- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- The USD/CAD ended the week almost flat amidst a volatile’s Friday session.

- Canada’s May GDP contracted by 0.2%, on its preliminary reading, a headwind for the CAD.

- US manufacturing data showed signs of slowing down; will the Fed slow its tightening pace?

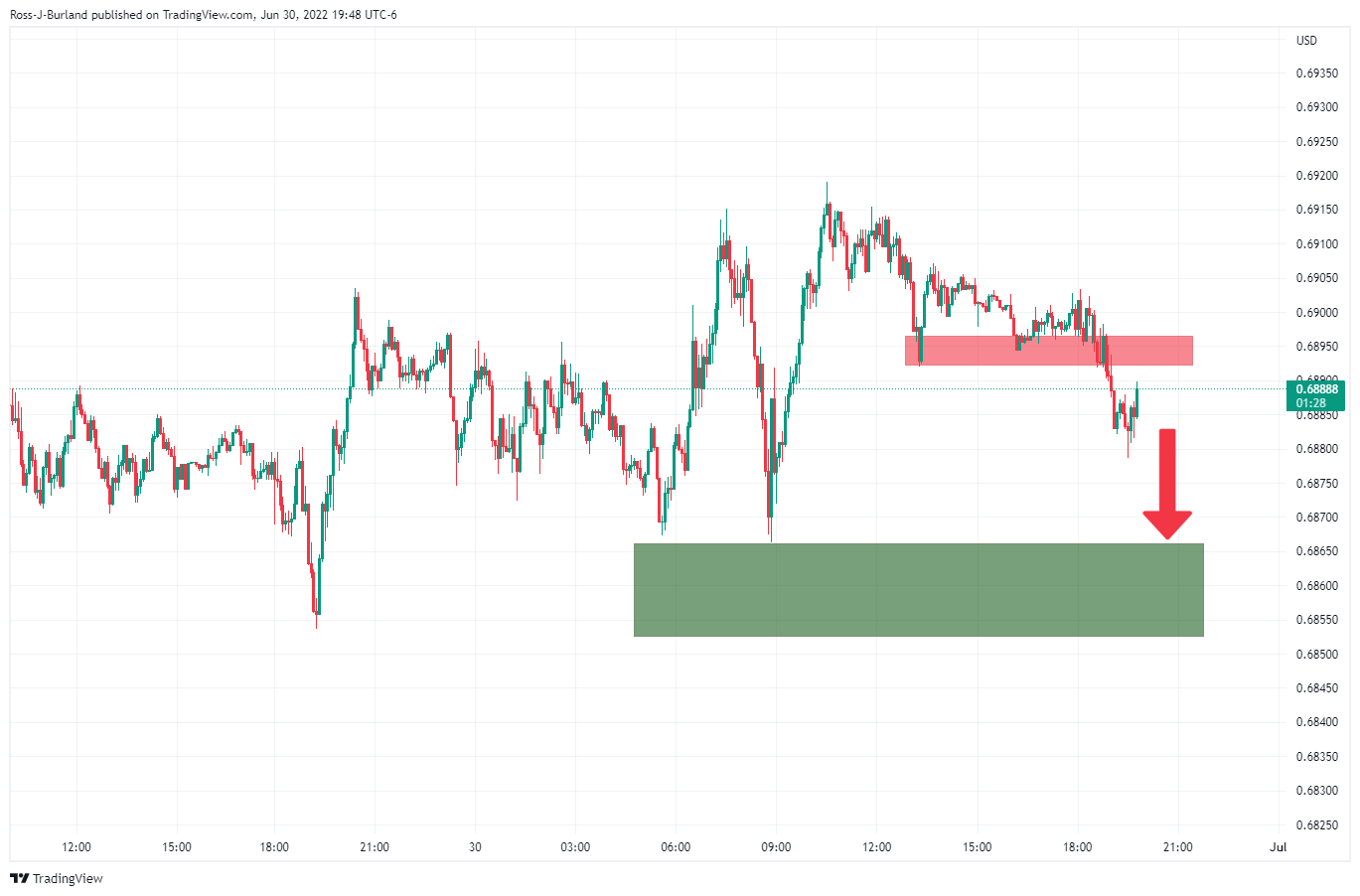

The USD/CAD pares some of Thursday’s losses after reaching a weekly high of around 1.2960s but retraced below 1.2900 as the greenback weakened ahead into a long weekend, courtesy of the US Independence day. At 1.2882, the USD/CAD records minimal gains of 0.08% and finishes the week with losses of 0.09%.

Sentiment shifts, and the USD/CAD retreats from weekly highs to familiar levels

US equities finished with solid gains after the S&P 500 slumped by 20% since its peak in 2022. US manufacturing data, as reported by the Institute for Supply Management, released June’s Manufacturing PMI at 53.0, lower than the 54.9 expected prior at 56.1. Investors’ reaction was a counter-cyclical, buying the US dollar as a safe-haven play as fears of a US and a global recession increased.

On the USD/CAD side, the pair rallied sharply, from around 1.2900s to 1.2966, amidst falling US Treasury yields, as bond traders bought US Treasuries, which sent short-term US bond yields plunging more than ten basis points, in the case of 2s, 5s, and 10s. The US 10-year benchmark note finalized around 2.889%, down twelve basis points and 70 bps from the 2022 peak near 3.5%.

Data-wise, during the week, the Canadian docket revealed a GDP contraction of 0.2% MoM on May’s preliminary reading, while April was downward revised from 0.7% to 0.3% MoM. The data could deter the Bank of Canada (BoC) from hiking rates aggressively, though, at the time of writing, Short Term Interest Rates (STIRs) markets have priced in a 92% chance of a 75 bps rate hike in the July 13 meeting.

On the US front, June’s Consumer Confidence reported by the Conference Board, downtick towards 98.7, missing expectations of 100.4, and trailed May’s 103.2. Furthermore, US inflation, as measured by the Personal Consumption Expenditure (PCE), and the Fed’s favorite gauge of inflation for May, rose by 6.3% YoY, lower than the 6.7% estimated. Meanwhile, the so-called core PCE, excluding volatile items, rose by 4.7% YoY, lower than foreseen and less than April’s 4.9%.

The week ahead, the Canadian economic calendar will feature S&P Global Manufacturing PMIs and Employment data. On the US front, the docket will reveal the ISN Non-Manufacturing PMI for June, the US Federal Reserve’s last meeting minutes, and the US Nonfarm Payrolls report for June.

USD/CAD Weekly chart

USD/CAD Key Technical Levels

- The EUR/GBP seesawed in a volatile 100-pip trading session on Friday.

- Weak data from the UK and the EU left traders undecided on which direction to take.

- The EUR/GBP daily chart depicts the pair as upward biased, but the 4-hour illustrates the cross might correct towards 0.8550 before resuming the uptrend.

The EUR/GBP advances during the day, though retraced from near two-week highs around 0.8678 on Friday, amidst an upbeat market mood that triggered support for risk-sensitive currencies in the FX space, the British pound one of them. At 0.8621, the EUR/GBP is trading in the green by just 0.19%.

A volatile session characterized EUR/GBP Friday’s price action. Weaker than expected, UK’s factory data lifted the cross-currency. Nevertheless, it began to pare its losses of late after hot Eurozone inflation, alongside languish factory output, was reported, painting a gloomy scenario for the EU.

EUR/GBP Daily chart

The EUR/GBP daily chart depicts the pair as neutral-upward biased. Traders should note how the Relative Strength Index (RSI) stayed steady between 50 and 70 since May, while the EUR/GBP rallied from 0.8250 to the YTD high above 0.8700. Therefore, the EUR/GBP might extend its rally in the near term and even challenge the YTD high above 0.8700, but a break above 0.8678 is needed. On the other hand, if EUR/GBP sellers plunge prices below 0.8550, that could pave the way to the 200-day EMA at 0.8442.

EUR/GBP 4-Hour chart

In the near term, the EUR/GBP 4-hour chart depicts the pair trading inside an ascending channel that has kept the cross-currency pair trading within a 100-pip range. On Friday, the cross reached the top of the range and reversed, piercing the R2 and R1 daily pivots, each at 0.8662 and 0.8633, before settling around the 20-EMA at 0.8622. Also, the Relative Strength Index (RSI) at 50.72 accelerates its fall towards the mid-line, and a cross below would pave the way for further downside in the EUR/GBP pair.

Therefore, the EUR/GBP’s first support would be the 50-EMA at 0.8609. Break below would expose the 100-EMA at 0.8592, followed by the June 30 swing low at 0.8551.

EUR/GBP Key Technical Levels

- AUD/USD reached a new YTD low at around 0.6776.

- US ISM Manufacturing PMI for June continued expanding but at a slower rhythm.

- Australia and China’s PMI came better than expected, but a jump in US bond yields kept the pair from further recovery.

The AUD/USD nose-dive to fresh YTD lows near 0.6776, on harmful US manufacturing data, thought as the New York session progressed has recovered some ground, and is closing to the 0.6800 figure. At 0.6821, the AUD/USD stays depressed and ready to finish the week with substantial losses of 2%.

A mixed market mood and a pullback in the US Dollar Index capped AUD/USD losses

Sentiment has improved as Friday’s session begins to wane. US equities pare earlier losses except for the heavy-tech Nasdaq, falling 0.19%, after slowing on a weaker than expected US ISM manufacturing data, which expanded though reached a two-year low, as new orders shrank. That sounded investors’ alarms, who also flew towards haven assets and bought US Treasuries, as depicted bu US Treasury yields plunging, with the 2-year at a time dropped 25 bps, as traders priced in a “less” aggressive than expected US Federal Reserve.

In the meantime, Timothy R. Fiore, Chair of the Institute for Supply Management, commented on the report that the manufacturing sector is being “powered” by demand while has been “held back by supply chain constraints.” Furthermore, the employment index, despite contracting, shows progress, according to the survey. Prices eased for the third month in a row while new orders fell.

During the Asian session, AUD/USD traders took cues from Australia S&P Global Manufacturing PMI, which came at 56.2, higher than foreseen, capping the AUD/USD fall. Late in the session, China’s Caixin Manufacturing PMI rose to 51.7 for June versus 50.1 expected and 48.1 prior.

AUD/USD Key Technical Levels

- The USD/CHF to finish the week with decent gains of 0.39%.

- Risk-aversion dominates Friday’s session, as throughout the whole week.

- The USD/CHF double top in the daily chart is still in play, but failure at 0.9544, paves the way for further gains as buyers eye 0.9700.

- In the near term, the major is upward biased, eyeing the 100-DMA.

The USD/CHF accelerates and reclaims the 0.9600 figure after harmful US economic data, showing that the economy, although expanding, is doing it at a slower pace than estimated amidst a US Federal Reserve tightening cycle. At the time of writing, the USD/CHF is trading at 0.9624.

US equities are falling, preparing to finish the week with substantial losses. Meanwhile, US Treasury yields have recovered some ground, while the greenback remains in the driver’s seat, as shown by the US Dollar index, up 0.58%, at 105.340.

USD/CHF Daily chart

The USD/CHF regained some composture and is trading near the week highs around 0.9641. USD/CHF traders should note that sellers failed to break below the 100-day moving average (DMA) at 0.9518, exposing the pair to additional buying pressure. Also, the Relative Strenght Index (RSI) at 46 aimed upward and broke above the RSI’s 7-day moving average, meaning that buying pressure is mounting.

Therefore, the USD/CHF first resistance would be 0.9641. Break above would expose the 0.9700 mark, followed by the 50-DMA at 0.9732.

USD/CHF 1-Hour chart

In the 1-hour chart, the USD/CHF found its floor around 0.9500 on June 29, and since then, it has not looked back, achieving successive series of higher lows and higher highs, paving the way for further gains. It is worth noting that the major on its way north broke above the simple moving averages (SMAs), further cementing the case of recovery to the upside.

Hence, the USD/CHF first resistance will be the R2 daily pivot at 0.9640. A breach of the latter would expose the June 23 high at 0.9678, followed by the 0.9700 figure.

USD/CHF Key Technical Levels

Analysts at MUFG Bank, point out that the South Korean won will likely remain affected by the ongoing concerns on global economic growth and the tightening from the Federal Reserve. They forecast USD/KRW at 1250.00 by the end of the second quarter, and at 1230.00 by the fourth quarter.

Key Quotes:

“KRW depreciated this June on resuming capital outflows amid global growth and recession worries, with foreign investors sold about a net USD4.2 bn of Korea’s local equities in the month after a net buying of USD170 mn in May. Notably, the won even breached the 1,300-mark for the first time in 13 years on June 23. As an export-driven economy, a negative exports growth in its early trade data also dragged on the KRW.”

“To counter growing inflationary pressure, the South Korean government on June 19 announced a package of emergency measures, including expanding tax cuts on fuel consumption to a legal cap of 37% from the current 30%, starting July 1 until the end of this year, and doubling tax deduction rates on credit card use for public transit services to 80%. These new measures could at least offer some support to domestic consumers and businesses amid the uncertain economic environment, in turn supporting the economy and the KRW.”

“Risk appetite is likely to remain highly volatile in the near term as uncertaiinties over external factors including global stagflation and the Fed’s policy trajectory could continue to drive KRW’s movement.”

Analysts at MUFG Bank, point out that higher crude oil imports could lead to a larger trade deficit and weigh on the Indian rupee. They forecast USD/INR at 79.500 by the end of the third quarter and at 80.000 by the end of 2022.

Key Quotes:

“The Indian rupee depreciated for the sixth consecutive month to new record lows against the USD in June. A confluence of factors such as renewed US dollar strength, mounting fears of an “anti-goldilocks” scenario and wider trade deficits pressured the rupee lower.”

“With risk sentiments to remain weak, we see risks of further outflows from the equity market which would then add strains on the rupee. Prospects of further rate hikes by the RBI are unlikely to help stem rupee losses as real yields remain entrenched in negative territory due to high inflation for at least the next three quarters.

“Other factors that are likely to keep the rupee fundamentally weak in the coming months is the widening of trade and current account deficits as import costs of oil and other commodities become more expensive.”

“The latest available data from the PPAC show an increase in the average price of Indian basket crude oil to USD116.02/bbl in June versus USD109.51/bbl in May in part due to the increase in premiums charged by Saudi Arabia. India’s current account deficit narrowed to 1.3% of GDP in Q1 from Q4’s 2.6% of GDP, but it is likely to widen to levels above 2% of GDP again thereafter due to larger trade deficits.”

According to analysts from Rabobank, if the Bank of England (BoE) do not keep step with the hawkish guidance of the Federal Reserve (Fed) there is a risk that the pound could weaken further. They see the risk of dips in the GBP/USD pair to 1.18 on a three-month view.

Key Quotes:

“In recent sessions, the market has started to switch its focus to the risks of a deteriorating growth outlook in the US. Various economic indicators suggest that the economy may already have slowed. The UK slowdown is more advanced, with the cost of living crisis having been evident for months. Arguably the challenges facing policymakers in the UK are among the most complex in the developed world. UK CPI inflation has not yet peaked, and labour market strife indicates that higher inflation expectations may be already entrenched. However, UK consumer confidence has plunged, and, more recently, measures of business sentiment have also started to dive.”

“If expectations regarding BoE policy moves do not keep step with the hawkish guidance of the Federal Reserve, it can be argued there is a risk that GBP could weaken further. Yet, GBP is also proving sensitive to fears regarding growth. We see risk of dips to GBP/USD 1.18 on a 3 month view. We expect EUR/GBP to end the year at 0.88.

“The BoE was out of the traps much earlier than either the Fed or the ECB in terms of policy tightening. However, this has failed to give the pound much of a lift, with GBP one of the poorer performing G10 currencies in the year to date. In our view, the inability of GBP to benefit substantially from the BoE’s early rate hiking cycle is due to the market’s focus on the poor growth outlook for the UK.”

Data released on Friday showed the ISM Manufacturing PMI dropped more than expected in June to 53, the lowest level in two years. According to analysts at Wells Fargo details of the report demonstrate slower activity in the manufacturing sector, but also that supply problems continue to slowly ease.

Key Quotes:

“The ISM manufacturing index slid 3.1 points to 53.0 in June. Notably, this was still above the 50-threshold signaling expansion, but marked the lowest reading in nearly two years and is consistent with a slower pace of activity. There were multiple signs of supply constraints easing, but weakness on the demand side pulled the overall index lower as new orders tumbled.”

“New orders tend to lead growth in industrial production (IP)—ISM new orders led growth in IP heading into the 2001 and the 2007 recessions. In short, this contraction-territory print for new orders is not good news for activity in the sector and could foreshadow coming weakness in actual output. One potential offset today, however, is the fact that manufacturers still have a record amount of backlog to move through, which may help support manufacturing activity even amid a pullback in new demand.”

“The June ISM piles onto weaker consumer data received this week. Investment spending is starting to weaken, which only adds to the evidence that the U.S. economy is rapidly slowing.”

- The GBP/USD prepares to finish the week with losses close to 1.80%.

- Worst than estimated, US manufacturing figures propelled the US dollar higher, a headwind for the GBP/USD.

- Investors start to price in a less aggressive Fed, as illustrated by US Treasury yields plunging more than ten bps.

The British pound trips below the 1.2000 mark, reaching a two-week low near 1.1975, after a US manufacturing report showed that, albeit expanding, the economy keeps hitting the brakes amidst growing concerns about a stagflation scenario. However, GBP/USD buyers reclaimed the figure, and at the time of writing, the GBP/USD is trading at 1.2055, down 0.98%.

Negative sentiment and US data showing that the economy is slowing bolstered the US dollar

Risk-off impulse witnessed by global equities sliding, increased appetite for safe-haven assets. The Institute for Supply Manufacturing reported that June’s Manufacturing index expanded to 53.0, lower than the 56.1 reported in May. Albeit showing that the economy stats in expansionary territory for the 25th month in a row, it’s slowing at the time that the Federal Reserve is front-loading aggressive rate hikes to the Federal funds rate (FFR).

Timothy R. Fiore, Chair of the Institute for Supply Management, commented on the report that the manufacturing sector is being “powered” by demand while has been “held back by supply chain constraints.” Furthermore, the employment index, despite contracting, shows progress, according to the survey. Prices eased for the third month in a row while new orders fell.

Meanwhile, an absent UK economic docket left GBP/USD traders adrift to US market data. The major reacted to the downside on the release, to fresh two-week lows, but of late, recovered some ground and has bounced close to 80 pips since.

In the bond market, US Treasury yields are plummeting, led by 2s, 5s, and 10s, tumbling more than ten basis points, as traders begin to price in a less aggressive US Federal Reserve. This means that financial analysts’ focus shifted towards growth amidst a time of aggressive rate hikes by worldwide central banks, which are fighting inflation levels at 40-year highs. Nevertheless, the above-mentioned shows that central banks are behind the curve and, if their scenario looks cloudy, are trying to tackle inflation without getting the economy into a recession.

GBP/USD Key Technical Levels

- Emerging market currencies extend weekly losses on Friday.

- US dollar firm on risk aversion, DXY up 0.65%.

- USD/MXN testing critical resistance that contains the 100-week SMA.

The US dollar is rising against emerging market currencies on Friday, extending weekly gains boosted by global concerns about the growth outlook and as central banks raise interest rates. The Mexican peso is among the worst performers.

The USD/MXN jumped on Friday to 20.46, reaching the highest level in two weeks. It then pulled back to the 20.30 level. High volatility is likely to remain elevated as panic continues to drive price action.

After a brief pause, USD/MXN resumed the upside on Friday, adding to weekly gains. It started to move higher from 20.05 (20-day SMA). The rally found resistance at the 20.45 strong barrier that contains the 100-week SMA. A consolidation above should point to more gains. The next strong resistance is located at 20.70.

Fear almost everywhere

In Wall Street, the main indexes are in red but off lows. Bond yields are sharply lower, reflecting risk aversion and softer expectations about monetary tightening. Economic data from the US showed a larger than expected decline in ISM Manufacturing in June that fueled recession fears.

Despite the slowdown in activity, high inflation pressures the Fed and other central banks to tighten aggressively monetary policy. Higher rates are usually negative for emerging markets.

USD/MXN weekly chart

-637922868447044425.png)

- Gold prices trim daily losses as the dollar soars on risk aversion.

- US yields collapse amid fears of a recession.

- Silver also rebounds, down “just” 2.60%.

Metals rebounded during the American session, amid a collapse in US yields. The rally in Treasuries boosted gold that dragged silver to the upside. XAU/USD is hovering around $1,800/oz, far from the daily low.

Yields tumble helping gold that helps silver

US yields spiked to the downside. The US 10-year dropped to as low as 2.79%, the lowest since late May (earlier on Friday, it traded above 3.00%), while the 30-year tumbled to 3.02%.

Recession fears are softening Fed’s tightening expectations. The bond market on Friday is showing more concerns than the equity market. In Wall Street, the Dow Jones is falling by 0.56% and the Nasdaq by 0.49%.

The sharp slide in yields pushed gold back above $1,800, alleviating the bearish pressure. XAU/USD bottomed at $1,784, the lowest since late January. It is still down for the day and about to post the lowest weekly close in months. The area around the 2022 low at $1,780 is a critical support.

Silver also trimmed losses dragged to the upside by gold. XAG/USD bottomed at $19.38, level not seen since July 2020 and it is trading at $19.75, down 2.60%. Price is under the 200-week Simple Moving average for the first time since May 2020.

Technical levels

- EUR/USD collapsed more than 100 pips after the US ISM missed the street’s forecasts but remained at expansionary territory at 53.0

- The greenback got bolstered by a counter-cyclical move, meaning that bad US data related to growth could lift the US dollar.

- EU’s inflation rose above 8.5% YoY, in line with France, Spain, and Germany’s figures.

The EUR/USD plunges as the second half of 2022 begins, breaking on its way south below the 1.0400 mark, reaching a fresh two-week high amid increasing concerns shifting towards economic growth, which now appears to be dented by an aggressive tightening of global central banks. At the time of writing, the EUR/USD is trading at 1.0396.

US ISM Manufacturing missed expectations, but the greenback rose

Sentiment remains dismal, with global equities falling. Meanwhile, the US ISM Manufacturing PMI fell below expectations to a two-year low as new orders contracted. The US Dollar, struck by a counter-cyclical move, rose on the report and hit a two-week high around 105.635 but retraced some towards 105.490. That was a headwind for the EUR/USD extending its losses, despite a hotter-than-expected EU inflation report.

Timothy Fiore, the ISM Manufacturing Business Survey Committee chair, said that manufacturing growth was “held back by supply chain constraints.” Fiore added, “Prices expansion slightly eased for a third straight month in June, but instability in global energy markets continues. Sentiment remained optimistic regarding demand, with three positive growth comments for every cautious comment. Panelists continue to note supply chain and pricing issues as their biggest concerns.”

Earlier during the European session, the Euro area reported June’s inflation, which rose 8.6% YoY, beating estimations, while the core readings expanded by 3.7% YoY, lower than foreseen. The previous report shows the high inflationary pressures reported by France, Span, and Germany, though the downtick in core figures offers a ray of hope that inflation may be close to its peak.

In the meantime, US Treasury yields are slumping sharply as investors’ focus shifted toward growth. Now that central banks are trying to tame inflation, financial analyst chatter begins to assess if the US Federal Reserve would achieve a soft landing, meaning avoiding a recession. Per the bond market reaction, sending 2s, 5s, and 10-year yields tumbling more than ten basis points illustrates that investors expect a less aggressive Fed, with money market futures expectations waiting for the first rate cut by the end of Q3 2023.

EUR/USD Key Technical Levels

- ISM Manufacturing PMI fell at a stronger pace than expected in June.

- US Dollar Index continues to push higher after the data.

The business activity in the US manufacturing sector expanded at a much softer pace in June than it did in May with the ISM Manufacturing PMI dropping to 53 from 56.1. This print came in weaker than the market expectation of 54.9.

Further details of the publication showed that Employment Index declined to 47.3 from 49.6 and New Orders Index fell to 49.2 from 55.1. Finally, Prices Paid Index dropped to 78.5 from 82.2, compared to analysts' estimate of 81.

Commenting on the data, "the US manufacturing sector continues to be powered — though less so in June — by demand while held back by supply chain constraints," noted Timothy R. Fiore, Chair of the ISM Manufacturing Business Survey Committee.

"Despite the Employment Index contracting in May and June, companies improved their progress on addressing moderate-term labor shortages at all tiers of the supply chain, according to Business Survey Committee respondents' comments," Fiore added. "Panelists reported lower rates of quits compared to May. Prices expansion slightly eased for a third straight month in June, but instability in global energy markets continues."

Market reaction

Wall Street's main indexes erased daily gains after the disappointing data and the dollar continued to gather strength as a safe haven. As of writing, the US Dollar Index was up 0.85% on the day at 105.62.

AUD/USD slipped around 9% in the second quarter. The pair approaches the July Reserve Bank of Australia (RBA) meeting with mostly headwinds. Therefore, even in the event of a hawkish surprise, economists at ING expect very limited benefits for the aussie in the near term.

Major headwinds for AUD to persist

“A significantly weakened link between domestic monetary policy dynamics and AUD/USD suggests that a rebound towards the 0.70 mark is unlikely to materialise soon even in the event of a hawkish surprise by the RBA (markets are not fully pricing in a 50 bps hike).”

“A more aggressive RBA tightening can suggest a wider room for AUD/USD recovery towards the end of this year and the start of next year (assuming that’s when market sentiment begins to recover), but a number of other factors – especially related to China’s demand and the USD outlook – will continue to be playing a big role too. All this makes any consideration about the AUD outlook purely based on rates dynamics still reductive.”

“Our baseline scenario for now is a gradual return to above-0.70 levels in AUD/USD for the remainder of the year, with most gains likely concentrated in 4Q, when the USD could start giving up some gains.”

- S&P Global Manufacturing PMI for US declined to 52.7 in June.

- S&P 500 posts modest daily gains after the data.

The S&P Global Manufacturing PMI for the US dropped to its lowest level since July 2020 at 52.7 in June from 57 in May. This print came in slightly better than the market expectation and the flash estimate of 52.4.

Commenting on the data, "the PMI survey has fallen in June to a level indicative of the manufacturing sector acting as a drag on GDP, with that drag set to intensify as we move through the summer," noted Chris Williamson, Chief Business Economist at S&P Global Market Intelligence. "Forward-looking indicators such as business expectations, new order inflows, backlogs of work and purchasing of inputs have all deteriorated markedly to suggest an increased risk of an industrial downturn."

Market reaction

The market mood remains upbeat after this report with the S&P 500 Index rising more than 0.5% on a daily basis.

- USD/TRY adds to Thursday’s advance near 17.00.

- Türkiye Manufacturing PMI eased to 48.10 in June.

- Investors’ attention shifts to Monday’s CPI release.

The Turkish lira loses further ground and pushes USD/TRY to new multi-day highs near 16.75 on Friday.

USD/TRY remains supported around 16.00

USD/TRY advances for the second straight session at the end of the week and slowly approaches the key barrier at the 17.00 yardstick.

The pair thus continues to reclaim ground lost following the sharp drop recorded on Monday, all in response to Friday’s measure by the banking watchdog (BDDK) to shore up the domestic currency.

It is worth recalling that the BDDK banned commercial loans in Turkish lira for companies with a strong FX holdings. Companies could therefore access loans in liras by converting FX currency into the government’s currency-protected time deposits or by acquiring securities.

Moving forward, all the attention will be on Monday’s release of the June’s inflation figures tracked by the CPI (73.50% YoY prev.).

Earlier in Türkiye, the Manufacturing PMI edged lower to 48.10 in June (from 49.20).

What to look for around TRY

USD/TRY keeps digesting the recent sharp decline and subsequent rebound following Friday’s announcement by the Turkish banking watchdog.

So far, price action in the Turkish currency is expected to gyrate around the performance of energy prices, the broad risk appetite trends, the Fed’s rate path and the developments from the war in Ukraine, although the effects of this new measure aimed at supporting the de-dolarization of the economy will also have its say.

Extra risks facing TRY also come from the domestic backyard, as inflation gives no signs of abating, real interest rates remain entrenched in negative figures and the political pressure to keep the CBRT biased towards low interest rates remain omnipresent.

Key events in Türkiye this week: Trade Balance (Thursday) – Manufacturing PMI (Friday).

Eminent issues on the back boiler: FX intervention by the CBRT. Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Upcoming Presidential/Parliamentary elections.

USD/TRY key levels

So far, the pair is gaining 0.41% at 16.7509 and faces the immediate target at 17.3759 (2022 high June 23) seconded by 18.2582 (all-time high December 20) and then 19.00 (round level). On the other hand, a breach of 16.0365 (monthly low June 27) would pave the way for a test of 15.6684 (low May 23) and finally 15.2702 (100-day SMA).

As we enter the second half of the year, some analysts have updated their US dollar forecasts. Here you can find the expectations of seven major banks regarding the greenback’s outlook for the coming months.

Wells Fargo

“Our short to medium term view on the US dollar is unchanged, and we continue to forecast a stronger greenback against most foreign currencies through early 2023. With the US economy now likely to fall into recession and the Fed to start cutting policy rates, we now believe the dollar will peak in mid-2023 and start to gradually weaken in the second half of next year.”

Credit Suisse

“The core source of USD strength has been a hawkish Fed in the face of upside US inflation surprises and a still-resilient real economy, despite soggy financial markets. Still, some reasons are finally emerging for a pause in the USD strength trend. US exporters are noting a material negative impact from USD strength. Also, US yield curve inversion starting in 2023 points to genuine fears of a US recession taking hold in that year. Despite these US-specific risks, we still see ex-US problems that should keep the USD on the front foot. In the case of commodity currencies, a world facing a 2023 growth shock is not one that boosts their case, whether DM or EM. Meanwhile, JPY and GBP remain hindered by defensive central banks, while the EUR is in need of ECB alchemy to convince markets it can resist fragmentation pressures. And it’s still possible that the market is underpricing the likely end-point for the US terminal rate.”

TDS

“We continue to expect a resilient USD through the early parts of the summer. That said, the following months and quarters present increasing downside USD risks, especially as we see correlations and themes changing once again. Excessive Fed tightening could start to turn on the USD, especially as US equities and growth continue to come under pressure.”

Commerzbank

“We expect the USA to slide into recession next year. This risk is already visibly increasing. We, therefore, assume that an initially aggressive Fed will no longer have a sustained USD-positive effect. Admittedly, a US recession would not be detrimental to the USD if the Fed nevertheless maintained its high-interest rate level in consideration of inflation risks. However, we no longer expect this to happen. On the contrary. We expect a significant Fed rate cut cycle (to 2.5%) in 2023. Assuming that this view gradually spreads in the market, the looming US recession will thus increasingly become a burdening factor for the US currency.”

HSBC

“Our USD framework has rested on two forces coming together causing it to strengthen, namely a hawkish Fed and slower global growth. These have underpinned and will continue to support our strong USD view for the months ahead.”

MUFG

“While spreads have worked against the dollar, the sharp decline in global equity markets has provided support. We remain of the view that current market conditions are supportive of the dollar but that later in the year the US dollar is likely to weaken on a more sustained basis.”

CIBC

“We ultimately see slowing growth and a turn in inflation as convincing the Fed to back away from what its most hawkish members are now advocating, paving the way towards a softer greenback in 2023. But that's not going to be apparent in the next few months, leaving the near term risks still tilted towards the USD retaining or even building further on its recent gains.”

US ISM Manufacturing PMI overview

The Institute of Supply Management (ISM) will release its latest manufacturing business survey result, also known as the ISM Manufacturing PMI at 14:00 GMT this Friday. The index is anticipated to decline from 56.1 in the previous month to 54.9 in June. The gauge will provide a fresh update on the manufacturing sector activity and the health of the economy amid growing worries about a possible recession.

According to Yohay Elam, Senior Analyst FXStreet: “The more important data point is Prices Paid, which is a snapshot of purchasing managers' inflation expectations. The economic calendar is pointing to a slide from 82.2 to 80.5 points. However, with rising prices being on everybody's minds – television sets and gas stations serving as billboards – there is room for an upside swing rather than a downside one.”

How could it affect EUR/USD?

Ahead of the key release, the US dollar jumped back closer to a 20-year high touched in June and dragged the EUR/USD pair back below the 1.0400 round-figure mark. Stronger-than-expected PMI print would be enough to provide an additional boost to the buck.

Conversely, any disappointment is unlikely to derail the Fed's policy tightening path or impress the USD bears amid concerns about the global economic slowdown. This, in turn, suggests that the path of least resistance for the EUR/USD pair is to the downside.

Eren Sengezer, Editor at FXStreet, offered a brief technical outlook and outlined important technical levels to trade the major: “the Relative Strength Index (RSI) indicator on the four-hour chart stays below, confirming the view that sellers look to retain control. 1.0470 (Fibonacci 23.6% retracement of the latest downtrend) aligns as initial resistance. As long as this level stays intact, buyers are likely to remain uninterested.”

“Above 1.0470, 1.0500 (psychological level, 100-period SMA) and 1.0520 (Fibonacci 38.2% retracement) could be seen as next technical hurdles,” Eren added further.

Key Notes

• ISM Manufacturing PMI Preview: High inflation component steal the show, boost dollar

• EUR/USD Forecast: Euro remains vulnerable after mixed eurozone inflation data

• EUR/USD Price Analysis: Further decline remains on the cards

About the US ISM manufacturing PMI

The Institute for Supply Management (ISM) Manufacturing Index shows business conditions in the US manufacturing sector. It is a significant indicator of the overall economic condition in the US. A result above 50 is seen as positive (or bullish) for the USD, whereas a result below 50 is seen as negative (or bearish).

- EUR/USD resumes the downside and flirts with a breach of 1.0400.

- The June low at 1.0358 should offer decent contention initially.

EUR/USD maintains the bearish bias unchanged and keeps navigating the area of 2-week lows on Friday.

The inability to surpass the 4-month line near 1.0640 should keep the downside pressure well in place around the pair for the time being. Against that, there is a minor support at the weekly low at 1.0382 (June 30) ahead of the June low at 1.0358 (June 15). A deeper pullback should put a visit to the 2022 low at 1.0348 (May 13) back on the radar.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.1106.

EUR/USD daily chart

- DXY leaves behind Thursday’s pullback and regains 105.00.

- Further up aligns the 2022 top near 105.80 (June 15).

DXY resumes the upside and reclaims the area beyond 105.00 the figure at the end of the week, managing well to keep the trade in the 2-week highs zone.

Further upside in the dollar is forecast to motivate the index to attempt another visit to the so far yearly highs near 105.80 recorded in the wake of the FOMC event in June. If cleared, then a test of the December 2002 at 107.31 could start emerging on the horizon.

As long as the 4-month line near 102.40 holds the downside, the near-term outlook for the index should remain constructive.

Looking at the longer run, the outlook for the dollar is seen bullish while above the 200-day SMA at 98.13.

DXY daily chart

- EUR/JPY drops further and breaches 141.00 to multi-session lows.

- Next on the downside comes the June low at 137.86 (June 15).

EUR/JPY comes under further selling pressure and prints new 2-week lows in the sub-141.00 region on Friday.

Despite the ongoing correction, the bullish bias in the cross remains well in place as long as the support line around 138.70 holds the downside. This area of contention is currently reinforced by the 55-day SMA.

The current bearish move, however, carries the potential to revisit the June low at 137.86 recorded on June 15, where it is expected to hold the downside.

EUR/JPY daily chart

- A combination of factors dragged Gold below the $1,800, back closer to the YTD low on Friday.

- Aggressive Fed rate hike bets, broad-based USD strength exerted heavy downward pressure.

- Recession fears did little to impress bulls or lend any support to the safe-haven commodity.

The prospects for a more aggressive policy tightening by major central banks to curb soaring inflation continued taking its toll on the non-yielding gold. Apart from this, the underlying bullish tone around the US dollar was seen as another factor that weighed heavily on the dollar-denominated commodity. Spot prices broke through the $1,800 psychological mark and tumbled back closer to the YTD low during the early North American session. Meanwhile, growing worries about a possible global recession did little to impress bullish traders or lend any support to the safe-haven XAUUSD. This, in turn, suggest that the path of least resistance for the precious metal is to the downside.

Gold Price: Key levels to watch

The Technical Confluence Detector shows that Gold Price could find decent support near the YTD low, around the $1,780 region. The said area coincides with Pivot Point one month S1 and is closely followed by Pivot Point one day S3. A convincing break below the latter would be seen as a fresh trigger for bearish traders and pave the way for an extension of the ongoing downward trajectory.

On the flip side, the $1,790 region - the convergence of Pivot Point one day S2 and Bollinger Band one-hour Lower and SMA - now seems to act as immediate resistance. Sustained strength beyond might trigger a short-covering bounce and lift Gold Price back towards the $1,798-$1,800 area. The said hurdle comprises Pivot Point one week S2, Pivot Point one day S1 and 5-period SMA 4-hour.

About Technical Confluences Detector

The TCD (Technical Confluences Detector) is a tool to locate and point out those price levels where there is a congestion of indicators, moving averages, Fibonacci levels, Pivot Points, etc. If you are a short-term trader, you will find entry points for counter-trend strategies and hunt a few points at a time. If you are a medium-to-long-term trader, this tool will allow you to know in advance the price levels where a medium-to-long-term trend may stop and rest, where to unwind positions, or where to increase your position size.

- GBP/USD witnessed aggressive selling on Friday and dived to over a two-week low.

- Technical selling below the 1.2100 mark aggravated the intraday bearish pressure.

- Descending trend-channel breakdown supports prospects for a further near-term fall.

The GBP/USD pair added to its heavy intraday losses and tumbled to over a two-week low, around the 1.2030 region heading into the North American session.

The prospects for more aggressive Fed rate hikes, along with growing recession fears, boosted demand for the safe-haven US dollar and prompted fresh selling around the GBP/USD pair on Friday. This marked the third day of a sharp fall in the previous four and took along some short-term trading stops placed near the 1.2100 mark.

The subsequent decline below a two-week-old descending trend-channel support confirmed a fresh bearish breakdown and supports prospects for a further near-term depreciating move. The negative outlook is reinforced by the fact that bearish technical indicators on the daily chart are still away from being in the oversold territory.

That said, RSI (14) on the 4-hour chart is already flashing overstretched conditions and warrants some caution for aggressive bearish traders. Nevertheless, the GBP/USD pair still seems poised to prolong the downward trajectory and challenge the 1.2000 psychological mark before eventually dropping to the YTD low, around the 1.1935 zone.

On the flip side, the aforementioned ascending channel support breakpoint, around the 1.2085 region, now seems to act as an immediate resistance ahead of the 1.2100 mark. Any further move up could be seen as a selling opportunity near the 1.2140-1.2150 region. This, in turn, should cap the GBP/USD pair near the 1.2180-1.2185 supply zone.

GBP/USD 4-hour chart

-637922746834317044.png)

Key levels to watch

- USD/JPY witnessed selling for the second successive day and dropped closer to the weekly low.

- The overnight break through an ascending trend-line and 200-hour SMA favours bearish traders.

- Mixed technical indicators warrant some caution before confirming a near-term top for the pair.

The USD/JPY pair extended its retracement slide from the 137.00 mark, or a fresh 24-year high touched on Wednesday and witnessed heavy selling for the second successive day on Friday. The corrective slide dragged spot prices back closer to the weekly low, though bulls showed some resilience below the 135.00 psychological mark.

Given the overnight breakdown through a two-week-old ascending trend-line, subsequent weakness below the 200-hour SMA was seen as a fresh trigger for bearish traders. The latter, currently around the 135.70 region, capped the USD/JPY pair's intraday recovery move and should now act as a key pivotal point for short-term traders.

Technical indicators, meanwhile, are holding deep in the bearish territory on hourly charts, though are still far from confirming a negative bias on the daily chart. This makes it prudent to wait for strong follow-through selling before confirming that the USD/JPY pair has topped out and positioning for any further depreciating move.

From current levels, any further decline below the 135.00 mark is likely to find decent support near the mid-134.00s, which if broken would trigger a fresh wave of technical selling. The USD/JPY pair might then weaken further below the 134.00 round figure and accelerate the fall towards testing the next relevant hurdle near the 133.60 area.

On the flip side, momentum beyond the 135.70 area (200-hour SMA) now seems to confront some resistance near the 136.00 round-figure mark. Any further recovery is more likely to attract fresh sellers and remain capped near the aforementioned ascending trend-line support breakpoint, now turned resistance, near the 136.35-136.40 region.

USD/JPY 1-hour chart

-637922727432240174.png)

Key levels to watch

Economist at UOB Group Lee Sue Ann suggests the RBA would continue its hiking cycle at the July 4 meeting.

Key Takeaways

“The RBA has now embarked on a more aggressive front-loading hiking cycle. We continue to expect a series of rate hikes over the coming months.”

“We now see the RBA hiking by another 90bps for the remainder of 2022 to bring the OCR to 1.75% by year-end (compared to 1.25% previously), before continuing to rise more gradually over 2023.”

European Central Bank (ECB) executive board member Fabio Panetta said on Friday that the ECB's policy normalization should remain gradual, as reported by Reuters.

Additional takeaways

"Surge in prices does not reflect excess demand in the euro area."

"Acting against fragmentation is necessary for us to fulfil that mandate."

"Inflation expectations stand at around 2% and wage increases remain moderate."

"Vulnerable countries, fragmentation would lead to capital outflows and an increase in yields, resulting in financing conditions that would be too tight."

"Least vulnerable countries would experience capital inflows that would compress yields."

"Action to prevent fragmentation is therefore not at odds with the normalisation."

"Beyond ending negative rates, further adjustments to our monetary policy stance will depend on the evolution of the outlook."

Market reaction

These comments failed to help the shared currency find demand and the EUR/USD pair was last seen losing 0.2% on a daily basis at 1.0460.

- A combination of factors dragged gold below the $1,800 mark, or its lowest level since May 16.

- Aggressive Fed rate hike bets and a goodish pickup in the USD demand exerted some pressure.

- Recession fears and the risk-off mood did little to lend any support to the safe-haven XAUUSD.

Gold prolonged this week's bearish trend and witnessed heavy follow-through selling on Friday, marking the fifth successive day of a negative move. The downward trajectory extended through the early part of the European session and dragged spot prices to the lowest level since May 16, around the $1,792 region in the last hour.

The prospects for more aggressive rate hikes by the US central bank were reaffirmed by Fed Chair Jerome Powell's remarks on Wednesday, saying that the US economy is well-positioned to handle tighter policy. Speaking at the ECB Forum in Sintra, Powell added that the Fed remains focused on getting inflation under control and the market pricing is pretty close to the dot plot. This, in turn, continued driving flows away from the non-yielding gold. Apart from this, broad-based US dollar strength further exerted downward pressure on the dollar-denominated commodity.

The combination of factors overshadowed the prevalent risk-off environment, which tends to benefit the safe-haven precious metal. The market sentiment remains fragile amid concerns that rapidly rising rates and tightening financial conditions would pose challenges to global economic growth. Adding to this, the ongoing Russia-Ukraine war has been fueling fears about a possible recession. This, in turn, tempered investors' appetite for perceived riskier assets, though did little to impress bullish traders or ease the bearish pressure surrounding gold.

The anti-risk flow was reinforced by the recent slump in the US Treasury bond yields, which, again, failed to lend any support to the yellow metal. With the latest leg down, spot prices now seem to have confirmed a fresh bearish breakdown below the $1,800 round-figure mark. Furthermore, acceptance below the said handle might have already set the stage for an extension of the depreciating move towards the YTD low, around the $1,780 region. The downward trajectory could get extended towards the next relevant support near the $1,755-$1,750 zone. Traders now look forward to the release of the US ISM Manufacturing PMI for a fresh impetus.

Technical levels to watch

Economist at UOB Group Ho Woei Chen, CFA, reviews the latest PMI results in the Chinese economy.

Key Takeaways

“China’s official manufacturing and non-manufacturing Purchasing Manager’s Indexes (PMIs) rebounded into the expansion territory (defined as reading above 50) in Jun after three months in contraction as Shanghai lifted lockdowns.”

“This reaffirms expectation of an economic recovery in China that will likely pick up momentum in the second half of the year alongside stimulus measures rollout. Underlying weakness in employment and selling/ output prices (for both manufacturing and non-manufacturing) indicate that the recovery remains fragile.”

“Given the fragile outlook, we maintain our view that there is room for further monetary policy easing. PBoC Governor Yi Gang recently suggested this will likely be via boosting credit rather than interest rate cuts as China’s ‘real interest rate is pretty low’.”

- EUR/GBP gained strong positive traction on Friday and shot back to the weekly high.

- Stronger Eurozone CPI figures reaffirmed ECB rate hike bets and boosted the euro.

- Cautious BoE, Brexit woes undermined the GBP and contributed to the strong move.

The EUR/GBP cross built on the overnight goodish rebound from mid-0.8500s, or a nearly two-week low and gained strong positive traction on the last day of the week. The buying interest picked up pace during the early part of the European session and pushed spot prices to the 0.8650-0.8655 region, back closer to the weekly high.

The shared currency's relative outperformance comes amid a clear signal by the European Central Bank that it would begin the rate hike cycle in June. Furthermore, a 50-bps hike in September is seen as an almost done deal and the bets were reaffirmed by stronger Eurozone consumer inflation figures released earlier this Friday.

According to the preliminary estimate published by Eurostat, the annualized Eurozone Harmonised Index of Consumer Prices (HICP) accelerated to 8.6% in June. This was well above market expectations for a rise to 8.4% from the 8.1% reported in May, which, in turn, was seen as a key factor that provided a fresh lift to the EUR/GBP cross.

On the other hand, the British pound was pressured by expectations that the Bank of England would adopt a gradual approach toward raising interest rates amid growing recession fears. Apart from this, concerns about fresh UK-EU tensions over the Northern Ireland Protocol of the Brexit agreement should act as a headwind for sterling.

The fundamental backdrop supports prospects for a further near-term appreciating move for the EUR/GBP cross. Hence, some follow-through strength towards reclaiming the 0.8700 mark, en-route the YTD peak around the 0.8720 region, remains a distinct possibility.

Technical levels to watch

- GBP/USD came under renewed selling pressure on Friday amid a goodish pickup in the USD demand.

- Aggressive Fed rate hike bets, recession fears and the risk-off mood underpinned the safe-haven buck.

- Expectations for a cautious BoE and Brexit jitters support prospects for a further depreciating move.

The GBP/USD pair met with a fresh supply on Friday and dropped back closer to a two-week low touched the previous day, with bears still awaiting sustained weakness below the 1.2100 mark.

A combination of supporting factors assisted the US dollar to regain positive traction on the last day of the week, which, in turn, exerted some downward pressure on the GBP/USD pair. The Federal Reserve’s non-stop chatter about rate hikes to curb soaring inflation, along with the prevalent risk-off mood, drove some haven flows towards the greenback.

Speaking at the ECB Forum in Sintra earlier this week, Fed Chair Jerome Powell lifted market bets for more aggressive rate hikes and said that the US economy is well-positioned to handle tighter policy. Powell further added that the Fed remains focused on getting inflation under control and that the market pricing is pretty close to the dot plot.

The Fed's hawkish outlook added to growing market concerns that rapidly rising rates and tightening financial conditions would pose challenges to global economic growth. Apart from this, a further escalation in tensions between the West and Russia - in response to the latter's invasion of Ukraine - has stoked fears of a possible recession.

This, in turn, continued taking its toll on the global risk sentiment and forced investors to take refuge in traditional safe-haven assets, including the buck. The global flight to safety was reinforced by the recent slump in the US Treasury bond yields, which acted as a headwind for the USD and helped limit losses for the GBP/USD pair, at least for now.

The bias, however, remains tilted in favour of bearish traders amid expectations that the Bank of England would adopt a more gradual approach to raising interest rates. Apart from this, the risk of fresh UK-EU tensions over the Northern Ireland Protocol of the Brexit agreement supports prospects for a further depreciating move for the GBP/USD pair.

Market participants now look forward to Friday's US economic docket, featuring the release of the US ISM Manufacturing PMI for a fresh impetus later during the early North American session. This, along with the US bond yields and the broader market risk sentiment, might influence the USD price dynamics and produce short-term opportunities around the GBP/USD pair.

Technical levels to watch

The annualized Eurozone Harmonised Index of Consumer Prices (HICP) surged by 8.6% in June vs. the previous reading of 8.1%, the latest data published by Eurostat showed on Friday. The market expected the bloc’s inflation to accelerate by 8.4%.

The core figures dropped to 3.7% YoY in June when compared to 3.9% expectations and 3.8% booked in May.

The Euro area figures are reported a day after Germany’s annual inflation for June eased from a record high, arriving at 8.2% while missing expectations of 8.8% following an 8.7% increase reported in May.

The bloc’s HICP figures hold significance, as it helps investors assess the European Central Bank’s (ECB) monetary policy normalization path. The ECB inflation target is 2%.

Key details (via Eurostat)

Looking at the main components of euro area inflation, energy is expected to have the highest annual rate in June (41.9%, compared with 39.1% in May), followed by food, alcohol & tobacco (8.9%, compared with 7.5% in May), non-energy industrial goods (4.3%, compared with 4.2% in May) and services (3.4%, compared with 3.5% in May).

EUR/USD reaction

EUR/USD caught a fresh bit on the mixed Eurozone inflation figures. The spot is now losing 0.14% on the day, trading at 1.0466. Hotter inflation will provide further headaches for the ECB ahead of the July 21 meeting, increasing the calls of the hawks for a 50 bps hike in July.

- EUR/USD resumes the downside well south of 1.0500.

- Germany June Final Manufacturing PMI came at 52.0.

- The US ISM Manufacturing will be the salient event later.

The selling bias re-emerged in the risk complex and drags EUR/USD back to the mid-1.0400s on Friday.

EUR/USD weak on risk-off trade, looks to data

EUR/USD rapidly fades Thursday’s rebound and refocuses on the downside on the back of the resumption of the buying pressure in the greenback, while the German 10y Bund yields attempt a mild rebound at the end of the week.

In the meantime, the risk aversion continues to dictate the price action around spot and the rest of the global assets, mainly in response to rising fears surrounding a potential global slowdown. In addition, the recent inaction of the ECB when it comes to its plans regarding the fragmentation issue also collaborates with the sour sentiment around the European currency.

In the domestic calendar, final figures saw the German and EMU Manufacturing PMI at 52.0 and 52.1, respectively, in June. Later in the session, ECB Board member F.Panetta us due to speak while the release of EMU flash inflation figures for the month of June will also be in the limelight.

Across the Atlantic, the final June Manufacturing PMI is due along the more relevant ISM Manufacturing.

What to look for around EUR

EUR/USD faces the re-emergence of the risk-off mood and the subsequent drop to the area well below 1.0500 so far this week.

In the meantime, the single currency continues to digest news from the ECB Forum in Portugal as well as any developments surrounding the bank’s plans to design a de-fragmentation tool in light of the upcoming start of the hiking cycle.

However, EUR/USD is still far away from exiting the woods and it is expected to remain at the mercy of dollar dynamics, geopolitical concerns and the Fed-ECB divergence, while higher German yields, persistent elevated inflation in the euro area and a decent pace of the economic recovery in the region are also supportive of an improvement in the mood around the euro.

Key events in the euro area this week: EMU, Germany Final Manufacturing PMI, EMU Flash Inflation Rate (Friday).

Eminent issues on the back boiler: Fragmentation risks. Kickstart of the ECB hiking cycle in July? Asymmetric economic recovery post-pandemic in the euro bloc. Impact of the war in Ukraine on the region’s growth prospects.

EUR/USD levels to watch

So far, spot is retreating 0.27% at 1.0454 and faces immediate contention at 1.0382 (weekly low June 30) seconded by 1.0358 (monthly low June 15) and finally 1.0348 (2022 low May 13). On the upside, a break above 1.0615 (weekly high June 27) would target 1.0773 (monthly high June 9) en route to 1.0786 (monthly high May 30).

- NZD/USD witnessed heavy selling on Friday and dived to its lowest level since May 2020.

- Aggressive Fed rate hike bets revived the USD demand and exerted downward pressure.

- Recession fears, the risk-off mood further drove flows away from the risk-sensitive kiwi.

The NZD/USD pair struggled to capitalize on the overnight modest recovery move and came under intense selling pressure on Friday. The intraday bearish trend extended through the early European session and dragged spot prices to the lowest level since May 2020, around the 0.6165 region in the last hour.

Speaking at the ECB's annual forum in Sintra on Wednesday, Fed Chair Jerome Powell lifted bets for more aggressive rate hikes and said that the US economy is well-positioned to handle tighter policy. Powell further added that the Fed remains focused on getting inflation under control and that the market pricing is pretty close to the dot plot. Adding to this, the prevalent risk-off environment boosted demand for the safe-haven US dollar and weighed on the risk-sensitive kiwi.

The prospects for a faster policy tightening by major central banks to curb soaring inflation, along with the ongoing Russia-Ukraine war, have been fueling fears about a possible recession. This, in turn, tempered investors' appetite for perceived riskier assets, which was evident from an extended sell-off in the equity markets. The combination of supporting factors assisted the USD to inch back closer to a 20-year high touched in June and exerted heavy downward pressure on the NZD/USD pair.

With the latest leg down, spot prices confirmed a fresh bearish breakdown below the 0.6200 round-figure mark. This was seen as another factor that aggravated the bearish pressure surrounding the NZD/USD pair and might have already set the stage for further losses. Furthermore, bearish technical indicators are still away from flashing oversold conditions and add credence to the negative outlook. Hence, some follow-through weakness, towards the next relevant support near the 0.6100 mark, remains a distinct possibility. Traders now look forward to the US ISM Manufacturing PMI for a fresh impetus.

Technical levels to watch

Gold has generally been fluctuating between $1,800 and a good $1,850 since mid-May. In the view of strategists at Commerzbank, nothing much is likely to unsettle the gold market in any serious way next week.

Gold will find it difficult to recover unless there is a reversal of ETF flows

“Gold is currently being held in check on two sides: higher interest rates and the firm US dollar are limiting gold’s upside potential as a non-interest-bearing investment, while the high inflation rates are preventing gold – in its capacity as a store of value – from sliding. This is not likely to change next week either, which is when the Fed will be publishing its latest meeting minutes.”

“The minutes will doubtless reflect the Fed’s determination to regain control of the high inflation by implementing sizeable rate hikes.”

“ETF investors have been turning their backs on gold again of late and selling shares. Unless there is a reversal of ETF flows, the gold price will likely find it difficult to recover.”

- Eurozone Manufacturing PMI dropped to a fresh 22-month low in June.

- EUR/USD trades deep in negative territory near 1.0450.

Economic activity in the eurozone's manufacturing sector expanded at its weakest pace in 22 months with the S&P Global Manufacturing PMI dropping to 52.1 (final) from 54.6 in May. This print came in slightly better than the market expectation and the flash estimate of 52.

Assessint the survey findings, "eurozone manufacturing has moved into decline in June, with production dropping for the first time for two years amid a steepening downturn in demand," said Chris Williamson, Chief Business Economist at S&P Global Market Intelligence. "Orders for goods have fallen at an accelerating rate over the past two months, dropping in June in every country surveyed with the exception of the Netherlands, and even here the rate of growth has weakened markedly in recent months."

Market reaction

The EUR/USD pair showed no immediate reaction to this report and was last seen losing 0.35% on the day at 1.0445.

- S&P Manufacturing PMI for Germany declined to 52 in June.

- Markets remain relatively calm ahead of EU inflation data.

Business activity in Germany's manufacturing sector expanded at a soft pace in June with the S&P Global Manufacturing PMI retreating to 52 (final) in June from 54.8 in May. This reading matched the previous estimate and the market expectation.

Commenting on the data, "we're seeing a rapid correction in underlying demand for German goods," said Phil Smith, Economics Associate Director at S&P Global Market Intelligence. "Inflows of new orders across the sector showed a deepening decline in June, as firms reported a degree of demand destruction from higher prices, growing market uncertainty, and multiple headwinds to export sales."

Market reaction

This report doesn't seem to be having a significant impact on risk sentiment with Germany's DAX 30 Index trading flat on the day at 12,787 points.

GBP/USD has failed to build on Thursday's modest recovery gains. As FXStreet’s Eren Sengezer notes, 1.2050 aligns as next bearish target amid risk aversion.

Cable remains technically bearish

“Investors continue to stay away from risk-sensitive assets ahead of the weekend.”

“On the downside, 1.2100 (static level, psychological level) aligns as immediate support. With a four-hour close below that level, additional losses toward 1.2050 (static level) and 1.2000 (psychological level) could be witnessed.”

“First resistance is located at 1.2120 (Fibonacci 23.6% retracement of the latest downtrend) ahead of 1.2170 (static level, 20-period SMA) and 1.2200 (Fibonacci 38.2% retracement).”

See: GBP/USD to retest the 1.1950 on a break under 1.21 – ING

- Silver continued losing ground on Friday and dived to a two-year low, below the $20.00 mark.

- The downward trajectory confirmed a fresh bearish break through an ascending trend channel.

- Oversold oscillators warrant some caution for bearish traders and positioning for further losses.

Silver remained under intense selling pressure on the last day of the week and weakened further below the $20.00 psychological mark during the early part of the European session. The downward trajectory dragged spot prices to the lowest level since July 2020, around the $19.85 region in the last hour.

With the latest leg down, the XAG/USD now seems to have confirmed a fresh breakdown through a one-month-old descending trend channel and seems vulnerable to extending the negative momentum. That said, oscillators on hourly/daily charts are flashing oversold conditions and warrant some caution for bearish traders.

This makes it prudent to wait for some near-term consolidation or a modest bounce before positioning for any further depreciating move. Nevertheless, the technical set-up supports prospects for an extension of the bearish trend and a fall to the next relevant support near the $19.60-$19.55 region.

On the flip side, any attempted recovery back above the $20.00 mark would attract fresh selling and remain capped near the ascending trend-channel support breakpoint, around the $20.25 region. The latter should now act as a pivotal point, which if cleared might trigger a near-term short-covering move.

The XAG/USD might then accelerate the momentum towards an intermediate hurdle near the $20.45-$20.50 area en-route the $21.00 round-figure mark.

Silver 4-hour chart

-637922583730106256.png)

Key levels to watch

No changes to the consolidation theme around USD/CNH in the near term, commented FX Strategists at UOB Group Lee Sue Ann and Quek Ser Leang.

Key Quotes

24-hour view: “We highlighted yesterday that ‘momentum indicators are neutral’ and we expected USD to ‘trade sideways within a range of 6.6900/6.7200’. Our view for sideway trade sideways was not wrong even though USD traded within a narrower range than expected (6.6902/6.7116). Further sideway-trading still appears likely, expected to be within a range of 6.6850/6.7080.”

Next 1-3 weeks: “We have expected USD to trade sideways between 6.6600 and 6.7400 since last Monday (20 Jun, spot at 6.7080). While shorter-term downward momentum has improved somewhat, there is no change in our view for now.”

- DXY starts the month in a positive tone around 105.00.

- US yields extend the downtrend across the curve.

- Flash Manufacturing PMI, ISM Manufacturing next of tap.

The greenback, in terms of the US Dollar Index (DXY), regains some composure and trespasses the 105.00 yardstick on Friday.

US Dollar Index now looks to data

The index keeps the weekly upside well in place and leaves behind Thursday’s pullback, as the selling pressure seems to have returned to the risk-associated universe at the end of the week.

The dollar, in the meantime, remains on track to close the week with moderate gains and at shouting distance from the cycle peaks around 105.80 recorded in June 15 on the back of the resumption of the risk aversion, recession fears, a corrective downside in US yields and expectations of further tightening by not only the Fed, but also from the other major central banks.

In the US data space, the manufacturing sector will take centre stage with the releases of the final June S&P Global Manufacturing PMI and the always relevant ISM Manufacturing.

What to look for around USD

Renewed risk-off sentiment motivated the index to reclaim the area around the 105.00 zone despite US yields continued to trend lower.

The dollar, in the meantime, remains well supported by the Fed’s divergence vs. most of its G10 peers (especially the ECB) in combination with bouts of geopolitical effervescence, higher US yields and a potential “hard landing” of the US economy, all factors suggesting a stronger dollar in the next months.

Key events in the US this week: ISM Manufacturing, Final Manufacturing PMI (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Escalating geopolitical effervescence vs. Russia and China. Fed’s more aggressive rate path this year and 2023. US-China trade conflict. Future of Biden’s Build Back Better plan.

US Dollar Index relevant levels

Now, the index is up 0.35% at 105.05 and a break above 105.54 (weekly high June 30) would expose 105.78 (2022 high June 15) and then 107.31 (monthly high December 2002). On the other hand, the next contention emerges at 103.67 (weekly low June 27) seconded by 103.41 (weekly low June 16) and finally 101.29 (monthly low May 30).

The first six months of 2022 have been marked by the dominance of the dollar. In the new quarter, economists at ING expect to see the same old dollar strength.

USD still in demand

“Our view remains that the dollar should continue to count on a rather solid floor in the third quarter thanks to the Fed’s front-loaded rate hikes and a still challenging environment for global risk assets due to tighter liquidity and fears of a global slowdown.”

“Some moderate dollar weakness may start to emerge in the fourth quarter when US rates peak.”

The GBP/USD pair was last seen retreating toward 1.21. Below here, cable could retest the 1.1950 low, economists at ING report.

Downside risks persist

“Brexit-related headlines should continue to come in over the coming days, but the pound may remain little touched by them for now.”

“A re-pricing of aggressive Bank of England expectations is the biggest risk for the pound, which also remains exposed to further risk sentiment instability.”

“Should we see a break below 1.21 in cable, the 1.1950 low could be re-tested soon.”

“When it comes to EUR/GBP, an almost equally unattractive euro should keep the pair around 0.86.”

EUR/USD continues to trade very close to the 1.05 gravity line. Today, all eyes will be on the eurozone-wide CPI figures for June. However, inflation figures are unlikely to impact the shared currency, economists at ING report.

EUR/USD may end the week in the 1.0430-1.0500 range

“The euro appeared to have a reduced sensitivity to the inflation prints this week, and this may well be the case today as markets seem to have cemented their ECB tightening expectations.”

“EUR/USD should remain mostly a function of global risk sentiment and USD dynamics and may end the week in the 1.0430-1.0500 range.”

See – EUR/USD: Eurozone inflation data unlikely to lift the shared currency – Commerzbank

FX option expiries for July 1 NY cut at 10:00 Eastern Time, via DTCC, can be found below.

- EUR/USD: EUR amounts

- 1.0400-05 937m

- 1.0425 287m

- 1.0450 521m

- 1.0475-80 914m

- 1.0500-05 454m

- 1.0520-25 363m

- 1.0540-55 2.0b

- 1.0565-75 2.6b

- 1.0590-00 2.53b

- 1.0615 611m

- 1.0630 994m

- GBP/USD: GBP amounts

- 1.2000 408m

- 1.2100 259m

- 1.2150 222m

- 1.2200 248m

- USD/JPY: USD amounts

- 133.50 1.47b

- 134.00 1.58m

- 135.25 295m

- 135.50 571m

- USD/CHF: USD amounts

- 0.9450 750m

- 0.9650-60 450m

- AUD/USD: AUD amounts

- 0.6800 754m

- 0.6900-10 816m

- 0.6950 337m

- 0.7000 400m

- 0.7050 1.96b

- NZD/USD: NZD amounts

- 0.6400 1.153b

EUR/GBP: EUR amounts

- 0.8600 329m

- 0.8635-40 276m

- USD/JPY lost ground for the second straight day and retreated further from a 24-year peak.

- Sliding US bond yields, recession fears benefitted the safe-haven JPY and exerted pressure.

- The Fed-BoJ policy divergence warrants some caution for bears amid modest USD strength.

The USD/JPY pair witnessed heavy selling for the second successive day on Friday and retreated further from its highest level since September 1998, around the 137.00 mark set on Wednesday. The corrective fall dragged spot prices further below the 135.00 psychological mark, closer to the weekly low during the early European session.

The prevalent risk-off environment - as depicted by a sea of red across the equity markets - drove haven flows towards the Japanese yen and exerted downward pressure on the USD/JPY pair. The market sentiment remains fragile amid concerns that a more aggressive move by major central banks to curb soaring inflation would pose challenges to global economic growth. Apart from this, a further escalation in tensions between the West and Russia - in response to the latter's invasion of Ukraine - has stoked fears of a possible recession.

The worsening global economic outlook forced investors to take refuge in traditional safe-haven assets, which was reinforced by the recent slump in the US Treasury bond yields. This resulted in the narrowing of the US-Japan yield differential, which further benefitted the JPY and prompted traders to lighten their bullish bets around the USD/JPY pair. That said, the divergent monetary policy stance adopted by the Federal Reserve and the Bank of Japan held back traders from placing aggressive bearish bets amid modest US dollar strength.

Speaking at the ECB Forum in Sintra on Wednesday, Fed Chair Jerome Powell said that the US central bank remains focused on getting inflation under control. Powell further added that the market pricing is pretty close to the dot plot and that the US economy is well-positioned to handle tighter policy. This, in turn, reaffirmed bets that the Fed would retain its faster policy tightening path and underpinned the USD. In contrast, the BoJ has repeatedly signalled that it would stick to its ultra-accommodative policy and keep borrowing costs at "present or lower" levels.

The mixed fundamental backdrop warrants some caution before confirming that the USD/JPY pair has topped out in the near term and positioning for a deeper correction in spot prices. Market participants now look forward to the release of the US ISM Manufacturing PMI, due later during the North American session. Apart from this, the US bond yields, the USD price dynamics and the broader market risk sentiment might provide a fresh impetus, which should allow traders to grab short-term opportunities around the major.

Technical levels to watch

AUD/NZD has rallied to recent highs of 1.1174. Benjamin Wong, Strategist at DBS Bank, retains constructive bias on the pair.

Terms of trade divergence favours the AUD over the NZD

Terms of trade divergence favours the AUD over the NZD, and unless the cross sustains losses under 1.0806, buying pullbacks is preferred.”

“Further upside targets a neckline calibrated target at 1.1251, followed by 1.1324.”

Here is what you need to know on Friday, July 1:

Following a volatile American session amid soft US inflation data and month-end flows on Thursday, markets stay relatively calm early Friday. Nevertheless, investors remain cautious ahead of June inflation figures for the euro area. In the second half of the day, the ISM Manufacturing PMI report will be featured in the US economic docket. The US Dollar Index recovers modestly toward 105.00 and the US stock index futures trade deep in negative territory.

ISM Manufacturing PMI Preview: High inflation component steal the show, boost dollar.

In an interview with Austrian newspaper Oberoesterreichische Nachrichten, European Central Bank (ECB) policymaker Robert Holzmann noted that he would have preferred the bank to hike its policy rate earlier. Eurostat is expected to report that the annual Harmonised Index of Consumer Prices (HICP) rose to 8.3% in June from 8.1% in May.

Eurozone Inflation Preview: Core holds the keys, with 4% set to trigger a EUR/USD rally.

Earlier in the day, the data from China showed that the Caixin Manufacturing PMI improved to 51.7 in June from 48.1 in May but this print doesn't seem to be having a positive impact on market sentiment in the early European session.

Meanwhile, cure oil prices fell sharply after OPEC+ decided to stick to its current plan of increasing the output by 648,000 barrels per day in August. The group refrained from discussing the output strategy from September. The barrel of West Texas Intermediate (WTI), which fell more than 3% on Thursday, was last seen losing 0.8% on the day at $105.15.

EUR/USD staged a decisive rebound during the American session and ended up closing in positive territory on Thursday. The pair stays on the back foot early Friday and edges lower toward 1.0450.

GBP/USD registered small daily gains on Thursday but turned south early Friday. The pair was last seen retreating toward 1.2100.

USD/JPY fell sharply on Thursday amid falling US Treasury bond yields. With the benchmark 10-year US T-bond yield losing nearly 2% below 3% so far on the day, the pair trades in negative territory below 135.00 in the European morning.

Gold failed to take advantage of falling yields and closed the fourth straight day in negative territory. Sellers continue to dominate XAU/USD's action early Friday with the pair trading below $1,800 for the first time since mid-May.

Although Bitcoin climbed above $20,000 on Friday after having dropped below that level on Thursday, it failed to preserve its recovery momentum and was last seen trading near $19,300. Ethereum continues to trade within a touching distance of $1,000.

The Japanese yen is the worst performing currency among the majors so far this year. But economists at Scotiabank believe that JPY’s slide may be slowing.

140 may be around the limit of the USD rise in this cycle

“We think that the apparent cap on US yields should be modestly JPY supportive and help stabilize the recent yen decline.”

“We noted that USD/JPY spot trends (higher highs) is diverging with the daily RSI (lower highs). This divergence is a classic sign that a move may be poised to reverse. There are scant signs of a reversal in terms of pure price action, however.”

“Firmer resistance is developing in 136.75/00 but the USD will have to trade below 134 at the moment in order to signal some (even modest) downside pressure is developing.”

“Given the extent of the USD rally so far this year, we are attentive to signs of a more significant reversal ahead of the 140 zone which we think may be around the limit of the USD rise in this cycle.”

- EUR/JPY drops for the fourth consecutive day as bears keep reins at the lowest levels in fortnight.

- Rush to risk-safety underpins bond, USD buying ahead of EU inflation data.

- Japan data join weak yields to exert additional downside pressure.

- Preliminary readings of Eurozone HICP for June will be important to watch, risk catalysts are the key.

EUR/JPY takes offers to refresh the fortnight low around 140.90 during early Friday morning in Europe. The yen cross traces moves of the Treasury yields amid the market’s pessimism surrounding the economic path forward.