- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- USD/CHF has picked demand after dropping below 0.9220 as volatility might trigger ahead of US GDP data.

- Tuesday’s upbeat preliminary US S&P PMI data failed to infuse confidence in the USD Index.

- Accelerating interest rates by the Fed is dampening firms’ production activities.

The USD/CHF pair has sensed buying interest after dropping below the critical support of 0.9220 in the early Asian session. The Swiss franc asset is gaining traction as investors are shifting their focus toward the release of the United States Gross Domestic Product (GDP) data, which is scheduled for Thursday.

S&P500 futures are displaying losses after Tuesday’s choppy trade, portraying a caution for the risk-sensitive assets. A decline in the risk appetite of the market participants has improved the appeal for safe-haven assets. The US Dollar Index (DXY) is building a cushion around 101.50 after a sell-off. The 10-year US Treasury yields are still hovering above 3.45%.

Tuesday’s upbeat preliminary United States S&P PMI data failed to infuse confidence in the USD Index for continuing its upside momentum. Manufacturing PMI landed at 46.8, higher than the expectations of 46.1 and the former release of 46.2. Also, the Services PMI remained upbeat and scaled higher to 46.6 against the consensus of 44.5 and the prior release of 44.7.

For further guidance, US GDP data will better guide USD/CHF for further action. As per the projections, a contraction is expected in preliminary GDP for the fourth quarter of CY2022 to 2.8% from 3.2% reported earlier. This could be the outcome of accelerating interest rates by the Federal Reserve (Fed), which has forced firms to dodge borrowings at a higher cost to avoid higher interest obligations.

On the Swiss Franc front, investors are awaiting the release of the ZEW Survey- Expectations (Jan), which will release on Wednesday. The economic data that display present business conditions and employment conditions is expected to trim to -47.6 from the former release of -42.8. A weaker-than-projected qualitative data could impact the Swiss Franc ahead.

Overview

The fourth quarter (Q4) release of the Australian Consumer Price Index (CPI), as well as the monthly CPI for December, scheduled for publishing on early Wednesday, appears the crucial data for the AUD/USD pair traders. The reason could be linked to the Reserve Bank of Australia’s (RBA) recent hesitance in defending the hawkish monetary policy, not to forget the downbeat Aussie pair’s trading near the multi-day high.

Not only the headline CPI Q4 and the monthly inflation numbers but the RBA Trimmed Mean CPI for Q4 also appears crucial to watch for the AUD/USD pair traders.

Forecasts suggest that the headline CPI is expected to ease to 1.6% QoQ versus 1.8% prior but the monthly CPI could rise to 7.7% YoY from 7.3% previous readings. Further details signal that the RBA Trimmed Mean CPI may inch up to 1.9% from 1.8%.

Ahead of the release, Analysts at the ANZ said,

The trimmed mean, non-tradables and services inflation are the key measures to watch. We expect all of these measures to have lifted strongly in Q4, and for trimmed mean inflation to rise to 6.7% y/y, exceeding the RBA’s forecast of 6.5% y/y.

On the same line, Westpac stated

We see Australia’s Q4 CPI. Robust gains in food prices, rising fuel prices and a bounce in holiday travel prices are all expected to continue pushing headline inflation higher, albeit at a slower pace than observed in the September quarter. Hence, Westpac anticipates a 1.5% and 1.6% lift for the headline and trimmed mean CPI measures respectively (market f/c: 1.6% and 1.5% respectively). The annual inflation rates we expect of 7.4% headline and 6.6% trimmed mean should be the cycle peak.

How could AUD/USD react to the news?

AUD/USD renews its intraday low near 0.7030 as it pares for the key data amid mixed sentiment during early Wednesday. In doing so, the Aussie pair also takes clues from the downbeat US stock futures and the Treasury bond yields to print mild losses.

That said, the Aussie pair is likely to witness profit booking should the Aussie inflation data disappoint as the RBA appears running out of steam to defend the hawkish interest rate moves. It should be noted that the RBA Trimmed Mean CPI will gain major attention and hence any minor change in the headline CPI data may not affect the AUD/USD to a much extent.

Technically, the 200-week Simple Moving Average (SMA) near 0.7070 appears the key hurdle for the AUD/USD buyers to watch in case of the pair’s further upside. Until then, the firmer RSI and looming bull cross on the daily chart, a condition when 50-DMA crosses the 200-DMA from below, can keep the buyers hopeful.

Key notes

AUD/USD Price Analysis: On the verge to test a five-month high around 0.7060 ahead of Australian CPI

AUD/USD buoyed by risk-appetite improvement climb above 0.7040s ahead of Aussie CPI

About Aussie Consumer Price Index

The quarterly Consumer Price Index (CPI) published by the Australian Bureau of Statistics (ABS) has a significant impact on the market and the AUD valuation. The gauge is closely watched by the Reserve Bank of Australia (RBA), in order to achieve its inflation mandate, which has major monetary policy implications. Rising consumer prices tend to be AUD bullish, as the RBA could hike interest rates to maintain its inflation target. The data is released nearly 25 days after the quarter ends.

- Gold Price remains mildly bid, mostly sidelined, during the sixth consecutive week of uptrend.

- Market’s cautious mood ahead of the next week’s Federal Reserve (Fed) meeting probes Gold buyers.

- United States Purchasing Managers Index for January failed to recall US Dollar buyers, allowing XAU/USD to remain firmer.

- US GDP could offer the last key signal ahead of Fed to Gold traders.

Gold price (XAU/USD) seesaws around $1,938 as bulls take a breather inside a bearish chart pattern during early Wednesday. In doing so, the bright metal depicts the market’s mixed feelings amid downbeat data from the United States, as well as the cautious mood ahead of the next week’s Federal Reserve (Fed) meeting. Even so, the US Dollar weakness and optimism surrounding Europe, as well as China, appears to favor the XAU/USD bulls.

Lack of clarity in the market probes Gold buyers

Although the Gold buyers keep the reins for the sixth consecutive week, the mixed signals from global markets and the Federal Reserve’s (Fed) silence period ahead of next week’s Federal Open Market Committee (FOMC) seem to restrict the XAU/USD moves. Also challenging the Gold traders could be the one-week-long holidays in China due to the Lunar New Year (LNY) celebrations. It’s worth noting that the European Central Bank (ECB) officials also sneak into the pre-monetary policy blackout starting today and adds barriers to the Gold price moves. While portraying the sentiment, the US 10-year Treasury yields dropped five basis points (bps) to 3.455% but Wall Street closed mixed.

Downbeat US Dollar favors XAU/USD bulls

Despite the mixed sentiment, the US Dollar weakness favors the Gold buyers due to the inverse relationship between the XAU/USD and the greenback. It’s worth noting that the US Dollar Index (DXY) remains indecisive near 101.90 after printing a two-week downtrend in the last. In doing so, the greenback’s gauge versus the six major currencies takes clues from the market’s bearish bias for the next week’s Fed meeting, as well as highlights the downbeat US data.

That said, preliminary readings of the US S&P Global Manufacturing PMI for January rose past 46.2 market forecast and 46.1 market expectations with 46.8 figure while the Services PMI followed the suit with the 46.6 figure for the said month, versus 44.5 forecast and 44.7 prior. That said, the S&P Global Composite PMI for January increased to 46.6 from 45.0 prior and the 44.7 consensus, marking the seventh consecutive read below 50.

Following the US data, the US Dollar Index (DXY) managed to rise for a brief time before closing in the red. The reason could be linked to the comments from Chief Business Economist at S&P Global Chris Williamson who said, “The US economy has started 2023 on a disappointingly soft note, with business activity contracting sharply again in January."

Considering the downbeat US data, markets widely anticipate a 0.25% Fed rate hike and the policy pivot in the next week. As a result, the Gold buyers appear pricing in the expected outcome.

Europe, China-linked optimism also strengthens Gold price

Even if China is off the market for the Lunar New Year celebrations, the positive vibes emanating from the reopening of the world’s largest commodity user keep Gold buyers hopeful. Also underpinning the XAU/USD upside could be the expectations of strong festive demand. It’s worth noting that the recent challenges to the US-China ties due to the alleged Chinese connection to the Russian war seem to probe the optimism.

Elsewhere, the latest activity data from Europe appear to help the traders optimistic about the old continent. That said, Eurozone S&P Global Manufacturing PMI crossed the 48.5 market forecasts and 47.8 previous readouts with 48.8 figure for January. Further, the Services PMI also impressed Euro bulls with 50.7 mark versus 50.2 expected 49.8 prior. With this, the Composite PMI for the bloc increased to 50.2 from 49.3 previous readings and 49.8 market forecasts. Following the data releases, Chris Williamson, Chief Business Economist at S&P Global said, “A steadying of the Eurozone economy at the start of the years adds to evidence that the region might escape recession.”

US Gross Domestic Product is the key

While the United States Durable Goods Orders and the second-tier employment data could also entertain the Gold buyers, major attention will be given to the first readings of the US Gross Domestic Product (GDP) for the fourth quarter (Q4). The reason appears logical due to the next week’s Federal Reserve (Fed) meeting, as well as the talks of the US recession. Forecasts suggest the world’s biggest economy eases with 2.8% annualized growth.

Also read: US Gross Domestic Product Preview: Three reasons to expect a US Dollar-boosting outcome

Gold price technical analysis

Despite the mildly bid performance of late, the Gold price stays inside a one-week-old rising wedge bearish chart pattern. The bearish bias also gains support from the Relative Strength Index (RSI) line, placed at 14, as well as the mixed signals from the Moving Average Convergence and Divergence (MACD) indicator.

As a result, the XAU/USD is likely to grind higher unless staying between $1,944 and $1,916 levels. However, the oscillators, namely the RSI and MACD, tease the bears and hence a downside break of $1,916 could gain more response than the otherwise conditions.

In that case, a one-month-old ascending trend line and the 100-Simple Moving Average (SMA), respectively near $1,896 and $1,890, will be crucial to watch before expecting the Gold price downside toward the theoretical target of $1,870.

On the flip side, a successful break of $1,944 will defy the bearish chart pattern and could propel the XAU/USD toward March 2022 peak surrounding $1,966.

Should the Gold buyers keep the reins past $1,966, the odds of witnessing the $2,000 on the chart can’t be ruled out.

Gold price: Four-hour chart

Trend: Further weakness expected

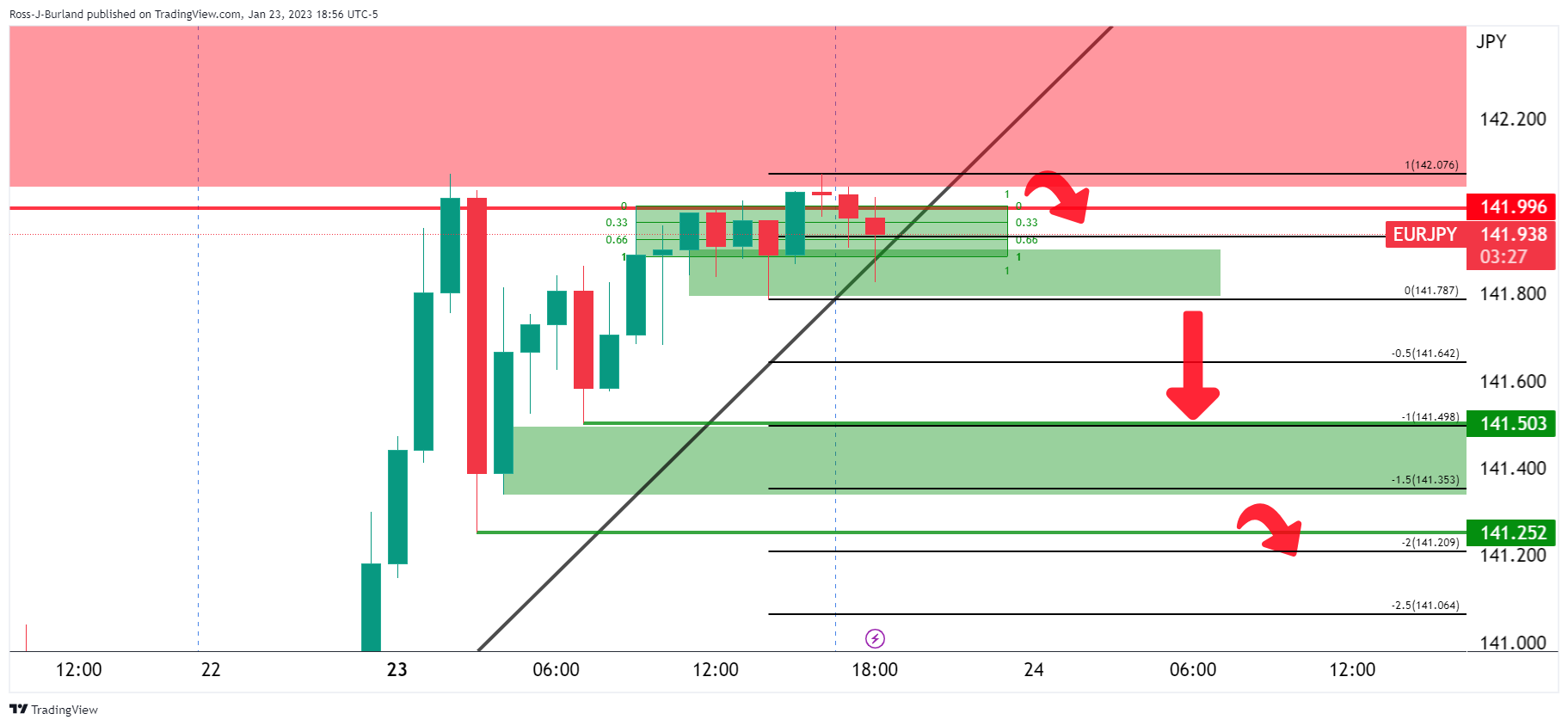

- EUR/JPY forms a hanging man as it fails to conquer the 100-day EMA, suggesting further downside is expected.

- EUR/JPY Price Analysis: The pair would be bearish below 141.00; otherwise, it could challenge 142.00.

EUR/JPY snapped two days of consecutive gains and retraced some of its gains as the EUR/JPY clashed with the 100-day Exponential Moving Average (EMA) at 141.83 but could not crack it. Therefore, the cross dived beneath the latter, with Tuesday’s session closing at 141.65. As the Asian session begins, the EUR/JPY is trading at 141.62, registering minuscule losses of 0.04%.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY remains sideways, even though the pair reached a two-week high at 142.20. Although the EUR/JPY recovered 2% since last Friday, Tuesday’s price action formed a hanging man, suggesting the exchange rates would aim lower. Nevertheless, the EUR/JPY would face a confluence of support areas, like two previous downslope resistance trendlines, around 141.00. Once those trendlines are broken, the next zone of demand tested would be the 20-day EMA at 140.79, ahead of the 200-day EMA at 140.20

However, if buyers can hold above 141.00, a retest to the 100-day EMA at 141.73 is on the cards. A decisive break would expose the 142.00 psychological figure, followed by the January 11 high at 142.85.

EUR/JPY Key Technical Levels

- EUR/USD is eyeing to recapture the 1.0900 resistance as ECB might not pause policy tightening beyond summer.

- The Euro is delighted with bullish bets for CY2023 as the ECB will continue to raise interest rates further.

- According to the consensus, investors should brace for a contraction in the US GDP for the fourth quarter of CY2022.

The EUR/USD pair is aiming for a recovery extension to near the critical resistance of 1.0900 as the odds of hawkish European Central Bank (ECB) bets are soaring dramatically. The major currency pair is looking to extend its upside journey further as the expectations of the continuation of policy tightening by the ECB beyond summer have strengthened.

Earlier, ECB President Christine Lagarde and other policymakers were stating that the central bank will reach an interest rate peak by the end of summer at 3.25%.

ECB policymaker Gediminas Simkus said on Tuesday that the ECB should continue with 50 basis points (bps) rate hikes amid growing wage pressures, as reported by Bloomberg. Simkus further added that reaching the peak policy rate before summer 'may be unlikely' and noted that the strong core Consumer Price Index (CPI) shows that their battle against inflation is not over yet.

Meanwhile, the street has started delivering bullish projections for the Euro for CY2023 considering the fact the ECB will continue to raise interest rates further. According to economists at CIBC Capital Markets, “The improved macro backdrop comes as the ECB now details that ‘rates will still have to rise significantly at a steady pace to reach levels that are sufficiently restrictive to ensure a timely return of inflation to the 2% medium-term target.’’

The market mood seems neutral as S&P500 remained choppy in Tuesday’s trade ahead of the United States Gross Domestic Product (GDP) data. However, weakness in the 10-year US Treasury yields to near 3.45% and in the US Dollar Index (DXY) to 101.50 support indicate that the risk-perceived currencies could remain in a positive trajectory ahead.

According to the consensus, the annualized GDP is seen lower at 2.8% vs. the prior release of 3.2%. An expression of a contraction in overall economic activities might accelerate recession fears in the United States.

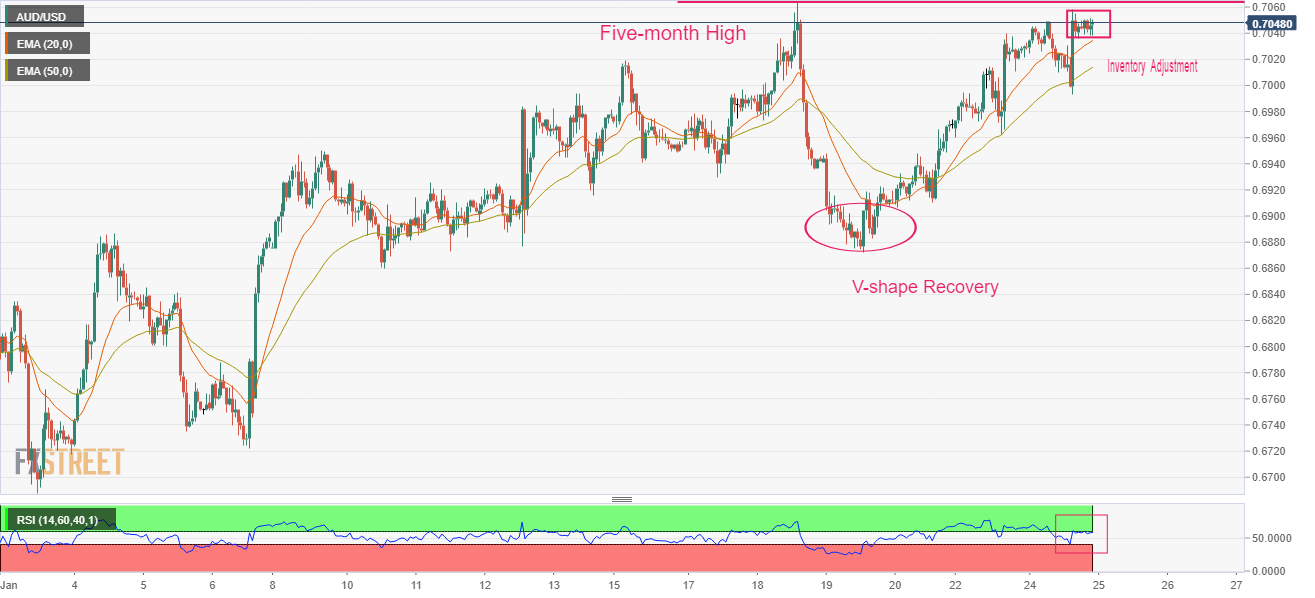

- AUD/USD is aiming to print a fresh five-month high above 0.7060 ahead of Australian inflation.

- The USD Index has found an intermediate cushion around 101.50, however, the downside bias is still solid.

- A bullish momentum will be triggered after a jump by the RSI (14) into the bullish range of 60.00-80.00.

The AUD/USD pair is juggling in a narrow range above the crucial support of 0.7040 in the early Asian session. The Aussie asset is on the verge of hitting a five-month high at 0.7060 ahead of the release of the Australian Consumer Price Index (CPI) data. The consensus claims an escalation in the annual inflation to 7.5% from the prior release of 7.3%. While monthly inflation is seen sharply higher at 7.7% from the former release of 7.3%.

Investors’ risk appetite has improved again as S&P500 futures have recovered their marginal losses witnessed on Tuesday. The US Dollar Index (DXY) has found an intermediate cushion around 101.50, however, the downside bias is still solid.

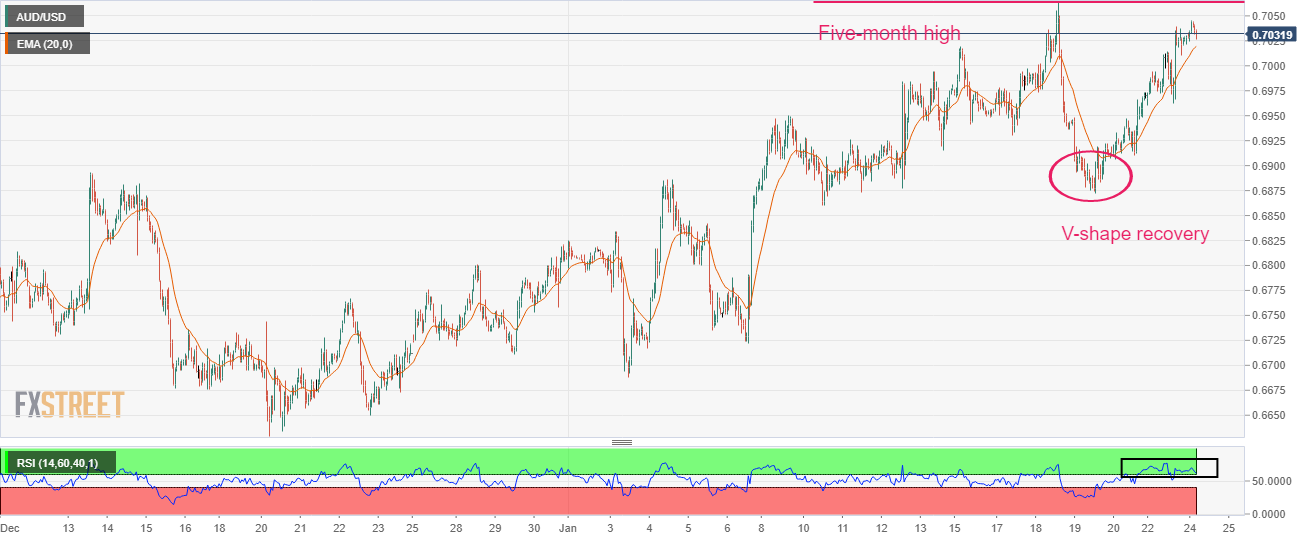

AUD/USD is marching towards the five-month high plotted from January 18 high at 0.7064 on an hourly scale. The Aussie asset displayed a V-shape recovery from January 19 low around 0.6875, which provides confidence that bullish momentum is present in the current trend.

Upward-sloping 20-and 50-period Exponential Moving Averages (EMAs) at 0.7035 and 0.7014 respectively, add to the upside filters.

What is interesting in the current scenario is the inventory adjustment phase below the critical resistance of 0.7060. This seems to be an inventory accumulation in a bullish trend, which favors the continuation of the upside journey after the conclusion.

Also, the Relative Strength Index (RSI) (14) is looking to shift into the bullish range of 60.00-80.00, which will trigger the bullish momentum.

For more upside, the Aussie asset needs to surpass the five-month high around 0.7060 decisively, which will drive the major towards August 11 high at 0.7137. A breach of the latter will expose the asset to the round-level resistance at 0.7200.

On the contrary, a downside move below December 29 low at 0.6710 will drag the major further toward December 22 low at 0.6650 followed by November 21 low at 0.6585.

AUD/USD hourly chart

- USD/CAD holds lower ground on the Bank of Canada interest rate announcement day.

- Sluggish MACD, sideways performance near 38.2% Fibonacci retracement challenge bears.

- Convergence of 200-day EMA, support line from early June portrays strong support.

- Buyers need to cross descending resistance line from mid-October 2022.

USD/CAD portrays the typical pre-event anxiety as it makes rounds to 1.3370-60 during early Wednesday in Asia. In doing so, the Loonie seesaws near the 38.2% Fibonacci retracement level of the Loonie pair’s April-October upside amid the sluggish MACD signals.

It’s worth noting, however, that the USD/CAD pair appears clubbed between the 1.3250 support confluence and the descending resistance line from October 2022 near 1.3610. That said, the 200-day Exponential Moving Average (EMA) joins ascending trend line from June to highlight the 1.3250 as the short-term key support level.

Given the Bank of Canada’s (BoC) 0.25% rate hike already priced-in, the USD/CAD bears need either hawkish remarks from the BoC statement or the higher rate increase to extend its downturn.

Also read: Bank of Canada Preview: The final one, with a pause ahead?

In that case, the 1.3250 support confluence will gain the market’s attention, a break of which could direct the USD/CAD bears towards the 50% and 61.8% Fibonacci retracement levels, respectively near 1.3190 and the 1.3000 psychological magnet.

Alternatively, the previous weekly high of 1.3520 could gain the USD/CAD buyer’s attention in case of the pair’s recovery post-BoC.

Even so, a convergence of the multi-day-old resistance line and the 23.6% Fibonacci retracement level could challenge the Loonie pair’s further upside near 1.3610.

USD/CAD: Daily chart

Trend: Further downside expected

- Silver recovered some bright on Tuesday and gained 0.90% after plummeting more than 1% on Monday.

- XAG/USD Price Analysis: Rally capped at the 20-day EMA.

Silver price recovers some ground and is back above Monday’s daily close, still struggling to break the 20-day Exponential Moving Average (EMA) at $23.67 a troy ounce. However, it trimmed some losses after nosediving sharply underneath the 50-day EMA and reaching a 5-day low of $22.76. The XAG/USD is trading at 23.64, up by 0.85%, as of typing.

Silver Price Analysis: Technical outlook

After visiting the 50-day EMA, XAG/USD resumed its uptrend, though it encountered solid resistance in the form of the 20-day EMA at 23.67. Nevertheless, bulls could remain hopeful that XAG/USD could continue to rise further as it reclaimed a three-week upslope support trendline around $23.40s.

Looking ahead, if Silver’s prices break above the 20-day EMA, that could open the door for further upside, exposing crucial resistance levels. Firstly, the psychological $24.00 a troy ounce, followed by the YTD high of $24.54. A breach of the latter and the $25.00 figure is up for grabs.

Otherwise, the XAG/USD first support would be $23.40. Once cleared, sellers would likely mount and drag prices to the 50-day EMA at $22.99. A decisive break could send the XAG/USD sliding toward December’s 16 daily low at $22.56.

Silver Key Technical Levels

- GBP/USD is looking to surpass 1.2350 after a recovery move amid a risk-on market mood.

- The USD Index has been weighed down by weaker US yields as the odds of a slowdown in the Fed’s policy tightening are solid.

- This week, the release of the US GDP data will be of utmost importance.

The GBP/USD pair is looking to extend its recovery move above the immediate resistance of 1.2340 in the early Tokyo session. The Cable delivered a V-shape recovery on Tuesday after S&P reported better-than-projected preliminary United States PMI data (Jan). It seems that the street was expecting an upbeat performance and therefore supporting the US Dollar Index (DXY) earlier. But later on, dumped the USD Index as a ‘Buy on rumor and sell on news’ indicator was triggered.

S&P500 futures remained choppy on Tuesday and settled with a marginal loss. However, the 500-US stock basket futures have recovered their marginal loss now and portraying a recovery in the risk appetite theme. The return generated by the 10-year US government bonds slipped sharply to 3.45% as the odds of a slowdown in the pace of policy monetary policy tightening are extremely solid.

United States Manufacturing PMI landed at 46.8, higher than the expectations of 46.1 and the former release of 46.2. Also, the Services PMI remained upbeat and scaled higher to 46.6 against the consensus of 44.5 and the prior release of 44.7. The release of the better-than-anticipated US PMI has trimmed recession fears for a while.

For further guidance, investors will focus on the release of the preliminary US Gross Domestic Product (GDP), which is scheduled for Thursday. As per the projections, the annualized GDP is seen lower at 2.8% vs. the prior release of 3.2%. An expression of a contraction in overall economic activities might accelerate recession fears again on a broader basis.

On the United Kingdom front, investors are awaiting the release of the Producer Price Index (PPI) (Dec) data. As per the consensus, the core PPI output is seen higher at 13.9% vs. the former release of 13.3%. Shortage of labor and rising wages for addressing the former could be the reason behind rising prices of goods and services at factory gates.

- NZD/USD pops 25 bps on upbeat New Zealand Q4 Consumer Price Index.

- NZ CPI came in 7.2% YoY, 1.2% QoQ versus 7.1% and 1.3% expected respectively.

- US PMIs failed to impress US Dollar for long as Composite PMI marked seven-month downtrend.

NZD/USD begins Wednesday’s trading on a firmer footing on upbeat New Zealand (NZ) inflation data, initially poping up to 0.6525 before retreating to 0.6500 by the press time. Adding strength to the Kiwi pair’s run-up could be the US Dollar’s failure to keep the late Tuesday’s gains amid dovish bias for the Federal Reserve’s next move.

NZ Consumer Price Index (CPI) for the fourth quarter (Q4) rose past 7.1% YoY market forecast to reprint the 7.2% figures while the QoQ data suggests a 1.4% number against 1.3% expected and 2.2% prior. It’s worth noting that the Reserve Bank of New Zealand (RBNZ) anticipated 7.5% yearly inflation in its November meeting.

Also read:

On the other hand, preliminary readings of the US S&P Global Manufacturing PMI for January rose past 46.2 market forecast and 46.1 market expectations with 46.8 figure while the Services PMI followed the suit with the 46.6 figure for the said month, versus 44.5 forecast and 44.7 prior. That said, the S&P Global Composite PMI for January increased to 46.6 from 45.0 prior and the 44.7 consensus, marking the seventh consecutive read below 50.

Following the US data, the US Dollar Index (DXY) managed rise for a brief time before closing in the red. The reason could be linked to the comments from Chief Business Economist at S&P Global Chris Williamson who said, “The US economy has started 2023 on a disappointingly soft note, with business activity contracting sharply again in January."

That said, receding odds of the Federal Reserve's (Fed) hawkish play in the next week’s monetary policy meeting, mainly due to the recently downbeat US data seemed to have weighed on the US Treasury bond yields, as well as the US Dollar. It should be noted that the mixed earnings report and sentiment portrayed Wall Street’s mixed close on Tuesday.

Having witnessed the initial reaction to New Zealand inflation data, which is not much alarming, the NZD/USD pair traders may wait for Australia’s CPI and NZ Credit Card Spending data for December for immediate directions.

Technical analysis

A six-week-old ascending resistance line near 0.6535 restricts immediate NZD/USD upside amid nearly overbought RSI conditions.

The Consumer Price Index released by the Statistics New Zealand is out as follows:

- New Zealand Q4 inflation 1.4% QoQ (expected 1.3%) 7.2% YoY (expected 7.1%)

New Zealand's consumer price index (CPI) rose 1.4% in the fourth quarter on the prior quarter, above analysts' forecasts. This compares with a 2.2% rise in the previous quarter. Annual inflation remained stable at 7.2%. Economists polled by Reuters had forecast a 1.3% rise for the quarter, with an annual rise of 7.1%.

NZD/USD rallied to test the 0.6520s.

About NZ CPI

With the Reserve Bank of New Zealand's (RBNZ) inflation target being around the midpoint of 2%, Statistics New Zealand’s quarterly Consumer Price Index (CPI) publication is of high significance. The trend in consumer prices tends to influence RBNZ’s interest rates decision, which in turn, heavily impacts the NZD valuation. Acceleration in inflation could lead to faster tightening of the rates by the RBNZ and vice-versa. Actual figures beating forecasts render NZD bullish.

Here is what you need to know for January 25:

The US Dollar edged lower against the euro and was vulnerable across the board despite solid US manufacturing data that gave some life to otherwise consolidative markets ahead of key events for the days ahead. The markets are in anticipation of inflation data from the antep[iodeans and the US on Thursday as well as growth updates for the US economy.

Firstly, eurozone business activity made a surprise return to modest growth in January, which helped to boost the Single currency. EUR/USD was 0.09 % higher at $ 1.0881, just shy of the 9-month high of $ 1.0927 touched on Monday backed by survey data supporting the view that the eurozone economy was fairing well despite intense price pressures. At the start of the week, the euro was bid on the back of European Central Bank (ECB) officials suggesting that the ECB is set to raise interest rates by 50 basis points in both February and March and will continue to raise rates in the months after.

The US Dollar rose to a near 1-week high against the yen, before giving up those gains but staying above its weakest since May which it visited ahead of a Bank of Japan policy review. However, the BoJ left policy unchanged enabling a move higher in USD/JPY that touched 131.11 on the day.

GBP/USD was one of the worst-performing pairs and dropped by 0.34 % on the day to 1.2263 after a survey showed British private-sector economic activity fell at its fastest rate in two years in January.

USD/CAD was ending near flat on the day after travelling between a low of 1.3346 and a high of 1.3413 so far while US stocks have been volatile making for choppy trading conditions in the forex space on Tuesday.

Meanwhile, the US 10-year yield was 4bp lower at 3.47% and WTI was down 1.8% at USD80.15/bbl. Gold dropped 0.3% to $1,933.3/oz. Bitcoin was little changed on the day at $22,973, steadying after having jumped by about a third in value since early January.

For the day ahead, Aussie and New Zealand inflation data will be key.

- EUR/USD bullish rally has faded and a topping pattern is in play.

- There is a bearish bias while EUR/USD remains below 1.0950.

As per the pre-open analysis at the start of this week, when there were reports by Reuters that the European Central Bank (ECB) officials were suggesting that the ECB is set to raise interest rates by 50 basis points in both February and March and will continue to raise rates in the months after, the euro has stuck tot he forecasted schematic as follows:

EUR/USD prior analysis

(Bearish schematic could be playing out)

It was stated that the Euro was in the barroom brawl, chopping around support and resistance. The analysis argued that if the bulls commit, then the 1.0870/90s and potentially the 1.09 psychological level could be attractive to the bears who are in anticipation of a premium for the opening sessions of the week.

EUR/USD update

The bullish rally has faded. There is still plenty to go, however, until critical US calendar events and the US dollar remains capped at resistance. Therefore, there are no dramatic moves expected over the course of the day ahead Nevertheless, a topping pattern is in play in EUR/USD and that leaves the bias to the downside while below 1.0950.

- Gold price is running into a critical resistance area on the charts.

- A sell-off in Gold price and capitulation of the bulls could lead to a significant run towards $1,900.

The Gold price is making progress on the day into the final push on Wall Street and rallied from a low of $1,917.22 to a high of $1,942 on the day so far.

Gold price rose to the highest in nine months as the US Dollar and bond yields came under pressure following the start of the week's 1% drop in leading economic indicators in December which solidified the dovish sentiment surrounding the Federal Reserve, Fed, that is now expected to announce another interest-rate hike when its policy committee meets next week.

The US Dollar was weakening, making the metal more affordable for international buyers while the Fed officials are out on the blackout week ahead of the highly anticipated Fed interest rate decision. the Gold price flourished with investors now awaiting US economic data due this week that could impact the Federal Reserve's policy path.

Federal Reserve is eyed, sentiment mixed

Investors are banking on the Federal Reserve raising rates by 25 basis points (bps) at the January 31 - February 1 policy meeting, after slowing its pace to 50 bps in December, following four straight 75-bp hikes. Meanwhile, the Gold price tends to benefit due to lower interest rates that otherwise decrease the opportunity cost of holding the non-yielding asset.

The most hawkish of comments came from St. Louis Federal Reserve's President James Bullard who said US interest rates have to rise further to ensure that inflationary pressures recede.

''We’re almost into a zone that we could call restrictive - we’re not quite there yet,” Bullard said Wednesday in an online Wall Street Journal interview. Officials want to ensure inflation will come down on a steady path to the 2% target. “We don’t want to waver on that,” he said.

“Policy has to stay on the tighter side during 2023” as the disinflationary process unfolds, Bullard added.

Bullard has pencilled in a forecast for a rate range of 5.25% to 5.5% by the end of this year.

However, economic reports, such as Producer Price Index and Retail Sales have recently shown disinflationary tendencies, reinforcing expectations that the Fed will continue to reduce its tightening pace in upcoming meetings.

With that being said, analysts at ANZ Bank recently wrote a note, entitled, ''Fed tightening not done yet.''

''So far in early 2023, US data releases have indicated a mild easing in inflationary pressures and softer demand. This indicates the Fed’s aggressive tightening last year is starting to take effect,'' the analysts explained. ''Weakness in housing is evident (existing home sales fell 17.8% last year), manufacturing activity has faltered and Retail Sales are returning to trend.''

Meanwhile, analysts at Brown Brothers Harriman have also of the opinion that the market is underestimating the potential for a higher for longer Federal Reserve. ''Core Personal Consumption Expenditures, PCE, has largely been in a 4.5-5.5% range since November 2021,'' they said. ''We think the Fed needs to see further improvement before even contemplating any sort of pivot.''

EUR/USD and Europen Central Bank sentiment in the mix

Meanwhile, the Euro has been a little cheerier of late, also pressuring the US dollar and helping to support risk appetite and a bid into the Gold price. European Central policymaker, Peter Kazimir, said on Monday that inflation easing was good news but added that it was not a reason to slow the pace of interest rate hikes, as reported by Reuters.

Governing Council member and Governor of Austria's central bank Olli Rehn made some comments on the European Central Banks' interest rates policy during their appearances over the weekend also as did ECB governing council member Klaas Knot on Sunday, advocating steep rate hikes. "Expect us to raise rates by 0.5% in February and March and expect us to not be done by then and that more steps will follow in May and June," Knot said.

Analysts at TD Securities argued that the gold price could struggle to firm further in the absence of the single-largest buyer of gold over the past months. On the downside, a break below the $1,900/oz range is required to spark trend-follower liquidations.

Gold technical analysis

The Gold price is on track for a crash should the US dollar bust to life given the placement of the price in the market structure. The US Dollar has been testing the daily trendline resistance as follows:

If this were to break then the Gold price will likely be headed lower, but there is red news scheduled for Thursday so any moves prior to that might be limited and a distribution schematic and higher highs could be more likely in the lead up:

Bullish trendline for Gold price is vulnerable.

A break of Gold price structures is eyed for the days ahead so long as resistance holds.

A sell-off and capitulation of the Gold price bulls could lead to a significant run towards $1,900.

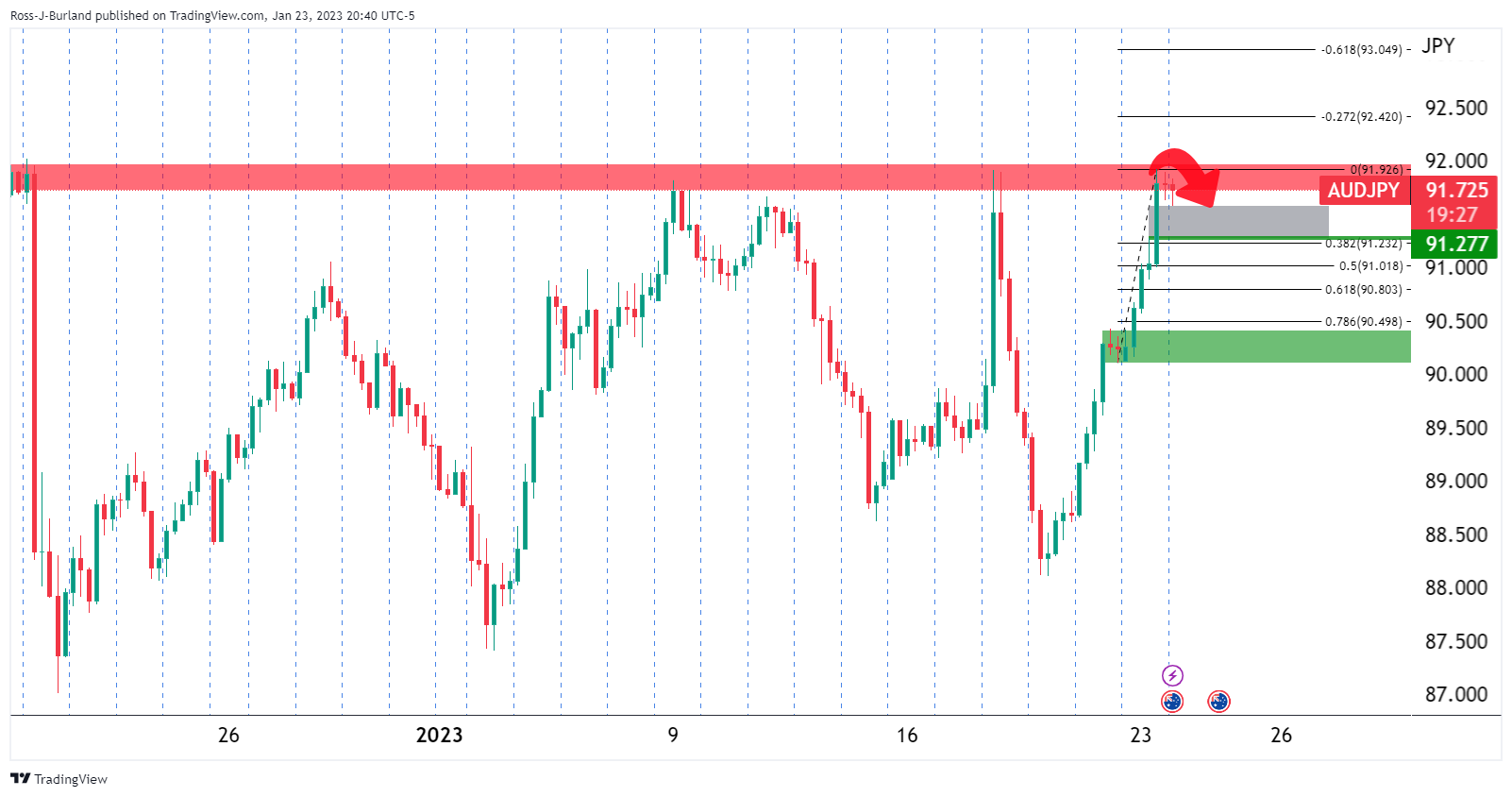

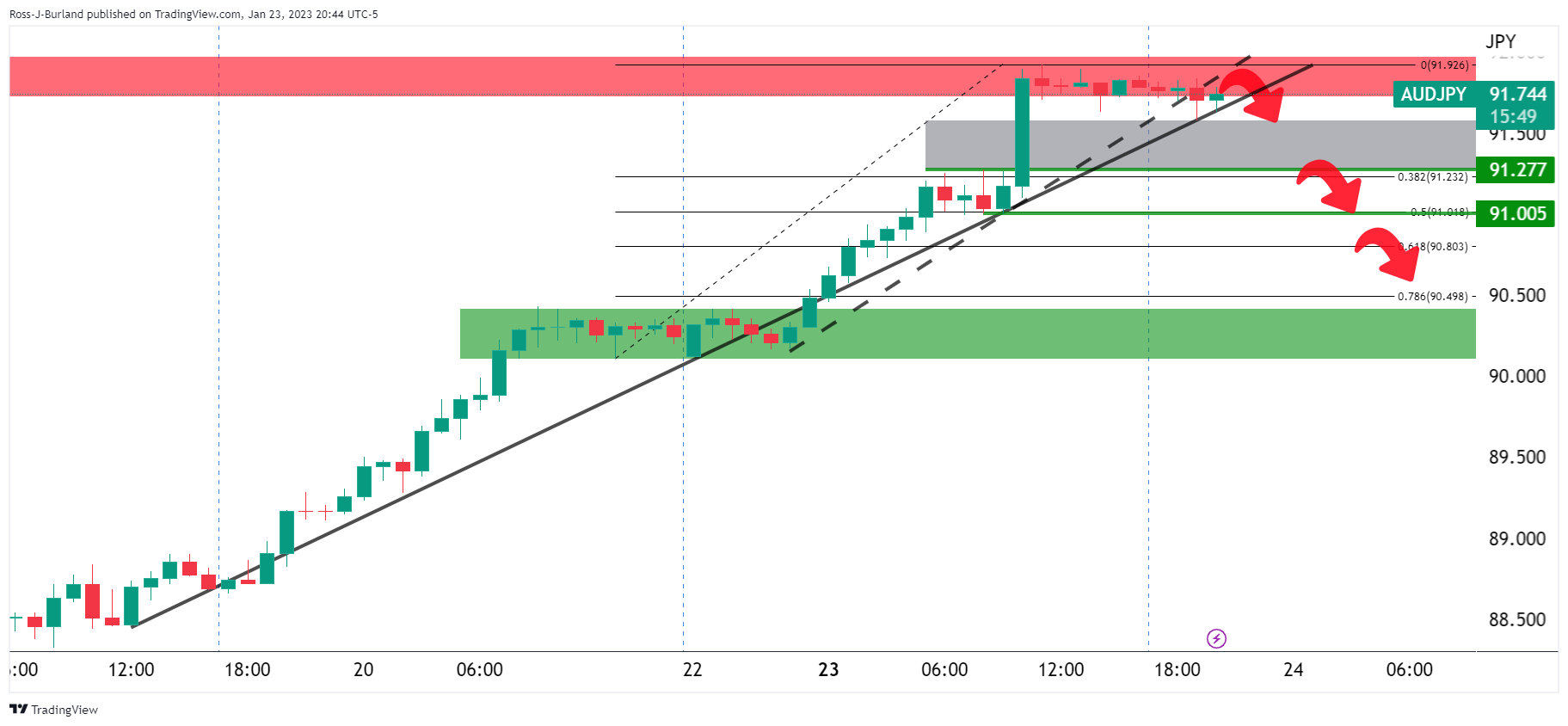

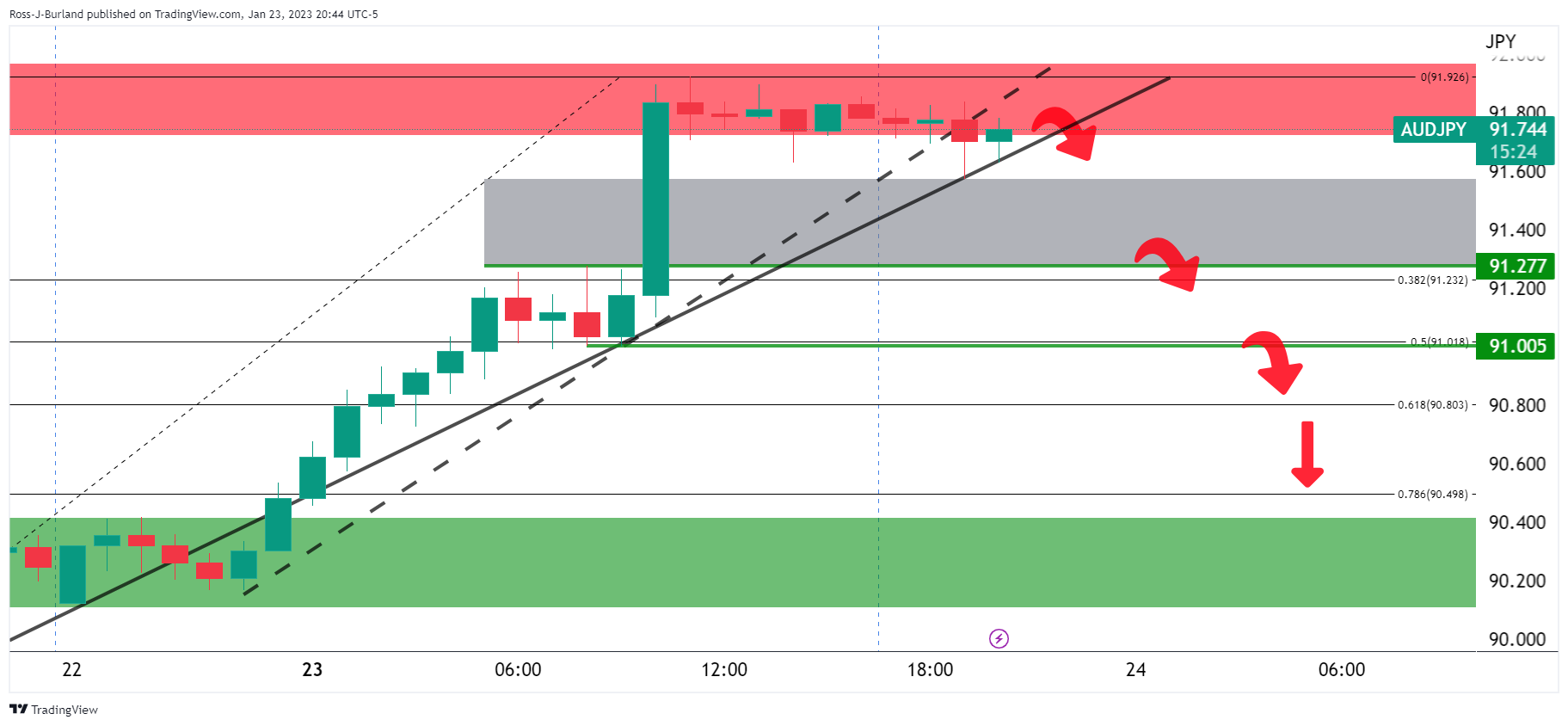

- AUD/USD prolonged its rally to three straight days, though Wednesday’s Aussie inflation data could rock the boat.

- US S&P Global PMIs remained in contractionary territory but came better than expected.

- AUD/USD Price Analysis: To extend its uptrend once it reclaims 0.7070.

The AUD/USD remains firm late in the New York session, albeit a mixed market mood keeps traders bracing for safe-haven assets. The US Dollar (USD) has recovered some ground late in the session, putting a lid on the AUD/USD steadily advance. At the time of writing, the AUD/USD is trading at 0.7045.

AUD/USD climbs sharply ahead of Australia's inflation data

Wall Street remains mixed, as shown by the Dow Jones Industrial, remaining firm, while the S&P 500 and the Nasdaq fluctuate. The US economic calendar featured a business activity report issued by S&P Global. US December’s PMIs improved, with the Services PMI jumping to 46.6 vs. 44.7 expected, while Manufacturing PMI advanced to 46.8 vs. estimates of 46.2.

The S&P Global Composite, which measures both indices, climbed 46.6, higher than the foreseen 45 figure. It should be said that even though business activity continues to deteriorate in the US economy, the downward trend moderated some.

On the Australian side, the docket will feature inflation data. According to Reuters, expectations for the Consumer Price Index (CPI) for Q$ are 1.6%, while on an annual basis, it meanders at 7.5%. Analysts at TD Securities noted that “the trimmed measure that will draw more attention. TD is at 1.6% q/q vs. the RBA, and consensus at 1.5% q/q. Our forecast pegs annually trimmed to hit the highest levels since 1990 at 6.6% vs. the RBA and consensus at 6.5%, above the prior 6.1% y/y print. We expect annual trimmed between 6.1% and 6.5% to lock in a 25bps hike next month.”

AUD/USD Technical Analysis

The AUD/USD daily chart portrays the pair as upward biased. The pair managed to record gains in three consecutive days, though it had struggled to surpass the January 18 daily high of 0.7063. Nevertheless, the AUD/USD bias remains upward for some reasons: the 20-day Exponential Moving Average (EMA) crossed above the 200-day EMA, while the 50 and 100-day EMAs are closing by. In addition, the Relative Strength Index (RSI) remains in bullish territory. Therefore, the AUD/USD first resistance would be the 0.7063 YTD high, followed by the 0.7100 figure. Break above will expose the August 11 swing high of 0.7136.

- USD/JPY bulls are attempting to break higher ahead of key events.

- The bears are committing to critical resistance so far.

USD/JPY is attempting to break out of a medium-term downtrend with prospects of a move up for the week ahead as we move into key events on the US calendar. The Yen traders had been wrong-footed by the Bank of Japan's surprise policy tweak last month and the recent hold on policy has left the pair able to trend up to test the daily trendline resistance as the following technical analysis will illustrate:

USD/JPY daily chart

The bulls have been moving in since the end of last week and we are on the verge of a breakout. However, there is still plenty of work to do from the bulls as we head over to key events 9n the calendar as the following analysis on the 4-hour chart shows:

USD/JPY H4 chart

The price action is building a bullish case but the resistance is key. At this moment in time, there is a lack of commitment form the bulls at the trendline resistance and the tests are feeble. Failures open risks fo a pull back as we head over to the US calendar events on Thursday.

- EUR/GBP finds acceptance above the 20/50-day EMAs and 0.8800.

- The January 13 daily high at 0.8897 will be the bull’s next target if the EUR/GBP achieves a daily close above 0.8800.

The EUR/GBP hit a five-day new high at 0.8846, as positive Eurozone data outweighed bad UK PMIs, which reignited recessionary fears amongst Britons. Therefore, the EUR/GBP exchanges hands at 0.8823, above its opening price by more than 0.50%.

EUR/GBP Price Analysis: Technical outlook

After bottoming around 0.8721 last Thursday, the EUR/GBP achieved three straight days finishing with gains. In addition, the EUR/GBP climbed above the 50 and 20-day Exponential Moving Averages (EMAs), each at 0.8755 and 0.8792, respectively, opening the door for further upside.

Looking ahead, the EUR/GBP might hold its reins above 0.8800. Once achieved, the EUR/GBP might challenge the January 13 daily high of 0.8897, ahead of the 0.8900 mark. A breach of the latter will send the pair rallying to the September 28 swing high of 0.9066.

As an alternate scenario, the EUR/GBP first support would be the 0.8800 figure. Once broken, the 20-day EMA at 0.8792 would be tested and might allow a bearish continuation towards the 50-day EMA at 0.8755, ahead of a one-month-old upslope support trendline at 0.8740.

EUR/GBP Key Technical Levels

- USD/CHF rises but clashes with the 20-day EMA and retreats some of its gains.

- The USD/CHF failure to crack 0.9300 exacerbated a pullback towards 0.9220s.

The USD/CHF climbs slightly after hitting a daily low of 0.9192 and reclaims the 0.9200 figure in the mid-North American session. Nevertheless, the USD/CHF surrendered some of its earlier gains once it failed to stay above the 20-day Exponential Moving Average (EMA). At the time of writing, the USD/CHF is trading at 0.9228.

USD/CHF Price Analisis: Technical outlook

The daily chart shows that the USD/CHF remains neutral to downward biased. It was further cemented by the USD/CHF pair, which after reaching a daily high of 0.9297, it was unable to stay above the 20-day EMA at 0.9248. The USD/CHF retreated further but persisted in positive territory.

If the USD/CHF registers a daily close around Tuesday’s open, that will form a doji, which could exacerbate a resumption of the downtrend, posing a threat to the YTD low of 0.9091. Nevertheless, on its way south, the USD/CHF would find some hurdles, like the 0.9150 February 21 daily low, followed by the 0.9100 mark, and then the YTD low.

As an alternate scenario, the USD/CHF first resistance would be the 20-day EMA at 0.9248, followed by 0.9300. A breach of the latter will expose the 50-day EMA at 0.9356, followed by 0.9400.

USD/CHF Key Technical Levels

- USD/CAD all depends on the BoC this week and the build-up to the Fed next week.

- USD/CAD is flat on the day following stock market volatility.

USD/CAD is flat on the day after travelling between a low of 1.3346 and a high of 1.3413 so far while US stocks have been volatile making for choppy trading conditions in the forex space on Tuesday.

Stocks took a breather after a two-day rally, with earnings from major companies starting to roll in. Market participants also digested economic data on manufacturing which led to volatility while the New York Stock Exchange saw an unusual number of halts at the open.

Meanwhile, we have important events coming up in the forex commodities complex in NZ and Aussie CPI ahead of critical US economic data later in the week. The main focus is on the Bank of Canada, Wednesday, and the Federal Reserve at the start of next week.

There are a lack of catalysts outside of teeth data with the Fed officials out on the blackout week ahead of the highly anticipated Fed interest rate decision. The market is running on Fed-official-fumes following the speakers that commented on their outlooks for monetary policy in the build-up to next month's Fed meeting.

The most hawkish of comments came from St. Louis Federal Reserve's President James Bullard who said US interest rates have to rise further to ensure that inflationary pressures recede.

''We’re almost into a zone that we could call restrictive - we’re not quite there yet,” Bullard said Wednesday in an online Wall Street Journal interview. Officials want to ensure inflation will come down on a steady path to the 2% target. “We don’t want to waver on that,” he said.

“Policy has to stay on the tighter side during 2023” as the disinflationary process unfolds, Bullard added.

Bullard has pencilled in a forecast for a rate range of 5.25% to 5.5% by the end of this year.

However, there have been bearish tendencies in the US data of late for the US Dollar which has remained under pressure for the best part of the last couple of weeks. Economic reports, such as Producer Price Index and Retail Sales have shown disinflationary tendencies, reinforcing expectations that the Fed will continue to reduce its tightening pace in upcoming meetings.

However, analysts at ANZ Bank recently wrote a note, entitled, ''Fed tightening not done yet.''

''So far in early 2023, US data releases have indicated a mild easing in inflationary pressures and softer demand. This indicates the Fed’s aggressive tightening last year is starting to take effect,'' the analysts explained. ''Weakness in housing is evident (existing home sales fell 17.8% last year), manufacturing activity has faltered and Retail Sales are returning to trend.''

''This is exactly what the Fed wants as it tries to steer inflation sustainably back to target. But it is early days, and the Fed will not declare victory on inflation yet,'' the analysts reminded its readership.

''However, the Federal Open Market Committee is entering a more nuanced phase of the tightening cycle. The lagged effects of last year’s policy tightening still have further to bite, and so far, there is no widespread evidence that the labour market is weakening significantly''

''High visibility layoffs at some major tech and financial firms are grabbing the headlines, but the layoffs are global and US initial claims data are not indicating that labour demand is weakening. We think the Fed will continue to emphasise the tightness of the labour market in its deliberations and err towards further tightening. We expect a 25bp rate hike at the next meeting and guidance that rates will need to rise further.''

Meanwhile, as for the Bank of Canada, money markets see a roughly 70% chance that the Bank of Canada will raise its benchmark interest rate by 25 basis points to a 15-year high of 4.50% at a policy announcement on Wednesday, Reuters reported.

Analysts at TD Securities look for the BoC to hike by 25bp in January. ''We expect this will be the last hike this cycle, though the forward-looking component will not preclude future hikes.''

For the CAD. the analysts argue that the currency may not receive much directional bias from this meeting with markets focused on the other side of this interest rate cycle. ''CAD may be more sensitive to any dovish elements should the BOC emphasize elements from the BOS. CAD's correlation with risk is high so that may take on added importance.''

- GBP/USD reached its daily low after the release of US S&P Global PMIs.

- Business activity in the UK reignited recession fears and weakened the GBP.

- The market expects the Bank of England to hike rates by 50 bps on February 2 – RTRS Poll.

GBP/USD surrenders 1.2400 and drops towards the 1.2310 regions amid a mixed mood trading session, as US equities fluctuate between gainers/losers. Nevertheless, the American Dollar (USD) is losing traction and edging lower, capping the GBP/USD’s fall. At the time of writing, the GBP/USD is trading at 1.2320 after hitting a high of 1.2413.

GBP/USD fell as low as 1.2260s on better-than-expected US PMIs and weak UK data

Wall Street portrays a mixed picture, but it’s a matter of time before it turns positive. S&P Global reported that December’s PMIs for the United States (US) improved, with the Services PMI coming at 46.6 vs. 44.7 expected, while Manufacturing rose by 46.8 vs. estimates of 46.2. The S&P Global Composite, which measures both indices, increased by 46.6, higher than the foreseen 45 figure. Although business activity continues to show deterioration in the US economy, the downward trend moderated some.

Across the pond, UK’s business activity disappointed investors, with business activity falling at its fastest rate in two years, according to an S&P Global/CIPS Survey. “Weaker-than-expected PMI numbers in January underscore the risk of the UK slipping into recession,” S&P Global’s Chief Business Economist, Chris Williamson, said.

In the meantime, a Reuters Poll showed that 29 of 42 economists estimate the Bank of England to raise the Bank’s rate by 50 bps to 4% on February 2, while 13 estimated a 25 bps hike. In addition, the economists expect a peak rate of 4.25%.

Also read: Reuters Poll: Bank of England to lift bank rate by 50 bps to 4.00% on February 2

GBP/USD Technical Analysis

Technically, the GBP/USD daily chart suggests the pair is consolidating around 1.2400, unable to aim higher and test the 1.2500 mark. Also, in the last couple of days, successive lower lows have opened the door for further losses. Of note, the GBP/USD appears to be forming a double top. However, the GBP/USD would need to fall below the January 6 daily low of 1.1841 to confirm its validity.

GBP/USD Key support levels are the 1.2300 figure, the 20-day EMA at 1.2222 and 1.2100. On the flip side, the GBP/USD key resistance levels are 1.2400, followed by the YTD high of 1.2454 and the 1.2500 mark.

- USD/JPY back into negative territory after a spike following US data.

- US PMI S&P Global recovers in January, still below 50.

- US Dollar weakens during the American session amid risk appetite.

The USD/JPY spiked to 131.21, following the release of US economic data but then pulled back toward 130.00 as stocks turned positive on Wall Street. The improvement in risk sentiment weighed on the US dollar.

Data released on Tuesday showed the PMI S&P Global Manufacturing rose in January according to preliminary numbers from 46.2 to 46.8, above the 46.1 of market consensus. The Service index climbed from 44.7 to 46.6, surpassing expectations of 44.5. Immediately after the release, the US dollar peaked but only to retreat later.

In Wall Street, after a negative opening main indexes are flat. Risk appetite and a retreat in US yields pushed USD/JPY to the downside. The pair is testing levels under 130.00, looking at the daily low it hit on Asian hours at 129.72.

Again, the 20-day Simple Moving Average, currently at 130.90, capped the upside. The main trend is bearish although in the short term, the Dollar is correcting higher. It continues to be unable to hold above 131.00. If it manages to do so, a deeper recovery seems likely.

Technical levels

European Central Bank (ECB) policymaker Gediminas Simkus said on Tuesday that the ECB should continue with 50 basis points (bps) rate hikes amid growing wage pressures, as reported by Bloomberg.

Simkus further added that reaching the peak policy rate before summer 'may be unlikely' and noted that strong core inflation shows that their battle against inflation is not over yet.

Market reaction

EUR/USD edged slightly higher with the initial reaction to these comments and was last seen posting small daily gains at 1.0875.

An improving macro backdrop and continued policy tightening from the ECB portend Euro strength in 2023, according to economists at CIBC Capital Markets.

ECB is looking at adjusting policy in 50 bps clips

“The improved macro backdrop comes as the ECB now details that ‘rates will still have to rise significantly at a steady pace to reach levels that are sufficiently restrictive to ensure a timely return of inflation to the 2% medium-term target.’ Breaking down the language suggests that the bank is looking at adjusting policy in 50 bps clips, at least across Q1.”

“Overall, we would be wary of EUR gains proving potentially over-extended, albeit we would expect any correction to be short-lived.”

AUD/USD broke decisively above 0.7000 yesterday. Australian Consumer Price Index data for the fourth quarter could fuel the rally if figures come out sticky, economists at ING.

AUD/NZD may retest the recent 1.0950 highs soon

“Tonight’s fourth-quarter CPI data in Australia will be key, as evidence of sticky inflation may force a hawkish repricing across the AUD curve (which currently embeds 40 bps of extra Reserve Bank of Australia tightening) and add steam to the AUD/USD rally.”

“CPI figures are released also in New Zealand and we see a larger risk they could show a deceleration in price pressures compared to Australia. AUD/NZD may retest the recent 1.0950 highs soon as the NZD curve has more room for a dovish repricing.”

See:

- Australian CPI Preview: Forecasts from seven major banks, sticky inflation figures

- NZ CPI Preview: Forecasts from four major banks, past the peak, but still red-hot

The European Central Bank should not pre-commit to any specific policy move beyond February, European Central Bank (ECB) executive board member Fabio Panetta told German newspaper Handelsblatt on Tuesday, as reported by Reuters.

Panetta argued that they can bring inflation down with well-calibrated and non-mechanical rate hikes and noted that he is "anxiously optimistic" about inflation after recent good readings.

Market reaction

EUR/USD managed to rebound from daily lows after these comments and was last seen trading at 1.0855, where it was down 0.1% on a daily basis.

- Gold price tumbled 0.50% on Tuesday after the release of US PMI data.

- US S&P Global PMIs remained in contractionary territory but appeared to bottom out.

- The US Federal Reserve is expected to raise rates by 25 bps, as CME FedWatch Tool shows.

- Gold Price Analysis: On a pullback before resuming its uptrend.

Gold price struggles to continue its rally after hitting a new 9-month high at $1,942.51, retreats to the $1,930s area, as Wall Street prepares to open on a lower note. Factors like a risk-off impulse, and the greenback erasing earlier losses, weighs on the XAU/USD. Therefore, the XAU/USD exchanges hands at $1,928.39.

Risk aversion is underpinning the US Dollar

The US cash equity market is poised for a lower open. The XAU/USD main driver so far in the day has been the American Dollar (USD), which, according to the US Dollar Index (DXY), which tracks the buck’s value vs. a basket of six currencies, is bottoming around 102.000, and so far is up 0.13%, at 102.150. Contrarily, US Treasury bond yields, namely the 10-year benchmark note rate, which usually influences Gold’s price, are unchanged at 3.532%.

US S&P Global PMIs were better than expected, weighing on Gold’s price

The US economic docket featured January’s PMIs, revealed by S&P Global, with the Services PMI coming at 46.6 vs. 44.7 expected, while Manufacturing rose by 46.8 vs. estimates of 46.2. The S&P Global Composite, which measures both indices, increased by 46.6, higher than the foreseen 45 figure. Even though US business activity remains in contractionary territory, the downward trend moderated.

“The worry is that, not only has the survey indicated a downturn in economic activity at the start of the year, but the rate of input cost inflation has accelerated into the new year, linked in part to upward wage pressures, which could encourage a further aggressive tightening of Fed policy despite rising recession risks,” Chris Williamson, a chief business economist at S&P Global Market Intelligence, said in a statement.

After the release of US data, the XAU/USD continues to extend its losses towards the $1,920 region.

US Federal Reserve to raise rates by 25 bps on next weeks

Aside from this, the US Federal Reserve (Fed) would feature its first monetary policy meeting from January 31 – February 1, in which the US Central Bank is estimated to hike rates by 25 bps, which would lift the Federal Funds rate (FFR) at the 4.50% - 4.75% range. The CME FedWatch Tool, odds for a 25 bps hike are 96.6%, with eight days ahead. For the March meeting, traders expect the Fed to raise rates to the 4.75% - 5.00% range. The slowdown in interest rate increases was spurred by inflation tempering in December, after the core Consumer Price Index (CPI) edged towards 5.7%, after peaking in September of 2022 at 6.6%.

Gold Technical Analysis

From a technical perspective, the XAU/USD daily chart suggests that the yellow metal uptrend remains unchanged. The ongoing pullback toward the $1,920 area could be a respite for XAU’s bulls after the Relative Strength Index (RSI) reached overbought conditions. Once the RSI exits from the oversold area, that would be the reason to resume the uptrend. Therefore, the XAU/USD first resistance would be $1,950, followed by the $2,000 mark. As an alternate scenario, if Gold struggles, its next support would be $1,900, followed by the 20-day Exponential Moving Average (EMA) at $1,883.75.

- USD/MXN with a bullish intraday bias, bearish in the long term.

- Correction from levels above 19.00, finds support at the 18.80 zone.

- US Dollar mixt on Tuesdays gains momentum after US data.

The USD/MXN is rising on Tuesday, after a two-day correction of the rally from multi-year lows near 18.55 (January 18) to 19.11 (January 19). The decline found support around the 18.80 zone and bounced toward 18.90.

The pair is trading at daily highs at 18.88 following the release of the US S&P Global PMI report that came in above expectations boosting the US Dollar across the board amid higher Treasury bond yields. At the same time, Emerging Market currencies, like the Mexican Peso lost further strength on the back of a deterioration in market sentiment and lower commodity prices.

The Mexican Peso needs to break and hold below 18.80, in order to regain strength. The next support stands at 18.65 followed by the recent bottom near 18.55.

The daily chart shows the main trend is bearish but technical indicators are modestly biased to the upside in the short term, suggesting some consolidation ahead that could be between 18.80 and 19.00, or with a higher limit at 19.11, a horizontal level and the 20-day Simple Moving Average. A break above would strengthen the US Dollar.

USD/MXN daily chart

-638101697011234253.png)

Economists at CIBC Capital Markets see the Canadian Dollar stuck in neutral in Q1 as markets are almost fully priced for BoC and Fed action, before gaining ground over the rest of 2023 as the USD falls out of favour.

USD/CAD to reach 1.28 in 2024

“With markets almost fully priced for both the Bank of Canada and Federal Reserve over the rest of Q1, expect the Loonie to be stuck in neutral in the near term, with USD/CAD likely ending the quarter at 1.34.”

“We expect USD/CAD to end the year at 1.31.”

“With global growth likely to receive a lift as central banks outside of North America start to normalize policy rates, and higher commodity prices benefitting Canada’s export sector, look for USD/CAD to reach 1.28 in 2024.”

- S&P Global Manufacturing and Services PMIs rose modestly in early January.

- US Dollar Index holds in positive territory above 102.00.

The business activity in the US private sector continued to contract in early January, albeit at a softer pace than in December. S&P Global Manufacturing PMI edged higher to 46.8 from 46.2 and Services PMI recovered to 46.6 from 44.7. Finally, the Composite PMI came in at 46.6, compared to 45 in December. All these figures came in slightly better than the market expectations.

Commenting on the data, "the US economy has started 2023 on a disappointingly soft note, with business activity contracting sharply again in January," noted Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

"Although moderating compared to December, the rate of decline is among the steepest seen since the global financial crisis, reflecting falling activity across both manufacturing and services," Williamson added.

Regarding input price pressures, Williamson explained that the rate of input cost inflation has accelerated into the new year, linked in part to upward wage pressures.

Market reaction

With the initial reaction, the US Dollar gathered strength against its rivals and the US Dollar Index was last seen rising 0.25% on the day at 102.25.

- EUR/USD’s upside appears capped around 1.0900.

- EMU, Germany flash PMIs came on a mixed note.

- US advanced PMIs also due later in the NA session.

EUR/USD appears to have met some decent resistance in the proximity of the 1.0900 hurdle so far on Tuesday.

EUR/USD: Rally shows signs of exhaustion

EUR/USD seems to struggle to extend the January’s rally further north of the 1.0900 mark amidst vacillating risk appetite trends and the consolidative theme surrounding the greenback.

Indeed, market participants appear prudent ahead of the upcoming FOMC event and the ECB gathering, both due next week and with bets favouring a 25 bps and 50 bps rate hike, respectively.

In the domestic calendar, Consumer Confidence in Germany tracked by GfK improved to -33.9 for the month of February. Additionally, the flash prints for the Manufacturing and Services PMIs in the euro area came at 48.8 and 50.7, respectively, while the same gauges for Germany came at 47 and 50.4, respectively.

In the US, the Manufacturing PMI is expected at 46.8 and the Services PMI at 46.6 in January.

What to look for around EUR

EUR/USD comes under pressure soon after failing to break above the key 1.0900 mark on Tuesday.

Price action around the European currency should continue to closely follow dollar dynamics, as well as the impact of the energy crisis on the euro bloc and the Fed-ECB divergence.

Back to the euro area, the increasing speculation of a potential recession in the bloc emerges as an important domestic headwind facing the euro in the short-term horizon.

Key events in the euro area this week: Germany GfK Consumer Confidence, France Business Confidence, ECB Lagarde, EMU/France/Germany Advanced Manufacturing/Services PMIs (Tuesday) – Germany Ifo Business Climate (Wednesday) – Italy Business Confidence (Thursday) – France Consumer Confidence, ECB Lagarde (Friday).

Eminent issues on the back boiler: Continuation of the ECB hiking cycle amidst dwindling bets for a recession in the region and still elevated inflation. Impact of the war in Ukraine and the protracted energy crisis on the bloc’s growth prospects and inflation outlook. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is losing 0.05% at 1.0862 and the breakdown of 1.0766 (weekly low January 17) would target 1.0560 (55-day SMA) en route to 1.0481 (monthly low January 6). On the other hand, the next up barrier emerges at 1.0926 (2023 high January 23) followed by 1.0936 (weekly high April 21 2022) and finally 1.1000 (round level).

Gold price touched a nine-month high on Tuesday. The yellow metal needs to surpass the $1,970 region to firm further, strategists at TD Securities report.

Break below $1,900 to spark trend follower liquidations

“The bar is low for price action to catalyze yet another CTA buying program in Gold. However, algo trading flows are expected to remain limited with substantial purchases only likely above the $1,970 range. Still, Gold prices could struggle to firm further in the absence of the single-largest buyer of Gold over the past months.”

“On the downside, a break below the $1,900 range is required to spark trend follower liquidations.”

Australian Q4 Consumer Price Index (CPI) data could be the deciding factor for RBA's February meeting. Economists at Commerzbank believe that an upside surprise could lift the Aussie.

Rate cycle in Australia almost over?

“Consumer prices are likely to increase the expectation of a rate step next week, if they are in line with expectations, thus supporting AUD a little. If the data surprises to the upside, the AUD is likely to jump higher due to the adjustment of rate expectations.”

“it will be more interesting for AUD how the RBA positions itself for the coming months as of 1st February – i.e. whether an imminent end of the rate cycle is in view or not. If that is the case the market is likely to lower its expectations for the peak of the key rate, which would put pressure on AUD.”

See – Australian CPI Preview: Forecasts from seven major banks, sticky inflation figures

With the Fed set to undershoot market expectations for the peak fed funds rate, and attention turning to policy tightening in other advanced economies, economists at CIBC Capital Markets look for the USD to weaken in 2023.

USD to fall out of favour over 2023

“We see some modest upside in the USD from potential data surprises that might tilt market pricing for Fed rate hikes at the margin. However, we’d look past that as the upcoming ‘step down’ to 25 bps hikes has been telegraphed by the market for now.”

“The USD should continue to come under pressure in the quarters ahead as the protracted showdown over the debt ceiling leads to an increased premium on USD valuation.”

“When layered with a much better backdrop outside of North America, this year is shaping up to be a difficult one for USD bulls.”

US PMI Overview

S&P Global will release the flash version of the US Manufacturing and Services PMIs at 14:45 GMT this Tuesday. The gauge for manufacturing is expected to remain in contraction territory for the fourth straight month and come in at 46.1 for January, slightly lower than the 46.2 in the previous month. The Services PMI, meanwhile, is also anticipated to deteriorate further to 44.5 for the current month, marking the sixth successive month of contraction. Furthermore, the composite PMI is expected to show a contraction in the overall business activity and edge down to 44.7 from 45.0 previously.

How Could it Affect EUR/USD?

Ahead of the key release, a fresh leg down in the equity markets assists the safe-haven US dollar to stage a modest recovery from a nine-month low touched earlier this Tuesday. A stronger US PMI print could lend additional support to the greenback, though expectations for a less aggressive policy tightening by the Fed should cap gains.

Conversely, weaker US macro data will reaffirm market bets for a smaller 25 bps Fed rate hike in February and prompt fresh selling around the buck. Apart from this, the recent hawkish rhetoric from ECB officials, signalling additional jumbo rate hikes in the coming months, might continue to underpin the shared currency. This, in turn, suggests that the path of least resistance for the EUR/USD pair is to the upside.

Eren Sengezer, European Session Lead Analyst at FXStreet, offers a brief technical outlook for the major and writes: “Despite the latest pullback, EUR/USD continues to trade within the ascending regression channel coming from early January. Additionally, the Relative Strength Index (RSI) indicator on the four-hour chart holds above 50. Both of these technical developments suggest that the pair's current action could be considered as a technical correction.”

Eren also outlines important technical levels to trade the EUR/USD pair: “On the downside, 1.0850 (lower limit of the ascending channel, 20-period Simple Moving Average (SMA)) aligns as immediate support. If EUR/USD falls below that level and starts using it as resistance, sellers could show interest and trigger an extended slide toward 1.0830 (50-period SMA) and 1.0800 (psychological level). ”

“In order to gather bullish momentum, EUR/USD needs to rise above 1.0900 (psychological level, mid-point of the ascending channel) and stabilize there. In that scenario, additional gains toward 1.0930 (upper-limit of the ascending channel) and 1.0980 (former support, static level) could be witnessed.” Eren adds further.

Key Notes

• EUR/USD Forecast: Euro needs to stabilize above 1.0900 to reach new multi-month tops

• EUR/USD: Gains through low 1.09s to revive bull move for a push on to 1.1000/50 – Scotiabank

• EUR/USD Price Analysis: Upside bias unchanged above 1.0650

About the US Manufacturing PMI

The Manufacturing Purchasing Managers Index (PMI) released by S&P Global captures business conditions in the manufacturing sector. As the manufacturing sector dominates a large part of total GDP, the manufacturing PMI is an important indicator of business conditions and the overall economic condition in the United States. Readings above 50 imply the economy is expanding, making investors understood it as a bullish for the USD, whereas a result below 50 points for an economic contraction, and weighs negatively on the currency.

About the US ISM Services PMI

The Services Purchasing Managers Index (PMI) released by S&P Global captures business conditions in the services sector. As the services sector dominates a large part of total GDP, the services PMI is an important indicator of the overall economic condition in US. A result above 50 signals is bullish for the USD, whereas a result below 50 is seen as bearish.

- The index now adds to Monday’s uptick above the 102.00 mark.

- Risk appetite trends remain inconclusive so far on Tuesday.

- Preliminary PMIs, Richmond Fed Index next on tap.

Alternating risk appetite trends keep the price action volatile around the greenback and now motivates the USD Index (DXY) to advance further north of the 102.00 yardstick.

USD Index appears bid pre-PMIs

The index remains side-lined around the 102.00 zone against the backdrop of the equally inconclusive sentiment in the risk complex on turnaround Tuesday.

Indeed, investors’ expectations surrounding the next FOMC event on February 1 also appear unchanged and keep favouring a 25 bps interest rate hike, while speculation around a Fed’s pivot and the likelihood of a soft landing of the economy continue to run high among traders.

Later in the US calendar, all the attention will be on the preliminary prints of the Manufacturing and Services PMIs for the current month seconded by the Richmond Fed Manufacturing Index.

What to look for around USD

The dollar’s price action remains subdued in the lower end of the recent range around the 102.00 region so far this week.

The idea of a probable pivot in the Fed’s policy continues to weigh on the greenback and keeps the price action around the DXY depressed. This view, however, also comes in contrast to the hawkish message from the latest FOMC Minutes and recent comments from rate setters, all pointing to the need to advance to a more restrictive stance and stay there for longer, at the time when rates are seen climbing above the 5.0% mark.

On the latter, the tight labour market and the resilience of the economy are also seen supportive of the firm message from the Federal Reserve and the continuation of its hiking cycle.

Key events in the US this week: Flash Manufacturing/Services PMIs (Tuesday) – MBA Mortgage Applications (Wednesday) – Durable Goods Orders, Advanced Q4 GDP Growth Rate, Chicago Fed National Activity Index, Initial Jobless Claims, New Home Sales (Thursday) – PCE, Core PCE, Personal Income, Personal Spending, Pending Home Sales, Final Michigan Consumer Sentiment (Friday).

Eminent issues on the back boiler: Rising conviction of a soft landing of the US economy. Prospects for extra rate hikes by the Federal Reserve vs. speculation of a recession in the next months. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China trade conflict.

USD Index relevant levels

Now, the index gains 0.02% at 102.04 and a breakout of the weekly high at 102.89 (January 18) would pave the way for a test of 105.63 (monthly high January 6) and then 106.45 (200-day SMA). On the flip side, the next support emerges at 101.52 (2023 low January 18) seconded by 101.29 (monthly low May 30 2022) and finally 100.00 (psychological level).

Economists at ING expect the USD/CAD to enter a sustainable downside path in the second half of the year. However, the pair could test 1.30 in the coming weeks.

CAD may lag other commodity currencies such as AUD and NZD

“A BoC-Fed rate gap of -50 bps (if the Fed hikes to 5.0%) does limit the downside potential of USD/CAD. However, there is a chance that the Fed cuts rates more aggressively in the second half of the year, and that is when USD/CAD could stabilise on a more solid downward path. Until then, it is possible that CAD may lag other commodity currencies such as AUD and NZD as it can only partly benefit from China’s improved growth story and suffers from domestic and US negative growth re-rating.”

“A test of 1.3000 in the coming weeks is surely possible in USD/CAD, but would likely be due to either more idiosyncratic USD weakness or rising oil prices.”

29 of 42 economists that took part in a recently conducted Reuters poll said that they expect the Bank of England to raise the policy rate by 50 basis points (bps) to 4% on February 2. 13 economists said they were looking for a smaller, 25 bps, hike.

"Median forecasts in the poll showed the Bank would then add 25 basis points in March, giving a peak rate of 4.25%," Reuters wrote.

Market reaction

This headline doesn't seem to be providing a boost to the Pound Sterling. As of writing, GBP/USD was down 0.7% on the day, trading at around 1.2290.

- NZD/USD attracts some intraday sellers amid a modest bounce from a multi-month low.

- Recession fears take a toll on the risk sentiment and benefit the safe-haven greenback.

- Bets for smaller Fed rate hikes drag the US bond yields lower and cap gains for the USD.

- Traders eye US PMIs for some impetus ahead of NZ quarterly CPI report on Wednesday.

The NZD/USD pair continues with its struggle to find acceptance above the 0.6500 psychological mark and retreats over 50 pips from a multi-day high touched earlier this Tuesday. Spot prices return to the lower end of the daily range, around the 0.6480-0.6475 region, heading into the North American session, though any meaningful decline seems elusive.

Worries about a deeper global economic downturn keep a lid on any optimism in the markets, which is evident from a fresh leg down in the equity markets. This, in turn, assists the safe-haven US Dollar to stage a modest recovery from a nine-month low and drives some flows away from the risk-sensitive Kiwi. That said, the prospects for a less aggressive policy tightening by the Fed might cap the upside for the greenback and lend support to the NZD/USD pair.

Investors seem convinced that the US central bank will soften its hawkish stance amid signs of easing inflationary pressures. In fact, the markets have been pricing in a smaller 25 bps rate hike move at the end of the upcoming policy meeting next week. This, in turn, exerts some downward pressure on the US Treasury bond yields and might continue to weigh on the buck. Traders also seem reluctant to place aggressive bets ahead of this week's important macroeconomic data.

The quarterly consumer inflation report from New Zealand is scheduled for release during the early Asian session on Wednesday. This will be followed by the Advance Q4 GDP print and the Core PCE Price Index from the US on Thursday and Friday, respectively. The key focus, however, will remain on the highly-anticipated FOMC monetary policy decision. This will play a key role in driving the USD in the near term and help determine the near-term trajectory for the NZD/USD pair.

In the meantime, traders on Tuesday will take cues from the US economic docket, featuring the flash PMI prints and the Richmond Manufacturing Index. Apart from this, the US bond yields and the broader risk sentiment, will influence the USD price dynamics and provide some meaningful impetus to the NZD/USD pair. Nevertheless, the fundamental backdrop still seems tilted in favour of bullish traders, suggesting that any meaningful pullback might be seen as a buying opportunity.

Technical levels to watch

EUR/USD keeps its range below the 1.09 level. A move above here will revive bullish momentum, economists at Scotiabank report.

Firm support on modest dips to the low/mid-1.08s

“EUR/USD is holding a solid-looking bull trend on the daily chart and is backed by supportive trend strength oscillators across the short, medium and longer-term DMIs. This should mean limited scope for counter-trend EUR losses and firm support on modest dips to the low/mid-1.08s. It should also mean steady progress higher in spot – which has been less obvious over the past few sessions.”

“Gains through the low 1.09s will revive the bull move for a push on to 1.1000/50.”

- EUR/USD alternates gains with losses below the 1.0900 mark.

- The 2-month support line near 1.0650 holds the downside so far.

EUR/USD’s daily advance falters just ahead of the key 1.0900 barrier on turnaround Tuesday.

The continuation of the uptrend now needs to rapidly clear the 2023 high at 1.0926 (January 23) to allow for a test of the weekly top at 1.0936 (April 21 2022). A sustainable break above this level could pave the way for a challenge of the key barrier at 1.1000 the figure in the not-so-distant future

In the meantime, while above the short-term support line near 1.0650, extra gains should remain in store for the pair.

In the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0308.

EUR/USD daily chart

GBP/USD drops to 1.23. The pair could extend its fall to the 1.22 level, economists at Scotiabank report.

Fiscal policy remains a potential weakness in the GBP outlook

“Intraday weakness in the GBP below support at 1.2315 leaves the Pound exposed to more weakness – unless it can quickly stabilize and strengthen.”

“After two tests of 1.2430/35 over the past week, a sustained break under 1.2315 triggers a mini-double top on the intraday chart which would imply more GBP losses to 1.22 over the next week or so.”

“Fiscal policy – and foreign investor participation in the UK Gilts market – remains a potential weakness in the GBP outlook.”

- USD/CAD remains under some selling pressure for the fourth straight day on Tuesday.

- Bullish crude oil prices underpin the Loonie and act as a headwind amid a weaker USD.

- Traders now eye the US macro data for some impetus ahead of the BoC on Wednesday.

The USD/CAD pair edges lower for the fourth successive day on Tuesday and remains depressed through the mid-European session. The pair is currently placed around mid-1.3300s, just a few pips above a one-week low touched on Monday and seems vulnerable to slide further.

Despite a softer risk tone, the safe-haven US Dollar struggles to capitalize on its modest intraday recovery from a nine-month low and acts as a headwind for the USD/CAD pair. Growing acceptance that the Fed will soften its hawkish stance amid signs of easing inflationary pressure turns out to be a key factor that continues to weigh on the greenback.

In fact, the markets have been pricing in a greater chance of a smaller 25 bps Fed rate hike move in February. This, along with softer US Treasury bond yields, keeps the USD bulls on the defensive. Apart from this, the recent rally in crude oil prices to over a one-month top underpins the commodity-linked Loonie and exerts pressure on the USD/CAD pair.

The aforementioned fundamental backdrop favours bearish traders and supports prospects for an extension of the USD/CAD pair's recent downward trajectory. Even from a technical perspective, last week's failure to find acceptance above the 100-day SMA validates the negative outlook and suggests that the path of least resistance for spot prices is to the downside.