemployment data is seen as stable at 2.2%.

- Hawkish Fed minutes have supported the DXY and may display more upside further.

The USD/CHF pair is likely to remain in a consolidation as investors are awaiting the release of the Swiss jobless rate. The asset has turned sideways after failing to cross the critical hurdle of 0.9740. The major is attempting a balance in a tad wider range of 0.9690-0.9740 ahead.

A preliminary estimate for the Swiss Unemployment Rate on a monthly basis is 2.2%, similar to the former release. The Swiss National Bank (SNB) is expected to be delighted with the economic data as it will facilitate a rate hike decision by the central bank. It is worth noting that the SNB is on the path of elevating interest rates now. SNB Governor Thomas J. Jordan announced a rate hike by 50 basis points (bps) in its June monetary policy meeting.

Meanwhile, the US dollar index (DXY) is holding itself comfortably above 107.00. The DXY has turned sideways after the release of the hawkish Federal Open Market Committee (FOMC) minutes on Wednesday. Only one FOMC member was not in support of dictating a 75 bps rate hike. The guidance will also remain highly restrictive if price pressures persist for longer.

In today’s session, the release of the Automatic Data Processing (ADP) Employment Change will remain in focus. As per the market consensus, the job additions in the labor market may improve to 200k, higher than the prior print of 128k. However, the Initial Jobless Claims will remain almost flat at 230k, against the former release of 231k.

- The EUR/JPY is tumbling in the week by some 1.88%.

- Selling pressure trips down the EUR/JPY to fresh weekly lows, below 138.00.

- The EUR/JPY might achieve a mean reversion move towards 139.00 before aiming towards the 100-day EMA at 136.00

The EUR/JPY is almost flat as the Asian Pacific session takes over, up 0.04%, after plunging 0.78% on Wednesday. All that courtesy of a mixed market mood painting a dark economic outlook due to the energy crisis that has the Euro area at the brink of a recession, as Russia squeezes energy supplies to “unfriendly” countries. At the time of writing, the EUR/JPY at 138.40.

Selling pressure trips down the EUR/JPY to fresh weekly lows

US equities finished in the New York session on a higher note. Asian stocks are set to open in negative territory, as illustrated by futures in Asia trading with losses, while safe-haven currencies in the FX market are recording gains.

The EUR/JPY, Wednesday’s open, was near Tuesday’s lows and seesawed through most of the Asian session. However, once the European session took over, EUR/JPY’s sellers stepped in and sent the pair plunging towards a fresh weekly low at around 137.26.

EUR/JPY Daily chart

The EUR/JPY is neutral-upward biased, but the break of the 20 and 50-day EMAs opened the door for sellers, which piled around the 142.50 mark, and at 138.40, July 6 high, spurring EUR/JPY’s losses of 400 pips. A continuation to the downside looms, but a corrective leg towards 139.00 is on the cards.

If that scenario plays out, the EUR/JPY’s first support would be the 138.00 figure. Once cleared, the next support would be the July 6 low at 137.26, followed by the 100-day EMA at 135.92.

EUR/JPY Key Technical Levels

- The USD/JPY rises bolstered by higher US Treasury yields, with the 10-year benchmark note up at 2.932%.

- A mixed market mood, keep safe-haven currencies bid, in the USD/JPY, the greenback.

- A USD/JPY rising wedge in the daily chart might open the door for a pullback towards 132.50 before challenging the YTD high around 137.00.

The USD/JPY steadily advanced on Wednesday and is up 0.50% amidst a mixed market mood session as equities rise while recessionary fears bolster safe-haven currencies. At the time of writing, the USD/JPY is trading at 135.91, shy of weekly highs around 137.00.

The sentiment is mixed as Wall Street closed. US equities rose, except for the Russell 2000, while in the meantime, in the FX market, a risk-off impulse keeps the safe-haven currencies in the driver’s seat.

Regarding the USD/JPY, the greenback got boosted by climbing US Treasury yields. The US 10-year yield erased Tuesday’s losses, rising twelve basis points at 2.932%, a tailwind for the USD/JPY.

USD/JPY Daily chart

The USD/JPY daily chart illustrates the pair as neutral-upward biased. Nevertheless, the major broke a rising wedge, though it remains to trade in the 134.90-136.90 area, signaling that “some” buying pressure lies ahead. However, risks of an intervention by Japanese authorities keep USD/JPY traders uncommitted to lift prices higher, which could open the door for a test of August’s 1998 highs around 147.67.

USD/JPY traders should be aware that a rising wedge was broken to the downside, meaning that prices at a certain time might fall towards 132.50 (the rising wedge profit target). After that, a re-test of the YTD highs around 137.00 is on the cards.

USD/JPY Key Technical Levels

- AUD/USD is in the hands of the bears on the long-term charts.

- Nearereterm, there are prospects of a bullish meanwhile correction.

AUD/USD is pressured mid-week and has been testing below 0.6800 again but has so far failed to break cleanly away despite making a fresh low for the week. Instead, the bulls moved in to take the price back to test the bear's commitments near the figure and failed to break through them. The following illustrates the prospects of both a move higher and lower in a multi-timeframe analysis:

AUD/USD H4 charts

The M-formations are drawing in the price towards the necklines. The grey area is a price imbalance that would be expected to be filled in due course.

AUD/USD daily chart

The daily chart, however, shows that there is a resistance that would guard against a move higher than the mitigation window.

AUD/USD weekly chart

The price is on the verge of moving lower to attenuate the price imbalance below. A correction to restest the neckline of the M-formation could fuel further supply to 0.6616 prior highs.

Michael Gove, one of the most senior ministers in the British government, earlier told Prime Minister Boris Johnson he must quit. As a consequence, the PM has firmed him as he seeks to reshuffle out those that oppose his leadership from within his cabinet.

Resignations began on Tuesday after Downing Street admitted the PM had known about allegations of inappropriate behaviour by disgraced MP Chris Pincher in 2019 before hiring him as deputy chief whip in February.

Mr Pincher resigned from the role last week after further allegations that he groped two men at a private club in London, and he was later suspended from the Conservative Party.

What you need to take care of on Thursday, July 7:

The dollar remained strong on Wednesday, with EUR/USD reaching a fresh 20-year low of 1.0160. The shared currency is among the weakest amid fears of a local recession and the looming energy crisis.

GBP/USD trades around 1.1930, under pressure as the UK Government crisis deepened. Over 30 officials resigned, while many others asked Prime Minister Boris Johnson to leave. The 1922 Committee of backbench Tory MPs is looking to change rules protecting PM Johnson from a second no-confidence vote.

The FOMC released the Minutes of its latest meeting. The document showed that Federal Reserve officials agreed high inflation warranted restrictive interest rates and are open to being even more restrictive if inflation persists. Also, the majority of participants saw a downside risk to growth, while judging there was a “significant risk” higher inflation could become entrenched. Somehow, the US Federal Reserve left the doors open for another 75 bps hike.

Wall Street spent the day struggling to post gains, but major indexes closed the day up. Despite hawkish FOMC Minutes, policymakers refrained from mentioning a 100 bps rate hike, despite pledging to do whatever was needed to tame inflation. Policymakers also refrained from speaking about recession.

The US Treasury yield curve remains inverted. The 10-year note currently yields 2.93%, while the 2-year note currently yields 2.97%. An inverted curve is usually seen as an early sign of recession.

Commodity-linked currencies were little changed against the greenback. AUD/USD trades around 0.6780 while USD/CAD hovers around 1.3040.

The USD/CHF reached a fresh monthly high of 0.9743, while the USD/JPY pair settled at 135.85.

Gold fell to a fresh 2022 low of $1,732.19 a troy ounce, trading nearby at the end of the day. Crude oil prices edged lower, with the barrel of WTI now at $98.40.

Like this article? Help us with some feedback by answering this survey:

- During the week, the New Zealand dollar is down 0.82%.

- The market sentiment is mixed as US equities rally alongside safe-haven currencies.

- The Fed to hike 75 bps in the July meeting, as shown by June’s FOMC minutes.

The New Zealand dollar drops for the second straight day but trades within the boundaries of Tuesday’s price action, just above the weekly low at around 0.6150s, following the release of the US Federal Reserve June meeting minutes. At 0.6152, the NZD/USD portrays a risk-off mood in the FX space, though US equities are rising.

NZD/USD drops due to risk-off mood and a strong US dollar

The kiwi has been under downward pressure as well as most G8 currencies. A buoyant greenback courtesy of worldwide recession fears, another China coronavirus outbreak, and elevated inflation spurred safe-haven flows since Tuesday. The US Dollar Index, a gauge of the greenback’s performance vs. six currencies, rose above the 107.000 mark for the first time since December 2002, reaching a 20-year high at 107.264.

Concerning the awaited US Federal Reserve’s minutes, FOMC pledged to its hawkish posture, and policymakers agreed that a 75 bps rate hike is warranted. Fed officials noted that even a “more restrictive stance” could be appropriate if inflation prevails while acknowledging that economic growth risks are skewed to the downside.

In the meantime, the US 2s-10s yield curve has remained inverted since Tuesday late in the North American session. Analysts at ING commented, “Inverted yield curves are typically bad news for pro-growth currencies (commodity exporters + Europe & Asia ex-Japan) and typically good news for the dollar and the Japanese yen and Swiss franc. This environment looks set to continue over the summer months as the Fed continues to push ahead with tightening.”

Elsewhere, an absent New Zealand economic docket left NZD/USD traders adrift to US economic data and market sentiment.

Earlier during the New York session, the US docket featured S&P Global and US ISM Services and Composite PMIs, with figures beating expectations but trailing previous readings. That illustrates a gloomy scenario as the US economic growth slows down.

The week ahead, the US economic docket will feature ADP Employment Change, Initial Jobless Claims, and Fed speakers on Thursday.

NZD/USD Key Technical Levels

- Gold has extended its downside into fresh bear cycle lows as the US dollar soars.

- Meanwhile, the price is reaching a key area on the daily chart where bulls will likely emerge.

At $1,739.31, the gold price is underwater by some 1.4% in the North American afternoon session and after the release of the Federal Open Committee Minutes which underpinned the prospects of a 50 or a 75 basis point interest rate hike at this month's meeting.

The minutes failed to energise what has turned out to be a relatively quiet session on Wednesday although stocks on Wall Street have risen with the S&P 500 now over 0.6% higher for the day. US stocks gyrated ahead of the minutes but have moved higher given that there was little in the detail that ensures an uber hawkish path in the latter half of the year.

Additionally, the minutes did not necessarily cement another sure 75 basis points as soon as July, leaving just a 50bp rate hike on the table still as well. While the minutes don't mention the word "recession," there was an acknowledgement that the interest rate hikes could have a bigger than anticipated dampening effect on the economy. Another hike this month was flagged but the Fed's chairman, Jerome Powell, would not commit to another 75 bp move in the presser at the June meeting.

However, according to CME Fed watch, the markets now see a 90.3% probability of another interest rate hike of at least 75 basis points at the conclusion of this month's two-day meeting, the last such meeting on the date book until the fall. This has supported the greenback which rose to fresh 20-year highs on Wednesday, sinking the euro that has tumbled to a new two-decade low. The dollar index (DXY), which tracks the greenback versus a basket of six currencies, burst through 107 the figure, sending the euro below 1.0200 vs the greenback for the first time since December 2002.

Fed bets tailing off?

Looking forward, the US dollar could struggle to extend gains in the Fed expectations alone, for which 50 bp hikes at the subsequent meetings November 2 and December 14 are moving towards 25 bp. Analysts at Brown Brothers Harriman explained that WIRP shows the beginning of an easing cycle by Q1 23. ''This is a much earlier timeframe for easing and one that we think is very, very premature since it would imply a recession hitting near the end of this year or early next year. The swaps market is now pricing in 175 bp of tightening over the next 6 months that would see the policy rate peak between 3.25-3.50%.''

Nevertheless, as analysts at TD Securities explained, ''gold is being weighed down by substantial CTA trend followers.'' The analysts explained that ''the massive amount of speculative length from proprietary traders in the yellow metal also appears complacent, given that this length was accumulated as early as 2020. In turn, they said, this ''suggests the bias remains to the downside in gold.''

Gold price analysis

Gold is trading below the rising supporting trendline on the monthly time frame but the critical fractal lows are located at $1,676.

Meanwhile, however, the price is reaching a key area on the daily chart where bulls will likely emerge. A correction to mitigate the imbalance of bids in this sell-off could see the yellow metal correct with a 50% mean reversion on the cards.

- Silver erases some earlier losses and advances more than 0.10% on Wednesday.

- The FOMC minutes showed the commitment of the Fed to tackle inflation, even if the economy slows down.

- The Fed might even get to a “more restrictive stance” if inflation persists.

- Fed policymakers reiterated that a 75 bps hike in July might be appropriate.

Silver (XAGUSD) bounced off the weekly lows around $18.92 and edged barely up during the North American session after the release of the US Federal Reserve June’s meeting minutes, showing that policymakers debated that a 50 or 75 bps would be appropriate at the July meeting. At the time of writing, XAGUSD is trading at $19.23.

Summary of the FOMC minutes

The Federal Open Market Committee’s tone was in line with expectations: hawkish. Policymakers stated that a 75 bps rate hike is warranted and noted that even a “more restrictive stance” could be appropriate if inflation prevails. Concerning economic growth, policymakers stated that risks to the economic outlook are skewed to the downside and also judged that uncertainty about economic growth over the next couple of years was elevated.

Silver’s reacted to the downside after the Fed released its minutes but made a U-turn and is trading in green territory. The US central bank’s commitment to bring inflation down would not deter them from hiking rates above neutral. Due to the tight labor market, they have room to spare before causing a jump in the Unemployment Rate, one of the consequences of a recession.

In the meantime, XAGUSD prices would remain downward pressured in the near term. The greenback remains buoyant in the session as portrayed by the US Dollar Index, up by 0.54%, above the 107.000 mark. US Treasury yields jumped on the release of the minutes, though the 2s-10s yield curve remains inverted, signaling that a recession could be around the corner.

Data-wise, the US calendar featured Services and Composite PMIs, unveiled by S&P Global and the US ISM. Figures exceeded expectations but trailed previous readings, signaling that the US economy is slowing down.

The week ahead, the US economic docket will feature ADP Employment Change, Initial Jobless Claims and Fed speakers on Thursday.

Silver (XAGUSD) Key Technical Levels

Reuters reports on an interview with IMF's Georgieva who says a global recession in 2023 cannot be ruled out.

''The head of the International Monetary Fund (IMF) on Wednesday said the outlook for the global economy had "darkened significantly" since April and she could not rule out a possible global recession next year given the elevated risks.

IMF Managing Director Kristalina Georgieva told Reuters the fund would downgrade in coming weeks its 2022 forecast for 3.6% global economic growth for the third time this year, adding that IMF economists were still finalizing the new numbers.

The IMF is expected to release its updated forecast for 2022 and 2023 in late July, after slashing its forecast by nearly a full percentage point in April. The global economy expanded by 6.1% in 2021.''

- IMF managing director Georgieva says can't rule out possible global recession in 2023.

- IMF's Georgieva says global economic outlook has 'darkened significantly' since last economic update in April.

- IMF's Georgieva says IMF will downgrade previous forecast for 3.6% growth in global economy in 2022 and 2023.

Market implications

The US dollar has been in demand this week as concerns mount about the global economy. DXY, a measure of the US dollar vs a basket of rival major currencies has rallied to a fresh cycle bull high:

(DXY monthly chart)

The Federal Open Market Committee has released a hawkish set of minutes of the June policy meeting.

Markets have nearly fully priced in another 75 basis points rate hike in July with which the minutes align with. Investors are paying closer attention to discussions around the September rate decision, however.

- See 50 or 75bps at the next meeting, July, as likely.

- Even more restrictive policy is possible in time.

- Fed's George was the only official not to back 75 basis points in June.

- 'Many' participants judged there was a 'significant risk' higher inflation could become entrenched if the public questions Fed's resolve.

- Participants 'concurred' that high inflation warranted 'restrictive' interest rates, with the possibility of a 'more restrictive stance' if inflation persists.

- The Fed expects inflation to remain above 2% for some time.

The US dollar is little changed after the minutes, trading at 107.00 and 0.48% higher on the day.

(5-min chart, DXY)

About the minutes

FOMC stands for The Federal Open Market Committee organizes 8 meetings in a year and reviews economic and financial conditions, determines the appropriate stance of monetary policy and assesses the risks to its long-run goals of price stability and sustainable economic growth. FOMC Minutes are released by the Board of Governors of the Federal Reserve and are a clear guide to the future US interest rate policy.

- The US dollar reached a 20-year high, around 107.264, weighing on the EUR/USD.

- Europe’s energy crisis takes center stage as prices soar, as countries like Germany and France scramble to ease the burden.

- The German Economy Minister Rober Harbeck said that current conditions could result in a recession.

The shared currency continued its collapse against the greenback, courtesy of recession fears in the Euro area, amidst an energy crisis that, if it aggravates, might cause a long-lasting economic contraction, as Russia threatens to halt natural gas flows to the bloc. At the time of writing, the EUR/USD s trading at fresh 20-year lows at 1.0175.

Negative mood and a strong US dollar, a headwind for the EUR/USD

A risk-off impulse favors safe-haven flows, meaning global equities are down and a stronger greenback. Recession fears appear to dissipate as traders brace for the release of the FOMC minutes. Softer US data revealed earlier showed that the US economy is slowing down, as illustrated by S&P Global and ISM Non-Manufacturing PMIs.

Alongside the previously mentioned factors weighing on the EUR/USD, China’s authorities reported that Shanghai recorded more than 100 positive cases, re-igniting fears of additional lockdowns. In the meantime, the European energy crisis aggravates as power prices skyrocket, courtesy of Russia’s tightening squeeze on energy supplies.

Germany Economy Minister Robert Habeck said that the current situation in Germany could result in a recession, according to Reuters. Meanwhile, the German government proposed an emergency law allowing the government to acquire shares of energy firms if they needed to be bailed out.

All the above-mentioned took their toll on the euro. EUR/USD Wednesday’s price action shows the major opening near the daily highs around 1.0264 and seesawed throughout the Asian session. When European traders arrived at their desks, the pair began nosediving and reached a fresh 20-year low at 1.0161.

In the week ahead, the EU economic docket will feature the German Industrial Production and ECB speaking led by ECB’s Philip Lane and Enria. Across the pond, the US calendar will unveil Initial Jobless Claims, ADP Employment Change, and Fed speakers, with Christopher Waller and St. Louis Fed President James Bullard crossing newswires.

EUR/USD Key Technical Levels

- GBP/USD holds near the lows of the week due to political turmoil.

- The BoE bets are being placed and weighed against Borish Johnson's survival rate and Brexit woes.

At 1.1928, GBP/USD is under water slightly, bleeding by 0.11% at the time of writing after sliding from a high of 1.1989 to a low of 1.1875 on the day so far and in the aftermath of yesterday's resignations of members of the Conservative party.

Health Minister Javid and Finance Minister Sunak resigned almost simultaneously out of dissatisfaction with UK PM, Boris Johnson's leadership. ''Replacements were immediately appointed in the persons of Barclay and Zahawi, but given the ongoing unrest, the question is how long they can enjoy their new office,'' analysts at Rabobank said. ''It could mean that the government will come up with popular measures, such as another tax cut, in an effort to regain the confidence of voters and party members.''

Sterling bears were hesitant to mark down the currency initially as the US dollar was drifting away from the fresh bull cycle highs made in the prior hours and earlier in the day. However, the currency fell to a fresh cycle low in London and again at the start of the New York session. Cable is now down nearly 12% against the dollar since the start of this year.

Nomura said on Wednesday it now expects sterling will slide in the coming months to its lowest level against the US dollar since 1985."We remain short GBP/USD in spot and now target 1.15 by end-July, towards 1.10 by end-September. With the U. becoming a key energy export partner for Europe this is leading to significant terms of trade shock to the benefit of USD." The analysts at Nomura also argue that the Bank of England also looked likely to disappoint investors betting on a 50-basis-point interest rate hike in August.

Casting minds back over the monetary policy path to date at The Old Lady, since December, the BoE has lifted the Bank Rate five times already. The market is pricing in 130bps of hikes over the next three meetings (August, September, and November), implying at least two meetings with 50bps hikes.

In other politics, an escalating row over Northern Ireland's status following Brexit could upend British trade ties with the European Union is also a weight on the currency. ''Uncertainties regarding red tape associated with Brexit and fear of a trade war with the EU over the Northern Ireland protocol are likely to be clouding the investment outlook,'' analysts at Rabobank said.

- The Loonie weakens in the week, weighed by a solid buck and falling energy prices.

- Global equities dropped, illustrating a dampened market mood, courtesy of recession fears and China’s Covid-19 outbreak.

- USD/CAD traders braces for FOMC June’s monetary policy minutes.

The USD/CAD rises for the second consecutive day, extending its weekly gains to almost 1.50%, courtesy of a buoyant greenback and falling crude oil prices. At the time of writing, the USD/CAD is trading at 1.3066, albeit in positive territory, shy of the YTD high around 1.3083.

USD/CAD falls on a risk-off mood, a solid buck, and falling oil prices

Sentiment stays negative as USD/CAD traders prepare to digest June’s Federal Reserve Open Market Committee (FOMC) minutes. During the New York Session, US Services and Composite-related PMIs, released by S&P Global and the Institute for Supply Management (ISM), beat expectations but trailed May’s reading, illustrating that the US economy is slowing down. Additionally, fears of a global recession, and China’s new coronavirus crisis, keep global equities under pressure, US Treasury yields climbing, and the US Dollar bid.

The US Dollar Index is gaining 0.66%, up at 107.194, underpinned by high US Treasury yields. Contrarily, the US crude oil benchmark, WTI, plunges 2.74% in the day, exchanging hands at $96.62 per barrel, a tailwind for the major.

All that said, investors’ eyes are focused on the Fed. Although it is usually an overvalued event, any hints that the US central bank could provide regarding forwarding guidance would be greatly appreciated by investors.

Meanwhile, money market futures began to show that traders expect the Fed to slash rates in the middle of 2023. Investors forecast a 75 bps rate hike for the July meeting, and the STIRs markets depict that the Federal funds rate (FFR) will peak at 3.25% before easing to 3.04% by June 2023.

In the week ahead, the Canadian docket will feature May’s Balance of Trade, Exports, and Imports. On the US front, the economic calendar will unveil Fed speakers – Christopher Waller and James Bullard –, US Initial Jobless Claims, and Nonfarm Payrolls.

USD/CAD Key Technical Levels

Citing three Conservative lawmakers, Reuters reported on Monday that the Conservative Party's 1922 Committee will hold an internal election of a new executive next Monday.

The new executive will decide whether to change the rules surrounding the grace period following the no-confidence vote.

Market reaction

The British pound is having a difficult time staging a recovery amid political jitters. The GBP/USD pair, which touched its lowest level since March 2020 at 1.1876 earlier in the day, was last seen losing 0.45% on the day at 1.1905.

British Prime Minister Boris Johnson said on Wednesday that he is not going to step down from his position and argued that the last thing the UK needs is an election, per Reuters.

Meanwhile, several news outlets are reporting that the Conservative Party's 1022 Committee have altered the rules around party leadership. This development suggests that Johnson could face another no-confidence vote regardless of the grace period.

Market reaction

These comments don't seem to be having a noticeable impact on the British pound's performance against its rivals. As of writing, the GBP/USD pair was down 0.45% on the day at 1.1902.

- JOLTS Job Openings declined by 427,000 in May.

- US Dollar Index clings to strong daily gains above 107.00.

The number of job openings decreased to 11.254 million in May from 11.681 million in April, the monthly Job Openings and Labor Turnover Summary (JOLTS) published by the US Bureau of Labor Statistics showed on Wednesday.

"Hires and total separations were little changed at 6.5 million and 6.0 million, respectively," the publication further read. "Within separations, quits (4.3 million) and layoffs and discharges (1.4 million) were little changed."

Market reaction

The US Dollar Index remains on track to post its highest daily close in nearly two decades above 107.00. Meanwhile, the S&P 500 Index was last seen losing 0.4% on the day.

German Economy Minister Robert Habeck said on Wednesday that the current situation in Germany could result in a recession, as reported by Reuters.

"The credit crunch could threaten the country's economic power," Habeck added. "What we're now doing is pretty close to an expropriation of companies."

On Tuesday, the German government proposed an emergency law that would allow the government to acquire shares of energy firms if they need to be bailed out.

Market reaction

The shared currency remains under constant bearish pressure on Wednesday and the EUR/USD pair was last seen losing 0.9% on the day at 1.0175.

- The non-yielding metal slips further as US bond yields recover from Tuesday’s session.

- US Global and ISM Services PMIs beat expectations but slowed compared to May’s readings.

- Gold Price Forecast (XAUUSD): Sellers stepped in and broke the $1750 price level, eyeing the next swing low at around $1720.

Gold price tumbles to fresh multi-month lows below $1752.51, amidst concerns of a global economic recession, but also driven down by a solid greenback, which remains to record new two-year highs as shown by the US Dollar Index, underpinned by rising US Treasury yields. At the time of writing, XAUUSD is trading at $1740.15 a troy ounce.

US Services PMIs beat expectations, but show signs of slowing down

A string of US economic data crossed newswires. The US ISM Non-Manufacturing PMI tripped to 55.3 in June from 55.9 in the previous reading, showing that growth eased but beat expectations of 54.3. in the same tone, the S&P Global Services and Composite PMIs exceeded expectations and trailed May’s figures.

According to Chris Williamson, Chief Business Economist at S&P Global, demand for goods and services shows signs of moderation blamed on high inflation. He added that “tighter financial conditions are starting to hit” and that the services index slowdown was led by a drop in financial services activity.

Meanwhile, US equities fluctuate as well as European ones. The US Dollar Index, a measurement of the greenback’s value vs. a basket of peers, clings above the 107.000 mark, gaining close to 0.60%, while the US 10-year Treasury yield trims Tuesday’s losses up at 2.878%, climbs seven bps.

Those abovementioned factors and rising US Real yields, as shown by US 10-year TIPS, yielding 0.608%, are a headwind for XAUUSD’s price. Gold’s Wednesday price action witnessed the yellow metal opening near the $1765 area and edged towards the daily high around $1772 before plunging toward $1749.

The US economic calendar will unveil the FOMC June minutes will be revealed, which will shed some forward guidance regarding future monetary policy decisions.

Gold Price Forecast (XAUUSD): Technical outlook

From a technical perspective, XAUUSD is still downward biased. Once the December 15 swing low at around $1752.35 was breached, the yellow metal sellers are eyeing a re-test of the September 29, 2021 low at $1721.52. Gold traders should note that oscillators are in oversold territory but showing no signs of turning the corner, as illustrated by the Relative Strength Index (RSI).

- ISM Services PMI edged lower in June, came in better than market expectation.

- US Dollar Index trades at its highest level in nearly two decades above 107.00.

The ISM Services PMI in June declined to 55.3 from 55.9 in May, showing that the business activity in the service sector expanded at a slightly softer pace. This print, however, came in better than the market expectation of 54.5.

The New Orders component of the survey fell to 55.6 from 57.6 and the Employment component slumped to 47.4, pointing to a contraction in service sector employment.

Assessing the findings of the survey, "the slight slowdown in services sector growth was due to a decline in new orders and employment," noted Anthony Nieves, Chair of the Institute for Supply Management Services Business Survey Committee. "Logistical challenges, a restricted labor pool, material shortages, inflation, the coronavirus pandemic and the war in Ukraine continue to negatively impact the services sector."

Market reaction

The US Dollar Index regained its traction after this report and was last seen rising 0.67% on the day at 107.20.

- EUR/GBP extends the weekly downside to 0.8540.

- Intense EUR sell-off weighs on the cross midweek.

- UK (still) PM B.Johnson could face another no-confidence vote.

Further weakness in the European currency now drags EUR/GBP to new 3-week lows in the 0.8540 region on Wednesday.

EUR/GBP looks to UK politics, EUR selling

EUR/GBP sheds ground for the third session in a row midweek, heavily influenced by the intense decline in the single currency in response to recession fears in the broader Euroland in combination with noticeable ECB inaction.

On the other side of the Channel, the sterling is expected to remain under scrutiny against the backdrop of mounting political effervescence, particularly exacerbated in response to several resignations from ministers of the government in the last hours and a most likely no-confidence vote against Boris Johnson as soon as tonight.

EUR/GBP key levels

The cross is losing 0.43% at 0.8547 and a breach of 0.8511 (low June 16) would expose 0.8485 (low June 9) and finally 0.8441 (200-day SMA). On the other hand, the next up barrier emerges at 0.8678 (monthly high July 1) followed by 0.8721 (2022 high June 15) and then 0.9085 (2021 high January 6).

- The AUD/USD is almost flat during the day, but risks are skewed to the downside.

- Concerns about a global economic recession prevailed; the greenback rose to a 52-week high, as the DXY broke above 107.000.

- Credit Suisse analysts see potential that the major could slip towards 0.6460s once it clears the 0.6757.

AUD/USD recovers from YTD lows reached on Tuesday, trimming some losses, but it remains at the lower end of the weekly range as the North American session begins. At 0.6800, the AUD/USD is barely flat.

Risk aversion emerges as Wall Street opens, and the greenback stays strong

Given the backdrop that concerns of a global economic slowdown persist, the US Dollar remains strong, putting a lid on the major. Talks between US and China policymakers earlier in the week appear to ease tensions between both countries. In fact, US President Joe Biden is assessing lifting some tariffs on Chinese goods and services imposed by the Trump administration.

Concerning China’s coronavirus crisis, during the Asian session, Shanghai reported more than 100 cases, and authorities ordered massive testing. That re-ignited fears of another lockdown in China’s second-largest city.

Those factors mentioned above, alongside tumbling Iron Ore prices, might keep the AUD/USD under pressure. In the meantime, the US Dollar Index, a gauge of the greenback’s value against a basket of peers, rises 0.44% to 106.969, a headwind for the AUD/SD. Further downward action is expected unless AUD/USD traders reclaim the 0.6900 figure.

At the time of writing, the US docket features the US S&P Global PMIs for June in Services and Composite, which beat expectations. The AUD/USD reacted downwards, from around the daily highs at 0.6826, towards 0.6804, putting the 0.6800 figure in sight.

Analysts at Credit Suisse see potential that the AUD/USD might reach 0.6461 once sellers clear 0.6757. “Support stays at the 50% retracement of the 2020/21 rise at 0.6757, a break below which is needed to enable a further downside to 0.6643 and 0.6609/00, with potential to reach the next key support at the 61.8% retracement at 0.6461 in due course.”

At 14:00 GMG, the US economic docket will feature the US ISM Non-Manufacturing PMIs, which would shed additional light on the status of the US economy. Later in the day, the FOMC minutes will be revealed, alongside the JOLTs Job Openings report.

AUD/USD Key Technical Levels

- USD/JPY edged lower on Wednesday, though lacked any follow-through selling.

- The USD surged to a fresh 20-year high and extended some support to the pair.

- A positive risk tone undermined the safe-haven JPY and also helped limit losses.

- Traders keenly await the FOMC meeting minutes before placing directional bets.

The USD/JPY pair struggled to capitalize on its modest gains recorded over the past two sessions and witnessed some selling on Wednesday. The pair maintained its offered tone through the early North American session and was last seen trading near the daily low, around the 135.00 psychological mark.

The recent sharp decline in the US Treasury bond yields resulted in the narrowing of the US-Japan rate differential. This, along with growing recession fears, offered support to the safe-haven Japanese yen

and exerted some downward pressure on the USD/JPY pair. The downtick could further be attributed to some repositioning trade ahead of the crucial FOMC meeting minutes, due later during the US session.

Fed Chair Jerome Powell reiterated last week that the US central bank remains focused on getting inflation under control and said the US economy is well-positioned to handle tighter policy. This, in turn, lifted bets for more aggressive rate hikes and continued lending support to the US dollar. Hence, investors will look for clues about the Fed's policy tightening path before placing fresh bets.

In the meantime, an extension of the recent strong USD bullish run to a fresh two-decade high should act as a tailwind for the USD/JPY pair amid signs of stability in the financial markets. Apart from this, a big divergence in the policy stance adopted by the Fed and the Bank of Japan supports prospects for the emergence of some dip-buying. This, in turn, warrants caution for bearish traders.

Technical levels to watch

- S&P Global Services PMI in the US fell modestly in June.

- US Dollar Index clings to strong daily gains near 107.00.

Business activity in the US service sector expanded at a softer pace in June than in May with the S&P Global Services PMI falling to 52.7 (final) from 53.4 in May. This print came in better than the flash estimate of 51.6.

Commenting on the data, "June saw signs of a broad-based weakening of the economy with demand now falling in both the manufacturing and service sectors," noted Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

"While the survey data point to a stalling of GDP at the end of the second quarter, a downshifting in the forward-looking new orders index and drop in companies' future output expectations hints at falling economic activity as we head through the summer," Williamson added.

Market reaction

The US Dollar Index showed no immediate reaction to this report and was last seen rising 0.45% on the day at 106.98.

Reuters reported that six further junior ministers, Kemi Badenoch, Neil O'Brien, Alex Burghart, Lee Rowley, Julia Lopez and Mims Davies, resigned from British Prime Minister Boris Johnson's government.

Meanwhile, several news outlets report that the 1922 Committee could change the rules as soon as this afternoon and trigger a no-confidence vote against PM Johnson before the end of the day.

Market reaction

GBP/USD managed to stage a recovery in the last hour but continues to trade in negative territory. As of writing, the pair was down 0.25% on a daily basis at 1.1927.

EUR/GBP is edging lower over the past few sessions, breaking the uptrend from April. Nonetheless, economists at Credit Suisse look for an eventual rise to the “neckline” to the 2020 top at 0.8861/76.

First support moves to 0.8524/11

“We stay biased higher over the next 2-4 weeks, with key resistance remaining at the recent and April 2021 high at 0.8722, with the 50% retracement of the fall from September 2020 at 0.8747. Beyond here in due course should then add weight to our view that a broader basing process is underway, with resistance seen next at the ‘neckline’ to the 2020 top and 61.8% retracement at 0.8861/76.”

“Next key support moves to 0.8524/11, which coincides with the rising 55-day average, which we would look to hold if reached to maintain our 2-4 week positive outlook.”

AUD/USD is still holding Credit Suisse’s prior technical objective at 0.6757. However, their analysts stay short-term bearish and see the potential to reach 0.6461 in due course.

Aussie is still attempting to break below 0.6757

“Support stays at the the 50% retracement of the 2020/21 rise at 0.6757, a break below which is needed to enable a further downside to 0.6643 and 0.6609/00, with potential to reach the next key support at the 61.8% retracement at 0.6461 in due course.”

“We look for near-term strength to ideally remain capped below the recent price highs at 0.6964/95. Above here would see scope to reach next resistance at the 55-day moving average at 0.7038.”

EUR/USD broke aggressively below key support at 1.0350/41 on Tuesday. This breakdown suggests a quick move over the next 2-4 weeks to 1.00/00.99, where analysts at Credit Suisse look for another phase of consolidation.

Opening up a move to parity

“EUR/USD has broken below key price support from the YTD and 2017 lows at 1.0350/41, which we view as a very important breakdown, suggesting further weakness over the next 2-4 weeks towardsh parity/0.99. Thereafter, our bias would be for another consolidation phase to emerge, similar to the one we saw in May/June. “

“The market should now ideally remain capped below 1.0341/66 in the short-term. Next resistance above here is seen at 1.0489, above which would point to a false breakdown and further ranging, which is not our base case in the short-term.”

US ISM Services PMI Overview

The Institute of Supply Management (ISM) will release the Non-Manufacturing Purchasing Managers' Index (PMI) - also known as the ISM Services PMI – at 14:00 GMT this Wednesday. The gauge is expected to edge lower to 54.5 in June from 55.9 in the previous month. Given that the Fed looks more at inflation than growth, investors will keep a close eye on the Prices Paid sub-component, which is expected to rise to 83.9 from 82.1 in May.

How Could it Affect EUR/USD?

Ahead of the key release, the US dollar built on the previous day's blowout rally and surged to a fresh two-decade high on Wednesday amid hawkish Fed expectations. Apart from this, the worsening global economic outlook underpinned the safe-haven buck and dragged the EUR/USD pair below the 1.0200 mark for the first time since December 2002.

Stronger-than-expected US macro data would reaffirm bets for more aggressive Fed rate hikes and push the US bond yields higher, along with the USD. Conversely, a softer reading is more likely to be overshadowed by concerns that a big jump in natural gas prices could drag the Eurozone economy faster and deeper into recession. This, in turn, suggests that the path of least resistance for the EUR/USD pair is to the downside.

Valeria Bednarik, Chief Analyst at FXStreet, offered a brief technical outlook and explained: “The EUR/USD pair is sharply down for a second consecutive day, and there are no technical signs of bearish exhaustion. In the daily chart, technical indicators are heading south pretty much vertically, entering oversold territory and reflecting persistent selling interest. The 20 SMA, in the meantime, accelerated south, currently at around 1.0470.”

“The near-term picture is bearish, as, in the 4-hour chart, technical indicators keep heading lower despite being at extreme oversold levels. At the same time, the pair is developing well below its moving averages, with the 20 SMA accelerating its decline and developing over 200 pips above the current level,” Valeria added further.

Key Notes

• EUR/USD Forecast: No rest for bears as panic persists

• EUR/USD Price Analysis: Parity at the end of the tunnel?

• EUR/USD Forecast: Sellers to retain control with a drop below 1.0200

About the US ISM manufacturing PMI

The Institute for Supply Management (ISM) Manufacturing Index shows business conditions in the US manufacturing sector. It is a significant indicator of the overall economic condition in the US. A result above 50 is seen as positive (or bullish) for the USD, whereas a result below 50 is seen as negative (or bearish).

- EUR/USD clinches new lows in the sub-1.0200 area.

- The pair enters oversold territory and could spark a bounce.

EUR/USD loses further ground and drops to nearly 2-decade lows in the 1.0170 region on Monday.

The sell-off in the pair stays everything but abated midweek amidst an increasing negative outlook. Against that, there is a minor support level at 1.0060 (low December 11 2002). The breakdown of the latter should herald a visit to the key parity area.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.1085.

EUR/USD daily chart

- Gold Price turned lower for the third straight day and refreshed YTD low on Wednesday.

- The USD gained strong follow-through traction and continued weighing on the commodity.

- Recession fears failed to lend support, though losses remain limited ahead of FOMC minutes.

Gold Price met with a fresh supply near the $1,773 region on Wednesday and drifted in negative territory for the third successive day. The intraday decline dragged the XAUUSD to a fresh YTD low, around the $1,760-$1,759 area during the early North American session and was sponsored by strong follow-through US dollar buying. In fact, the USD Index built on the previous day's blowout rally and surged to a fresh two-decade high amid aggressive Fed rate hike bets, which, in turn, undermined the dollar-denominated commodity. Bulls, so far, have failed to gain any respite from the prevalent risk-off environment, which tends to benefit the safe-haven precious metal. This, in turn, suggests that the path of least resistance for the yellow metal is to the downside.

Gold Price: Key levels to watch

The Technical Confluence Detector shows that the next relevant support for Gold Price is pegged near the $1,754-$1,753 region - Pivot Point One Month S2. This is closely followed by support near the $1,750 area - Pivot Point One Day S1. Failure to defend the said support levels would be seen as a fresh trigger for bearish traders and pave the way for a further near-term depreciating move.

On the flip side, the $1,765 region - the convergence of Previous Low One Day, Bollinger Band 15 Minutes Middle and SMA 5 One Hour - now seems to act as immediate resistance. Sustained strength beyond could trigger a short-covering move and lift Gold Price to the $1,780-$1,783 region - Pivot Point One Month S1, Bollinger Band One Day Lower and the Fibonacci 38.2% One Day.

Here is how it looks on the tool

About Technical Confluences Detector

The TCD (Technical Confluences Detector) is a tool to locate and point out those price levels where there is a congestion of indicators, moving averages, Fibonacci levels, Pivot Points, etc. If you are a short-term trader, you will find entry points for counter-trend strategies and hunt a few points at a time. If you are a medium-to-long-term trader, this tool will allow you to know in advance the price levels where a medium-to-long-term trend may stop and rest, where to unwind positions, or where to increase your position size.

Alvin Liew, Senior Economist at UOB Group, comments on the recently published PMI results in Singapore.

Key Takeaways

“Singapore’s manufacturing Purchasing Managers’ Index (PMI) edged slightly lower by 0.1 point to 50.3 in Jun, the 24th straight month where PMI stayed above the 50.0 mark, indicating an overall expansion in activity. The electronics sector PMI registered a surprise increase of 0.3 point to post a faster rate of expansion at 50.8, the highest level since Jan 2022.”

“Both the headline PMI and electronics PMI recorded faster expansion rates for new orders, new exports, factory output and imports index. It was also noted that their respective input prices index remained on a persistent upward trend while their employment index continued to expand but at a slower pace.”

“We continue to stay positive in our outlook for Singapore’s manufacturing sector (in particular, electronics) as it remains a key economic support pillar for the overall economy and for job creation. That said, we are mindful of the external risks due to the on-going Russia-Ukraine conflict and COVID-19 related supply chain disruptions. We are also keenly monitoring higher commodity prices (especially energy) which have persistently lifted the input prices index, which in turn would further add to inflation risks for the overall economy. In all, while we are cognizant of the attendant external risks and price pressures, the latest PMI outcome does not change our outlook for Singapore’s manufacturing which we expect to grow by an average of 4.5% in 2022.”

- DXY trades in cycle peaks north of the 107.00 mark.

- Extra gains look likely and target the 107.30 region.

DXY adds to the ongoing sharp uptick and leaves behind the 107.00 yardstick on Wednesday, or new YTD highs.

Further upside in the dollar remains in store in the short-term horizon. Against that, the index could now look to revisit the December 2002 top at 107.31 ahead of the October 2002 high at 108.74.

As long as the 4-month line near 102.60 holds the downside, the near-term outlook for the index should remain constructive.

The broader bullish view remains in place while above the 200-day SMA at 32.

Of note, however, is that the index trades in the overbought territory and thus could attempt a technical correction in the not-so-distant future.

DXY daily chart

Parliamentary Private Secretary Selaine Saxby announced her resignation via Twitter.

Private Parliamentary Secretary Claire Coutinho and Private Parliamentary Secretary David Johnston also stepped down from their positions, as reported by Reuters.

Meanwhile, when asked about the possibility of British Prime Minister Boris Johnson facing another no-confidence vote, the PM's spokesperson said that Johnson was confident that he still had the support of his backbench MPs. "There will be further appointments over the coming days," she added.

Market reaction

The GBP/USD pair stays under heavy bearish pressure on Wednesday and was last seen losing 0.6% on the day at 1.1885.

UOB Group’s Senior Economist Julia Goh and Economist Loke Siew Ting assess the latest inflation figures release in the Philippines.

Key Takeaways

“Headline inflation recorded a big jump to 6.1% y/y in Jun (from 5.4% in May), surpassing our estimate and Bloomberg consensus of a 6.0% gain. It also marked the highest inflation rate since Nov 2018, largely driven by costlier food, transportation and electricity amid a steep depreciation in Peso (PHP).”

“Inflation will remain elevated and above Bangko Sentral ng Pilipinas (BSP)’s medium-term target range of 2.0%-4.0% for the rest of the year and into 1H23. This is mainly due to higher global oil and non-oil prices, the continued shortage in domestic fish supply, pronounced second round effects on prices of domestic goods and services, as well as adverse weather. We maintain our full-year inflation forecasts at 5.0% for 2022 (BSP est: 5.0%, 2021: 3.9%) and 4.0% for 2023 (BSP est: 4.2%), with upward revision risks.”

“The higher-than-expected inflation outturn in Jun and persistent currency weakness have bolstered the case for a 50bps hike in the BSP rate next month (Aug). This follows new BSP Governor Felipe Medalla’s comments last Wed (29 Jun) that BSP opened the door to bigger rate hikes should the PHP overshoot and stoke imported inflation. Hence, the movement of the PHP in the next one and half months together with the next release of the nation’s CPI data (on 5 Aug) and 2Q22 GDP numbers (on 9 Aug), as well as FOMC’s rate decision on 27 Jul will be primary factors justifying the need for a more aggressive BSP rate hike at the upcoming Monetary Board meeting on 18 Aug, in which we keep our call for a 25bps hike to 2.75% at this juncture.”

"It is with sadness that I am resigning as Housing Minister," Conservative MP for Pudsey Stuart Andrew announced via Twitter on Wednesday.

Meanwhile, Sajid Javid, former British Health Minister who quit in protest at Prime Minister Boris Johnson on Tuesday, told Parliament that it had become increasingly difficult to be in PM's team.

"It's not fair on conservative voters who expect better standards," Javid added. "At some point, we have to conclude that enough is enough. That point is now."

Market reaction

GBP/USD stays under heavy bearish pressure on Wednesday and was last seen trading at its weakest level since March 2020 at 1.1877, losing 0.67% on a daily basis.

- GBP/USD met with a fresh supply on Wednesday and dropped to its lowest level since March 2020.

- The UK political drama, Brexit woes, expectations of a less hawkish BoE weighed on the British pound.

- Strong follow-through USD buying further contributed to the selling bias ahead of the FOMC minutes.

The GBP/USD pair struggled to capitalize on its early modest gains and attracted fresh selling in the vicinity of the 1.2000 psychological mark on Wednesday. The intraday decline dragged spot prices back below the 1.1900 mark, to the lowest level since March 2020 and was sponsored by a combination of factors.

The British pound was undermined by the UK political crisis, where British Prime Minister Boris Johnson faces mounting pressure to step down following the resignations of key Tory MPs. This comes amid worries that the UK government's controversial Northern Ireland Protocol Bill could trigger a trade war with the European Union. Apart from this, expectations that the Bank of England would adopt a gradual approach towards raising interest rates amid growing recession fears further weighed on sterling.

On the other hand, the US dollar built on the previous day's blowout and surged to a fresh two-decade high amid growing acceptance that the Fed would hike interest rates at a faster pace. In fact, Fed Chair Jerome Powell reiterated last week that the US central bank remains focused on getting inflation under control and that the US economy is well-positioned to handle tighter policy. This was seen as another factor that exerted downward pressure on the GBP/USD pair, though the downtick lacked strong follow-through selling.

Traders now seem to have moved to the sidelines and prefer to wait for the FOMC meeting minutes, due later during the US session. Market participants will look for fresh clues about the Fed's policy tightening path, which will influence the USD price dynamics and provide some impetus to the GBP/USD pair. In the meantime, traders will take cues from the US economic docket - featuring JOLTS Job Openings and ISM Services PMI.

Technical levels to watch

- EUR/JPY adds to the weekly leg lower and breaches 138.00.

- Further losses could retest the June low at 137.83.

EUR/JPY remains on the defensive and faces a deeper pullback in the short-term horizon.