- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- USD/JPY has moved marginally higher on downbeat Japan’s jobless data.

- The Unemployment data has landed at 2.6% while the Jobs/Applicants data has improved to 1.24.

- Investors’ focus will remain on US ISM PMI which is seen lower to 55.

The USD/JPY pair is aiming towards 136.00 as the Statistics Bureau of Japan has reported higher-than-expected Unemployment data. The jobless rate has improved to 2.6%, higher than the estimates and the prior print of 2.5%. While, the Jobs/Applicants ratio has improved to 1.24, higher than the former print of 1.23 but remains in line with the consensus of 1.24.

The higher jobless rate has weakened the Japanese yen against the greenback. The Bank of Japan (BOJ) has been keeping its ultra-loose monetary policy intact for a prolonged time to keep accelerating the aggregate demand. However, accelerating unemployment levels may force the BOJ to keep up with the prudent monetary policy as a tight labor market will always remain crucial for the Japanese economy.

Coming to the Tokyo inflation rate, the economic data has remained in a mid of estimates and the prior print of 2.2% and 2.4% respectively. A sustained inflation rate is lucrative for the yen bulls in the longer horizon.

On the dollar front, the US dollar index (DXY) is displaying some signs of exhaustion in the downside move and the pullback move is on the cards. The DXY witnessed an intense sell-off after the US CORE Personal Consumption Expenditure (PCE) Price Index landed along with the expectations of 4.9% but lower than the prior release of 4.9%. Even a minor fall in the inflation indicator seems lucrative for the risk-perceived assets. In today’s session, the spotlight will remain on the US ISM PMI numbers. The economic data is seen lower at 55 vs. 56.1 recorded previously.

- GBP/JPY prints four-day downtrend amid fears of recession, inflation.

- Japan’s inflation, unemployment rate increased, Tankan Large Manufacturing Index slumps.

- British government plans to cut VAT to battle the rising prices.

- UK Manufacturing PMI, risk catalysts will be crucial for immediate directions.

GBP/JPY remains pressured around 165.00 during the four-day downtrend amid early Friday morning in Asia.

The cross-currency pair’s latest moves could be linked to the downbeat US Treasury yields, as well as the UK’s failure to impress pound buyers despite announcing the plans to cut the Value Added Tax (VAT). Also exerting downside pressure on the GBP/JPY prices is news from Tokyo suggesting the record tax collection and mixed data.

Japan’s Tokyo Consumer Price Index (CPI) rose to 2.3% versus 2.2% expected and 2.4% prior in June while the nation’s Unemployment Rate for May increased to 2.6% compared to 2.5% market forecast and previous readings. Further, the Tankan Large Manufacturing Index for the second quarter (Q2) of 2022 slumped to 9 versus 13 expected and 14 prior.

Elsewhere, Nikkei came out with the news suggesting that Japan's tax revenue in the Financial Year 2021 reached a record 67 trillion yen.

On the other hand, Prime Minister Boris Johnson's chief of staff Steve Barclay suggested reducing the 20% headline rate of the tax, The Times said, adding a temporary cut would reduce the tax bill for millions, per Reuters. The news fails to impress the GBP/USD buyers as the actual outcome is yet to witness and the official announcement is pending as well.

Additionally, the final readings of the UK Gross Domestic Product (GDP) for Q1 2021 matched initial forecasts of 0.8% QoQ and 8.7% YoY.

It should be noted that the escalating fears of recession direct traders towards the US government bonds, which in turn exert downside pressure on the Treasury yields. That said, the US 10-year bond coupons dropped below 3.0%, before bouncing off to 3.01% at the closing, to portray around 50 basis points (bps) of a fall from June’s peak.

Looking forward, the final reading of the UK S&P Global/CIPS Manufacturing PMI for June, expected to confirm 53.4 initial forecasts, will be important to watch for fresh impulse. However, risk catalysts will be the key.

Technical analysis

The first daily closing below the 21-DMA in five weeks keeps GBP/JPY bears hopeful of revisiting the 50-DMA support, around 162.80 by the press time.

Alternatively, a one-week-old resistance line, near 166.20, adds to the upside filters even if the buyers manage to cross the immediate 21-DMA hurdle of 165.45.

- USD/CAD struggles inside the key DMA envelope after dropping the previous day.

- Fortnight-old descending trend line adds to the upside filters, bearish MACD favors further downside.

- 21-DMA holds the key to seller’s welcome, 10-DMA guards recovery.

USD/CAD fades bounce off intraday low around 1.2880 during Friday’s Asian session. In doing so, the Loonie pair remains pressured inside the familiar trading range between the 10-DMA and the 21-DMA by the press time.

It’s worth noting that the quote dropped the most in a week while reversing from the confluence of the 10-DMA and a two-week-old resistance line, around 1.2915-20 at the latest.

The pullback also gains support from the bearish MACD signals, which in turn challenge the quote’s corrective bounce afterward.

However, the 21-DMA support of 1.2837 precedes the weekly low near 1.2820 to challenge the short-term downside of the USD/CAD prices.

In a case where the pair stays weak past 1.2820, the odds of witnessing a south-run towards the 50% Fibonacci retracement of April-June upside, near 1.2740, can’t be ruled out.

On the contrary, a clear upside break of the 1.2920 hurdle could propel the USD/CAD pair towards the 1.3000 psychological magnet.

Following that, the double tops surrounding 1.3080 appear tough nut to crack for the bulls.

USD/CAD: Daily chart

Trend: Further weakness expected

- The AUD/JPY registered gains of almost 1.50% in June.

- A rising wedge in the AUD/JPY’s daily chart targets a fall towards 86.20s.

- The AUD/JPY in the near term is neutral-downward biased.

AUD/JPY prolongs its losses amidst a risk-off impulse weighing on global equities, sending investors scrambling toward safe-haven assets; in the FX complex being the Japanese yen and the Swiss franc, except the US dollar, undermined by falling US Treasury yields. At 93.67, the AUD/JPY is almost flat as the Asian Pacific session begins.

AUD/JPY Thursday’s price action illustrates consolidation in the last few days, within the 93.40-94.30 range, which buyers/sellers have been unable to break. AUD/JPY traders should note that the cross exchange rate is below the exponential moving averages (EMAs) in the 1-hour chart, signifying that downside risks remain in the short term.

AUD/JPY Daily chart

The AUD/JPY daily chart illustrates that the uptrend remains in play. Nevertheless, the pair’s falling below the 20-day EMA leaves it vulnerable to selling pressure, but the “damage” could be limited by the 50-day EMA at 92.41, followed by the June 16 swing low at 91.96. If that scenario plays out, it will also confirm the break of a rising wedge that targets the October 21, 2021 swing high-turned-support at 86.25.

AUD/JPY 1-Hour chart

In the near term, the AUD/JPY depicts a neutral-downward bias, confirmed by the EMAs and the Relative Strenght Index (RSI), which albeit almost trendless, remains below the 50-midline, in negative territory. Furthermore, a four-times tested downslope trendline suggests the pair is consolidating.

If the AUD/JPY breaks to the downside, its first support would be the June 30 daily low at 93.33. Once cleared, it would expose the S1 daily pivot at 93.23, followed by the June 26 low at 92.97. Contrarily, if the cross heads north, the AUD/JPY’s first resistance would be the 20-EMA at 93.74. Break above would expose the confluence of the 50, 100, and 200-EMAs, in the 93.85-88 range, followed by the R1 daily pivot at 94.20, followed by the June 22 high at 94.68.

AUD/JPY Key Technical Levels

- USD/CHF is inching higher after extending its recovery as DXY attempts a rebound.

- A decline in the US core PCE Price Index has resulted in a significant fall in the DXY.

- The improved Swiss Real Retail Sales have failed to support the Swiss franc bulls.

The USD/CHF pair has witnessed a modest rebound after hitting a low of 0.9535 in the New York session. The asset has successfully defended the responsive buying action recorded on Wednesday as the US dollar index (DXY) is eyeing a rebound after displaying a significant fall on Thursday.

The DXY witnessed a vertical downside move after attempting to renew its 23-year high at 105.78. The asset is trying to hold itself around 104.70 and may attempt a rebound amid its broader strength. A significant fall in the DXY is backed by an in-line rerelease of the US core Personal Consumption Expenditures (PCE) Price Index.

It is worth noting that the critical indicator of price levels has been advancing for the past few months and a minor slippage from the prior release of 4.9% indicates that the policy tightening measures have started showing their impact. However, the odds of a consecutive rate hike by 75 basis points (bps) are intact as the inflation rate at 8.6% is still more than four times higher than the desired rate of 2%.

In today’s session, investors’ focus will remain on the release of the US ISM PMI. As per the market consensus, the economic data may slip to 55 from the prior release of 56.1.

On the Swiss franc front, the release of the improved Real Retail Sales data has failed to provide any support to the Swiss franc bulls. The economic data released at -1.6%, higher than the prior print of -5.5% but lower than the estimates of 3.8%.

- GBP/USD fails to extend the corrective rebound from two-week low.

- No10 eyes reduction in VAT to battle inflation woes.

- Softer US spending, inflation weighed on the US dollar but broad pessimism put a floor under the fall.

- Fears of economic slowdown can keep grinding the pair lower, PMIs for June will be important for the day.

GBP/USD takes offers to refresh the intraday low around 1.2165, paring the biggest daily gains in a fortnight during Friday’s initial Asian session. In doing so, the Cable pair fails to cheer the news suggesting the UK government’s plan to ease the Value Added Tax (VAT) to counter the risk emanating from the price rise.

Prime Minister Boris Johnson's chief of staff Steve Barclay suggested reducing the 20% headline rate of the tax, The Times said, adding a temporary cut would reduce the tax bill for millions, per Reuters. The news fails to impress the GBP/USD buyers as the actual outcome is yet to witness and the official announcement is pending as well.

On the other hand, downbeat US personal spending and softer prints of the Fed’s preferred inflation gauge raised concerns over the health of the world’s largest economy and drowned the US dollar on Thursday. The greenback’s retreat could also be linked to the downbeat US Treasury yields as the benchmark 10-year bond coupons dropped below 3.0%, before bouncing off to 3.01% at the closing, to portray around 50 basis points (bps) of a fall from June’s peak.

That said, the US Dollar Index (DXY) reversed from a 12-day high to snap a two-day uptrend by closing the day around 104.75.

The recession fears, alternatively, kept the market’s risk appetite weak and weighed on the equities even as the yields were down and the dollar too.

It’s worth noting that the US Personal Income for May matched market forecasts and upwardly revised figures of 0.5% MoM but Personal Spending dropped to a three-month low, to 0.2% versus 0.5% expected and 0.6% downwardly revised previous readings. Further, the Personal Consumption Expenditure (PCE) Price Index reprinted 6.3% YoY figures for May.

More importantly, the Core PCE Price Index, the Fed’s preferred inflation gauge, matched expectations of 4.7% YoY versus 4.9% prior.

On the other hand, the final readings of the UK Gross Domestic Product (GDP) for Q1 2021 matched initial forecasts of 0.8% QoQ and 8.7% YoY.

Looking forward, the final reading of the UK S&P Global Manufacturing PMI for June precedes the US ISM Manufacturing PMI for the said month to direct intraday moves.

Also read: ISM Manufacturing PMI Preview: High inflation component steal the show, boost dollar

Technical analysis

Unless crossing a three-week-old resistance line, near 1.2250, GBP/USD remains vulnerable to refresh yearly low, currently around 1.1933.

- EUR/USD fades bounce off two-week bottom, pares biggest daily gains in a fortnight.

- Softer US spending, PCE inflation propelled growth concerns and weighed on the USD.

- Market sentiment remains weak amid recession, inflation fears.

- Eurozone inflation, US ISM Manufacturing PMI for June will be important to watch for the day.

EUR/USD fails to extend the previous day’s corrective pullback from a fortnight low, easing around 1.0480-75 during Friday’s initial Asian session. The major currency pair benefited from the broad US dollar pullback on Thursday before retreating ahead of another round of important data points.

Softer US spending and inflation figures amplified recession concerns for the world’s largest economy and drowned the US dollar on Thursday. The greenback’s retreat could also be linked to the downbeat US Treasury yields as the benchmark 10-year bond coupons dropped below 3.0%, before bouncing off to 3.01% at the closing, to portray around 50 basis points (bps) of a fall from June’s peak.

It should be noted, however, that the equities couldn’t cheer downbeat Treasury yields, nor the softer US dollar, amid fears of economic slowdown.

That said, the US Dollar Index (DXY) reversed from a 12-day high to snap a two-day uptrend by closing the day around 104.75.

Talking about the data, On Thursday, the US Personal Income for May matched market forecasts and upwardly revised figures of 0.5% MoM but Personal Spending dropped to a three-month low, to 0.2% versus 0.5% expected and 0.6% downwardly revised previous readings. Further, the Personal Consumption Expenditure (PCE) Price Index reprinted 6.3% YoY figures for May.

More importantly, the Core PCE Price Index, the Fed’s preferred inflation gauge, matched expectations of 4.7% YoY versus 4.9% prior.

On the other hand, German Retail Sales for May dropped below -2.0% market forecast to -3.6% YoY, versus -0.4% previous readings whereas the Eurozone Unemployment Rate declined to 6.6% versus 6.8% expected and 6.7% prior.

Looking forward, the initial readings of the Eurozone key inflation gauge, Harmonised Index of Consumer Prices (HICP), will precede the US ISM Manufacturing PMI for June to direct short-term EUR/USD moves.

Technical analysis

A daily closing below the ascending trend line support from May 13, near 1.0440 by the press time, appears necessary for the EUR/USD bears to refresh the yearly low. Otherwise, a three-week-old resistance line, near 1.0565, could lure the counter-trend traders.

- A double bottom formation is signaling a bullish reversal going forward.

- Aussie bulls are attempting to balance above the 50-period EMA.

- The RSI (14) is oscillating in a 40.00-60.00 range which signals a consolidation ahead.

The AUD/USD pair is going through a correction phase after facing barricades around 0.6920 in the New York session. The asset displayed some signs of reversal on Thursday after finding bids while testing two-week-old support at 0.6850.

Aussie bulls have displayed a Double Bottom formation after sensing lower selling pressure while attempting to violate June 14 low at 0.6850. The appearance of a light selling pressure while testing the prior crucial support results in a short-term bounce that demands more filters to turn into a bullish reversal. The trendline placed from June 16 high at 0.7070 will act as a major resistance for the counter.

The antipodean is attempting to sustain above the 50-period Exponential Moving Average (EMA) at 0.6896, which will strengthen the aussie bulls further. While the 200-period EMA at 0.6925 is higher than the asset, which clears that the long-term trend is still down.

Meanwhile, the Relative Strength Index (RSI) (14) is oscillating in the 40.00-60.00 range, which signals the consolidation phase ahead.

The aussie bulls could lift the asset price higher if the major overstep Wednesday’s high at 0.6965. This will drive the asset towards the psychological resistance at 0.7000, followed by June 13 high at 0.7035.

On the flip side, the aussie bulls could lose their grip if the asset drops below June 23 low at 0.6868. This will drag the asset towards May 12 low and the round-level support at 0.6829 and 0.6800 respectively.

AUD/USD hourly chart

-637922254002071346.png)

- The GBP/JPY closed in June with solid gains of almost 2%, as depicted by the weekly chart.

- From the daily chart perspective, the GBP/JPY is upward biased, but the pair tumbling below the 20-day EMA exposes the GBP/JPY to further selling pressure.

- GBP/JPY in the near term is neutral-downward biased and might accelerate its losses if sellers reclaim 164.65.

The British pound ended June with gains of almost 2% against the Japanese yen, but on the last trading day of the month, it recorded a loss of 0.19%, extending its fall to three straight days in the middle of a dampened market mood. At the time of writing, the GBP/JPY is trading at 165.24, barely up 0.04% as the Friday Asian session begins.

On Thursday, the GBP/JPY extended its fall, which began on June 28, when the pair reached a weekly high of around 166.94 and made a U-turn, which sent the pair tumbling towards a June 29 low at 169.39. That said, the GBP/JPY opened near the day’s highs and dropped towards the current week’s low around 164.80.

GBP/JPY Daily chart

The GBP/JPY daily chart illustrates the pair as upward biased in the long term, but a break below the 20-day EMA, at 165.44, leaves the cross-currency pair exposed to selling pressure. GBP/JPY sellers need to reclaim the June 23 daily low at 164.65 if they would like to extend the fall. If that scenario plays out, the next support would be the 50-day EMA at 162.69. Otherwise, the GBP/JPY’s first resistance would be the 20-day EMA at 165.44, followed by the June 28 high at 166.94.

GBP/JPY 1-Hour chart

In the 1-hour chart, the GBP/JPY illustrates a negative story in the short term. Since June 28, the pair fell 1.28%, more than 200-pips, courtesy of the Sterling weakness, which has bolstered the yen. In fact, price action is within a descending channel, showing the formation of a bullish flag. Nonetheless, further losses are expected if the GBP/JPY breaks below 164.65. Otherwise, the GBP/JPY first resistance would be the 20-EMA at 165.26, followed by the R1 daily pivot at 165.83, followed by the 200-EMA at1 65.98.

GBP/JPY Key Technical Level

"European Central Bank (ECB) policymaker and fiscal hawk Robert Holzmann would have preferred earlier action on interest rates than the ECB's current plan to raise them in July for the first time in more than a decade, he said in remarks published on Thursday,” per Reuters.

During an interview with Austrian newspaper Oberoesterreichische Nachrichten, ECB’s Holzmann also said, per Reuters, “From my Austrian point of view, I would have preferred earlier moves on interest rates but I am only one of 25 at the European Central Bank (Governing Council)."

Additional comments

We do not know how wage negotiations will go.

It will take some time to reach 2% inflation target.

Market reaction

The news appears to have failed in favoring Euro as the EUR/USD was last seen paring the biggest daily gains in a fortnight at around 1.0480.

- Gold price is likely to slip below $1,800.00 as odds of a 75 bps rate hike by the Fed have advanced.

- Fed’s focus is on bringing price stability to the economy.

- The activation of the descending triangle will send the gold prices deep into the negative trajectory.

Gold price (XAU/USD) is establishing below $1,810.00 after facing a steep fall while attempting a bullish reversal on Thursday. The precious metal is hovering near a fresh two-week low at $1,802.78 and is aiming to balance below the psychological support of $1,800.00. The release of the US core Personal Consumption Expenditures (PCE) Price Index at 4.7% has bolstered the odds of one more 75 basis points (bps) interest rate hike by the Federal Reserve (Fed) in July.

The US core PCE Price Index remained in line with the estimates but lower than the prior release of 4.9%. This indicates that the elevation of interest rates by the Fed to 1.50-1.75% in its past three monetary policy meetings has failed to make a substantial change in the price levels. Also, the Fed is ‘unintentionally committed’ to bringing price stability to the economy. Therefore, it will do ‘whatever it takes’ to cool off the red-hot inflation.

Going forward, the focus will remain on the US ISM PMI. A preliminary estimate for the economic data is 55, lower than the prior release of 56.1.

Gold technical analysis

On an hourly scale, the gold prices are expected to slip significantly below the psychological support of $1,800.00, which will activate the Descending Triangle formation. The downward sloping trendline of the chart pattern is placed from June 16 high at $1,857.58 while the horizontal support is plotted from June 14 low at $1,805.11. The gold bears have defended the 100-period Exponential Moving Average (EMA) at $1,820.11. Meanwhile, the Relative Strength Index (RSI) (14) will bring a fresh downside move after slipping below the 40.00.

Gold hourly chart

Here is what you need to know for Friday, July 1:

Risk-off was the theme on Thursday across most markets. Being the final day of the month, quarter, and half-year, there were some important developments which keep the outlook for the new quarter concerning global growth.

Weak inflation-adjusted consumer spending in the US only adds to these concerns and in turn, equities and rates lower are being pushed lower. US yields fell, with the 10-year down to a low of 2.97%, below the 3.00% psychological level, around 50bp below the peaks hit earlier in June. Equities were also weaker, with the S&P 500 down 1%.

In FX, DXY extended above 105.000 but fell sharply with the Yen regrouping as yields drop. The dollar rally remains largely intact, given rising worries about a global recession, although data on Thursday was far from impressive and did nothing to allay concerns about the US economy sinking towards a recession.

The highlights of Thursday's data schedule were a faster monthly pace of growth in the PCE price index, steady personal income expansion, and slower spending growth. Personal income was up 0.5% in May, right on expectations after a 0.5% gain in the previous month.

In other data, the Chicago PMI fell to 56.4 in June from 60.3 in May. Other manufacturing data already released have suggested slower growth or outright contraction. The ISM's national index will be released on Friday. Initial jobless claims decreased by 2,000 to 231,000 in the week ended June 25, but the four-week moving average rose by 7,250 to 231,750, continuing the string of gains.

The euro recovered on Thursday from a two-week low against the dollar, which sputtered after fresh inflation data showed US consumer spending rose less than expected in May. EUR/USD hit a high of 1.0488 and closed the North American session within that vicinity after reversing a decline sparked by increasing recession jitters in the eurozone and the energy crisis stoked by the war in Ukraine. For the start of the quarter, traders are going to be looking at eurozone inflation figures due on Friday which could give some insight as to how aggressive the ECB might be in hiking rates.

The yen regathered below the 24-year peak of 137 vs. the dollar although the gap between a hawkish Federal Reserve and a dovish Bank of Japan continues to weigh heavily on the Japanese currency. USD/JPY fell to 135.55. The yen was down 15% against the US dollar for the first six months of 2022, which makes for the worst first-half of year performance for the currency since 2013.

Gold declined in its worst quarter since early 2021 and is back to test $1,800. In cryptocurrencies, bitcoin fell below the $20,000 milestone level and the US Securities and Exchange Commission rejected a proposal to list a spot bitcoin exchange-traded fund by digital asset manager Grayscale. Bitcoin last fell to $18,595 and is down some 58% in the first six months of 2022, its worst first-half of year showing ever. West Texas Intermediate (WTI) crude oil also dropped sharply as concerns of a recession.

- A soft US dollar boosts appetite for risk-sensitive currencies in the FX space, so the NZD rises.

- The US 10-year Treasury yield dips below the 3% threshold, undermining the greenback.

- US recession fears increased after GDP for the first quarter contracted -1.5%, while Atlanta’s Fed GDPNow projections for the Q2 lie at -1.0%.

Broad US dollar weakness bolstered the New Zealand dollar on Thursday after mixed US economic data was released, which did not change the sour mood surrounding the financial markets since the beginning of the week. At 0.6247, the NZD/USD climbs nearly 0.50% during the North American session at the time of writing.

The greenback dipped on lower inflation expectations and falling US Treasury yields

As mentioned above, a soft US dollar is the main reason for the NZD/USD gains. The fall in US Treasury yields and lower US inflation expectations, as shown by the five and 10-year FRED Breakevens, undermined the greenback. Investors are backpedaling an aggressive Fed, and as illustrated by STIRs money market futures, traders expect the Federal funds rate to end at around 3.50% in twelve months.

Sentiment-wise, increased fears that the US could hit a recession were exacerbated by a weaker than expected consumer spending in May, alongside the Atlanta Fed’s GDPNow for the Q2, which plunged to -1.0%. Meanwhile, Wall Street is about to finish the first half of 2022 with substantial losses. The US Dollar Index, a gauge of the buck’s value, retreated from weekly highs near 105.541 and slid 0.35% down to 104.733.

On Thursday, US economic data was released. The US Bureau of Economic Analysis reported the PersonaLConsumption Expenditure (PCE) Price Index for May, which climbed by 6.3% YoY, less than estimations, while core PCE, the Fed’s favorite reading for inflation, heightened by 4.7% YoY, lower than expected.

At the same time, the US Department of Labour released the Initial Jobless Claims for the week ending on June 25, which topped above the 228K expected, and rose by 231K.

In the meantime, the Federal Reserve chair Jerome Powell crossed wires. He said policymakers’ job is to find price stability, even during the new forces of inflation, while adding that the US economy is solid and can withstand monetary policy adjustments.

The New Zealand economic calendar will feature the ANZ Roy Morgan Consumer Confidence for June is expected at 8, alongside the New Zealand Building Permits for May. On the US front, the calendar will reveal the S&P Global Manufacturing PMIs alongside the ISM Manufacturing PMI.

NZD/USD Key Technical Levels

- Gold bears are putting pressure on the bulls at a critical area on the daily chart.

- Gold prices are under pressure despite rising recession odds.

At $1,806, the gold price is lower by some 0.66% after falling from a high of $ $1,825.21 to a session low of $1,802.77, breaking out of its consolidation range. Traders have moved out of the yellow metal even as stocks, the dollar and bond yields fell.

The drop came even as investors moved out of equities, with the S&P 500 Index last seen down 1.25% on what has been a mixed week in sentiment and data. The highlights of Thursday's data schedule were a faster monthly pace of growth in the PCE price index, steady personal income expansion, and slower spending growth. Personal income was up 0.5% in May, right on expectations after a 0.5% gain in the previous month.

After an adjustment for a 0.6% increase in the PCE price index, real personal consumption was down 0.4% in May after a 0.3% increase in April. Core PCE prices rose by 0.3% for the fourth straight month, slowing the year-over-year rate to 4.7% from 4.9% in the previous month. Gold briefly bounced after the US data but quickly moved back into the tight range it has been in for the past few sessions.

In other data, the Chicago PMI fell to 56.4 in June from 60.3 in May. Other manufacturing data already released have suggested slower growth or outright contraction. The ISM's national index will be released on Friday. Initial jobless claims decreased by 2,000 to 231,000 in the week ended June 25, but the four-week moving average rose by 7,250 to 231,750, continuing the string of gains.

Meanwhile, the US dollar also fell, making gold more affordable for international buyers, with the DXY dropping to 104.645 the low of the day so far. US bond yields fell sharply, which is offering a lifeline to the precious metal since it pays no interest. The yield on the US 10-year note was last seen down at 2.980%, near its three-week low made earlier at 2.97%

''Gold prices are under pressure despite rising recession odds, in contrast to recent price action pointing to safe-haven flows supporting the yellow metal,'' analysts at TD Securities said.

''In fact, gold prices have disconnected altogether from market pricing for Fed hikes over the past month, and have instead grown their relationship with the USD, pointing to a smaller magnitude of idiosyncratic flows for the yellow metal.

''While the bias remains to the downside in gold, participants will need a catalyst to shake out the complacent longs in precious metals.''

Gold technical analysis

The bears have moved in on a critical area that could be broken that will give way to the potential of a deeper run towards $1,720.

- The USD/CHF daily chart illustrates a double top formation, but solid buying pressure below 0.9540s capped any downward moves.

- Risk-off impulse bolstered the appetite for the Swiss franc and weighed on the US dollar.

- USD/CHF 1-hour chart is tilted to the upside, but unless buyers reclaim 0.9600, the major is vulnerable to selling pressure.

The USD/CHF retreats from the 0.9600 figure after an earlier USD rally that faltered to break above the former figure, and so far has retraced just above the 100-day moving average (DMA), which lies near 0.9514. At the time of writing, the USD/CHF is trading at 0.9540 in the North American session.

Sentiment is still dismal due to renewed fears that high inflation and a global economic slowdown are a stagflation scenario. US equities are under pressure for their worst percentage fall since the 1970s, while the US Dollar turned negative and remains below the 105.000 figure, losing 0.38%.

That said, the USD/CHF seesawed around the 0.9546-0.9594 on mixed US economic data, followed by a drop towards Thursday’s central daily pivot point at 0.9540, a level where the major settled in.

USD/CHF Daily chart

The double top in the USD/CHF daily chart is still in play, though USD/CHF sellers are struggling to achieve a decisive break below the May 27 daily low at 0.9544. USD/CHF traders should be aware that the 100-DMA is meandering around that price level, though some 15 pips above the 0.9500 figure. A decisive break would send the major to probe the 100-DMA, followed by 0.9500, and then the March 16 high at 0.9460.

USD/CHF 1-Hour chart

The USD/CHF, hourly time frame depicts the pair as consolidating but slightly tilted to the upside. The weekly low recorded Wednesday, around 0.9495, propelled the major upwards. However, the confluence of the 50 and 100-simple moving averages (SMAs) around 0.9553-61 capped the pair upside after the major dropped on mixed US data. Break below 0.9529 would send the USD/CHF towards 0.9495; otherwise, the major would be vulnerable to buying pressure. In that scenario, if USD/CHF buyers reclaim the 200-SMA at 0.9599, that would clear the way for further gains.

USD/CHF Key Technical Levels

- USD/CAD is under pressure as the US dollar slides from recent highs.

- The price of oil, one of Canada's major exports, fell sharply, but hawkish BoC eyed.

USD/CAD is trading at 1.2868 and is off by some 0.2% after falling from a high of 1.2933 to a low of 1.2861 and is on track for a steep quarterly decline. On Thursday, the US fell from a two-week high against a basket of peers, with the index last down 0.38% at 104.70.

Both stocks and the US dollar came under pressure and data showed that Chicago-area business activity fell more than expected in June, according to data released Thursday. The Chicago Business Barometer slid to 56.4 this month from May's reading of 60.3, according to the Institute for Supply Management and Market News International. The consensus on Econoday was for a print of 58.4. Investors worry that the latest show of central bank determination to tame inflation will cause economies to slow rapidly.

Domestically, Canada's economy likely declined 0.2% in May, following a gain of 0.3% in April which matched estimates. This leaves the Bank of Canada on track to hike interest rates by three-quarters of a percentage point at its next policy decision on July 13, which would be its biggest hike in 24 years.

Meanwhile, the price of oil one of Canada's major exports fell sharply on Thursday on recession worries and signs US gasoline demand may be easing amid high prices. WTI crude oil for August delivery closed down US$4.02 to settle at US$105.76 per barrel, Marketwatch reported. August Brent crude, the global benchmark, was down US$1.44 to US$114.82, while Western Canada Select was down US$3.86 to US$87.63 per barrel.

The slide comes after the Energy Information Administration on Wednesday reported US oil inventories fell more than expected last week. However, price action still isn't pointing to demand-side constraints, given the still-extremely elevated crack spreads suggest that demand for crude oil will remain elevated nonetheless, analysts at TD Securities argued. ''Product inventories are at critically low levels, which also suggests restocking will keep crude oil demand strong.''

According to analysts at Wells Fargo, the mix of measured monetary tightening and rapid inflation, combined with the slowdown in UK economy, provides an underwhelming backdrop for the pound. They revised their forecast for the GBP/USD lower and now see it around 1.1700 in mid-2023.

Key Quotes:

“We expect the U.K. central bank to begin lowering its policy interest rate during the second half of 2023, by a cumulative 50 bps to 1.50% by the end of next year.”

“Overall, this mix of gradual monetary tightening and rapid inflation (meaning that real U.K. policy interest rates will remain substantially in negative territory), combined with a U.K. economic downturn, provides an underwhelming backdrop for the U.K. currency. We have revised our forecast for the pound lower, and now see a trough in the GBP/USD exchange rate around $1.1700 in mid-2023.”

“Even as the U.S. economy falls into its own recession and the Fed begins to lower interest rates by late next year, we believe that headwinds facing the U.K. economy will mean only a modest rebound for the pound, and we target a GBP/USD exchange rate of $1.1900 by the end of 2023.”

Data released on Thursday showed Canada’s Real GDP rose 0.3% in April on a monthly basis in line with market consensus. Analysts at CIBC point out the Canadian economy is slowing down but not in a way that suggests inflation will do the same.

Key Quotes:

“Growth in the Canadian economy is cooling, but not entirely in a way that will convince policymakers that inflation will do the same. Monthly GDP increased by 0.3% in April (in line with the consensus forecast), but advance data for May points to a decline of 0.2% during that month. However, declines in mining, oil & gas and manufacturing suggest that the monthly drop in May was at least partly due to supply issues rather than slowing demand, which could add to, rather than subtract from, current inflationary pressures.”

“For Q2 as a whole, GDP appears to be tracking just below a 4% annualized pace, compared to the 6% rate the Bank of Canada had forecast in its April MPR. However, other than perhaps a quicker retreat in housing activity, the slower than projected growth appears to be due to supply rather than demand side factors. As a result, it will do little to ease the Bank of Canada's concerns regarding current inflationary pressures. A slowing in other elements of domestic demand, including in retail sales and consumer-facing services, is expected to show up more during the second half of the year, with households currently able to use the excess savings put aside during the pandemic to cushion the blow of high inflation and interest rate increases.”

- The AUD/USD grinds higher despite a dampened market mood on a weaker greenback.

- Fed’s favorite gauge of inflation eases, but also consumer spending takes a hit, could the US economy support higher rates?

- Atlanta Fed’s GDPNow for the Q2 plunges towards -1.0%.

- AUD/USD Price Forecast: Seesawing around 0.6850-0.6950 as the pair consolidates in that area.

AUD/USD stages a recovery after plunging to fresh two-week lows around 0.6850s, reclaiming the 0.6900 figure, nearly gaining 0.60% on Thursday, after US inflation shows some signs of topping. At the time of writing, the AUD/USD trades at 0.6910 during the North American session.

A risk-off mood struck the financial markets on the last day of the first half of 2022. US equities extend their losses, and the greenback is falling, as shown by the US Dollar Index slumping 0.39%. Meanwhile, the US 10-year Treasury yield nosedives below the 3% threshold as recession fears increase, as illustrated by the Atlanta Fed’s GDPNow for the Q2 plunges towards -1.0%.

US inflation shows signs of easing; consumer spending falls

The US calendar reported inflation figures, which showed that it is slowing down. The Personal Consumption Expenditure (PCE) Price Index for May climbed by 6.3% YoY, less than foreseen, while core PCE, the Fed’s favorite reading for inflation, heightened by 4.7% YoY, lower than estimated, the US Bureau of Economic Analysis reported. Albeit a good sign for the US economy, the same report highlighted that American consumers spent less in May, for the first time in 2022, and previous numbers were downward revised, indicating that the economy is not as strong as thought.

At the same time, the US Department of Labour released the Initial Jobless Claims for the week ending on June 25, which topped above the 228K expected, and rose by 231K.

In the meantime, the Federal Reserve chair Jerome Powell crossed wires. He said policymakers’ job is to find price stability, even during the new forces of inflation, while adding that the US economy is solid and can withstand monetary policy adjustments.

Australia’s economic docket will feature the S&P Global Manufacturing PMI for June. Across the pond, the US docket will reveal S&P Global Manufacturing PMIs alongside the ISM Manufacturing PMI.

AUD/USD Price Forecast: Technical outlook

The AUD/USD remains in a downtrend, though slightly consolidating n the 0.6850-0.6950 range. Further confirmation of the previously-mentioned is the location and slope of the Relative Strength Index (RSI), albeit, at negative readings, it is almost horizontal. Nevertheless, the major’s price action on Thursday is rising sharply, and a break above the June 30 high at 0.6920 might open the door for further gains, but solid resistance near 0.7000 will be challenging to overcome. Contrarily, a continuation to the downside is in play, though it would accelerate once sellers reclaim 0.6850, which will send the pair tumbling towards the YTD low near 0.6828, followed by 0.6800.

- The greenback makes a U-turn and begins to weaken; after the London Fix, the pound recovers.

- Stagflation fears keep investors’ flows going through safe-haven assets, except the US dollar.

- GBP/USD Price Forecast: Range-bound, but a break above 1.2212 might open the door for further upside; otherwise, a re-test of YTD lows is on the cards.

The British pound recovered from two-week lows and is advancing just above 1.2150, after sliding below the 1.2000 mark, for the first time since mid-June, when the GBP/USD collapsed towards 1.1933 YTD lows. At 1.2176, the GBP/USD records solid gains, as the year’s first half is near to end.

Half/quarter/month-end flows finished; consequently, the buck drops

The market mood remains negative, though it was not an excuse for the pound to recover some ground. US equities are tumbling, and US Treasury yields followed suit, boosting the GBP/USD upside. In the meantime, the US Dollar Index, a measure of the greenback’s performance vs. six peers, after reaching a weekly high at around 105.541, dives 0.34%, sitting at 104.736, undermined by the fall in US bond yields.

Worries about a global recession and stagnation scenario keep investors on their toes. On Thursday, US inflation showed some signs of slowing down, as the US Bureau of Economic Analysis reported. The US Personal Consumption Expenditure (PCE) Index for May, rose 6.3% YoY, lower than expected. The so-called core PCE, the Fed’s preferred gauge of inflation, downtick from 4.8% YoY foreseen to 4.7%.

At the same time, the US Department of Labour released the Initial Jobless Claims for the week ending on June 25, which topped above the 228K expected, and rose by 231K.

In the meantime, the Federal Reserve chair Jerome Powell crossed wires. He said policymakers’ job is to find price stability, even during the new forces of inflation, while adding that the US economy is solid and can withstand monetary policy adjustments.

In the same event hosted by the ECB, the Bank of England Governor Andrew said the pound was “one of the many influences on inflation” and added that he was not surprised by its recent weakness. Bailey acknowledged that the UK’s economy is weakening sooner and somewhat more than other counterparties.

The UK economic calendar will feature June’s S&P Global/CIPS Manufacturing PMI readings in the week ahead. Across the pond, the US docket will reveal S&P Global Manufacturing PMIs alongside the ISM Manufacturing PMI.

GBP/USD Price Forecast: Technical outlook

From a technical perspective, the GBP/USD is still downward biased, but sellers unable to re-test the YTD lows, near 1.1933, has opened the door for further gains. If the GBP/USD breaks above the June 29 high at 1.2212, that will pave the way for a rally to the 20-day EMA at 1.2293. Otherwise, the major will consolidate until GBP sellers can drag the pound towards the YTD lows near the 1.1930s.

Data released on Thursday, showed real consumer spending fell 0.4% in May while April’s numbers were revised lower. Today's details on monthly spending figures show a much weaker profile for spending in the first five months of the year and sets the scenario for a weaker growth in the second quarter than the data would have suggested just 48 hours ago, explained analysts at Wells Fargo.

Key Quotes:

“Yesterday's GDP revisions that lowered estimates for first quarter consumer spending was just a jab; today's May personal income and spending report was the uppercut. Real consumer spending dropped 0.4% in May and prior monthly spending figures were revised lower. At least inflation did not get materially worse; the headline PCE deflator rose less than expected to 6.35%.”

“There is not much that is good about today's report, but something that is at least “less bad” is that the PCE deflator rose “just” 0.6% in May which only marginally lifted the year-over-year rate of inflation to 6.35% from 6.29% previously.”

“With the third estimate of first-quarter GDP, which revised real personal consumption expenditures (PCE) lower to reflect a 1.8% annualized pace of growth, and this sharp decline in May, estimates for second quarter PCE growth will likely be coming down. Even so, our overall expectations for consumer spending have not materially changed. We continue to expect consumers will increasingly rely on their balance sheets to fund spending in the near term despite persistently higher inflation.”

- USD/MXN turns negative, after hitting weekly highs near 20.30.

- A recovery in market sentiment helped the Mexican peso during the American session.

- A consolidation above 20.20 is likely to trigger more gains.

Emerging market currencies recovered ground during the American session from multi-day lows. They remain under pressure affected by the sharp decline in global stocks. The negative growth outlook and monetary tightening from the Fed weigh on currencies like the Mexican peso.

The USD/MXN peaked on Thursday at 20.26, the highest level in a week. Later as stocks recovered, pulled back erasing gains. Despite moving off highs, the outlook is biased to the upside. At the first attempt, the dollar was rejected from above 20.20. If it posts a daily close above it could rise further to the next resistance at 20.45. The 20.20 area is reinforced by the 100-day Simple Moving Average.

While under 20.20, some consolidation between 20.20 and 20.00 seems likely before the next directional move. A decline back to 20.00 should be seen as a normal correction after the rally from 19.80 to 20.20.

A decline under 20.00 and below the 20-day SMA should strengthen the Mexican peso, favoring an extension toward the weekly low at 19.81. The key support below is the 19.70 area that if reached, could likely trigger a rebound.

USD/MXN daily chart

-637922014430807648.png)

According to the Federal Reserve Bank of Atlanta's GDPNow model, the US economy is expected to contract by 1% in the second quarter, down from the June 27 forecast of +0.3%.

"After recent releases from the US Bureau of Economic Analysis and the US Census Bureau, the nowcasts of second-quarter real personal consumption expenditures growth and real gross private domestic investment growth decreased from 2.7% and -8.1%, respectively, to 1.7% and -13.2%, respectively, while the nowcast of the contribution of the change in real net exports to second-quarter GDP growth increased from -0.11 percentage points to 0.35 percentage points," Atlanta Fed explained in its publication.

Market reaction

The US Dollar Index showed no immediate reaction to this report and was last seen losing 0.27% on the day at 104.81.

- On a volatile session, gold reaffirms bearish bias.

- Gold falls sharply even as US yields move lower.

- XAU/USD testing $1805, below attention would turn to the YTD low at $1785.

- Gold is back below 1810$, under pressure and looking vulnerable to the downside. The price hit earlier a one-month low at $1802 and then spiked to $1825. The recovery was short-lived as gold resume the decline falling below 1810$.

XAU/USD is testing the $1805 area, and a consolidation below would expose $1800. Below that area, a test of the year-to-date low at $1786 seems likely.

On the upside, if gold manages to remain above $1820 it could alleviate the bearish pressure. A key level is seen currently at $1831, a short-term downtrend line that if broken, should open the doors to the weekly high at $1841 and to $1848 (June 22 high).

Volatile session between lower yields and risk aversion

The demand for Treasuries rose amid risk aversion. The US 10-year yield dropped to 3.00% and the 30-year fell to 3.12%, the lowest level in weeks. The decline in yields supports gold but at the same time, risk aversion is pushing commodity prices to the downside and the dollar higher.

In Wall Street, the Dow Jones is falling 0.87% and the Nasdaq 1.15%, both indexes off lows. Crude oil tumbles 2.70%.

Technical levels

- Risk-off impulse dominates the last trading day of June, boosting safe-haven peers.

- The USD/JPY falls from 137.00 below the 136.00 mark, weighted by the drop in US Treasury yields.

- The US Federal Reserve’s favorite inflation gauge, the core PCE came lower than the previous reading, signaling the effects of higher rates begin to feel.

The USD/JPY slides on Thursday, following a lower-than-expected inflation report, which could deter the US Federal Reserve from tightening at a faster pace amidst odds increasing of recession, keeping investors uneasy. At 135.85, the USD/JPY retreats from daily highs shy of 137.00, back below the 136.00 mark.

Negative sentiment and falling yields, a headwind for the USD/JPY

Risk aversion dominates the markets, as half/quarter/month-end flows bolstered the greenback. US equities remain heavy; the greenback rises shown by the US Dollar Index up by 0.04%, at 105.135, while US Treasury yields drop, led by the 10-year T-note rate at 3.00%, diving nine bps.

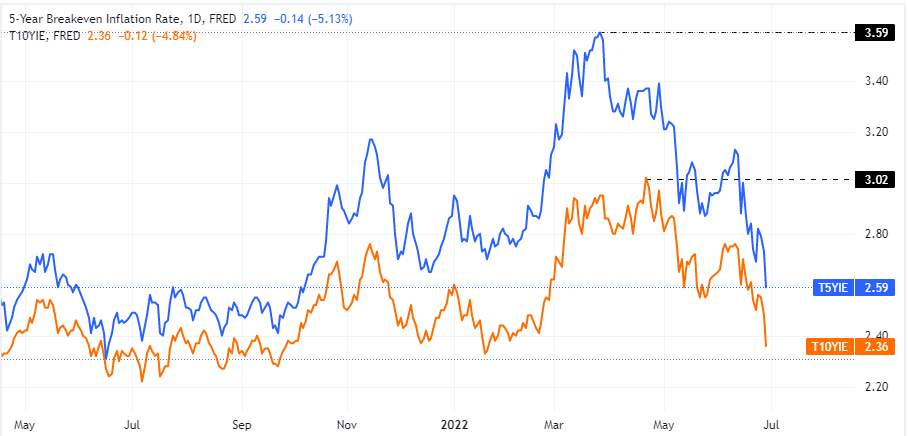

Besides that, fears of a recession as global growth stagnated, alongside high inflation, spurred a flight to safe-haven. Particularly in the USD/JPY, the yen remains bid, boosted by the fall in US Treasury yields, weighed by falling US inflation expectations, as illustrated by the five and 10-year break-even inflation rates, easing from YTD highs around 3.59% and 3.02% each, down to 2.59% and 2.36%, respectively.

Source: Tradingview/St. Louis FRED

In the meantime, US inflation, as measured by the Personal Consumption Expenditure (PCE), rose by 6.3% YoY, unchanged in May, the US Bureau of Economic Analysis reported. Meanwhile, the Fed’s favorite gauge of inflation, the core PCE, which excludes volatile items, grew 4.7%, YoY, lower than the 4.9% in April.

On the Japanese front, the docket revealed Industrial Production, which shrank faster than expected -1.3% MoM to -7.2%. Annually based, recovered some ground but stayed negatively at -2.8%, from a previous reading at -4.9%.

USD/JPY Key Technical Levels

Following its meeting on Thursday, OPEC+ announced on Thursday that it will stick to its plan of increasing oil output by 648,000 barrels per day (bpd) in August, as reported by Reuters. The group refrained from discussing the output strategy from September.

Meanwhile, Russian Deputy Prime Minister Alexander Novak said that the next meeting is planned to take place early August.

Market reaction

Crude oil prices continued to fall following this development. As of writing, the barrel of West Texas Intermediate (WTI) was trading at $105.90, losing 3.4% on a daily basis.

- Silver lost ground for the fourth straight day and dropped to a nearly two-year low on Thursday.

- Spot prices managed to find some support near the lower end of a downward sloping channel.

- The set-up still favours bearish traders and supports prospects for a further depreciating move.

Silver witnessed selling for the fourth successive day on Thursday and dived to a nearly two-year low, around the $20.30 region during the early North American session.

The downward trajectory, however, stalled near the lower boundary of a downward sloping trend channel extending from the beginning of this month. The XAG/USD did attempt a minor recovery from the said support, though lacked any follow-through beyond the $20.70-$20.75 region.

Given the recent repeated failures to find acceptance above the 200-period SMA on the 4-hour chart, the descending channel supports prospects for further losses. The negative outlook is reinforced by bearish oscillators, which are still far from being in the oversold territory.

That said, bearish traders are likely to wait for a convincing break through the trend-channel support before placing fresh bets. The XAG/USD might then turn vulnerable to weaken further below the $20.00 psychological mark and test the next relevant support near the $19.60-$19.55 area.

On the flip side, any meaningful bounce could be seen as a selling opportunity and remain capped near the $21.00 mark. The said handle should act as a key pivotal point, which if cleared decisively might trigger a short-covering rally and lift the XAG/USD towards the $21.50 supply zone.

The latter marks a confluence barrier, comprising the top end of the ascending channel and the 200-period SMA on the 4-hour chart. Sustained strength beyond would negate any near-term negative bias and pave the way for some meaningful near-term upside for the XAG/USD.

Silver 4-hour chart

-637921939354828923.png)

Key levels to watch

- USD/TRY leaves behind Wednesday’s advance and tests 16.70.

- Türkiye trade deficit widened to TL10.61B.

- Focus now shifts to Monday’s CPI release.

The Turkish lira sheds some ground and pushes USD/TRY to the area of 3-day peaks around 16.70 on Thursday.

USD/TRY appears supported near 16.00

USD/TRY extends the choppy trade so far and regains ground lost following Wednesday’s pullback, aiming once again for the upper-16.00s amidst the persistent upside momentum in the greenback as well as the increasing risk-off mood.

The lira continues to give away part of Monday’s strong gains, which saw the pair slip back to the 16.00 neighbourhood in response to the Turkish banking watchdog’s announcement to ban commercial loans denominated in lira for companies with a strong position in foreign currency (on Friday).

In the domestic calendar, the trade deficit widened to TL10.61B in May (from TL6.11B).

Next on the docket will be the release of key inflation figures for the month of June, due on July 4.

What to look for around TRY

USD/TRY keeps digesting the recent sharp decline and subsequent rebound following Friday’s announcement by the Turkish banking watchdog.

So far, price action in the Turkish currency is expected to gyrate around the performance of energy prices, the broad risk appetite trends, the Fed’s rate path and the developments from the war in Ukraine, although the effects of this new measure aimed at supporting the de-dolarization of the economy will also have its say.

Extra risks facing TRY also come from the domestic backyard, as inflation gives no signs of abating, real interest rates remain entrenched in negative figures and the political pressure to keep the CBRT biased towards low interest rates remain omnipresent.

Key events in Türkiye this week: Trade Balance (Thursday) – Manufacturing PMI (Friday).

Eminent issues on the back boiler: FX intervention by the CBRT. Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Upcoming Presidential/Parliamentary elections.

USD/TRY key levels

So far, the pair is gaining 0.67% at 16.6867 and faces the immediate target at 17.3759 (2022 high June 23) seconded by 18.2582 (all-time high December 20) and then 19.00 (round level). On the other hand, a breach of 16.0365 (monthly low June 27) would pave the way for a test of 15.6684 (low May 23) and finally 15.2373 (100-day SMA).

The money market has pared back expectations regarding the extent of European Central Bank (ECB) rate rises. Therefore, the outlook for the euro has worsened. Economists at Rabobank still expect the EUR/USD pair to test 2022’s low at the 1.1350 area.

Window of opportunity for ECB rate hikes could be narrow

“On the back of risks to gas supply over the winter, we expect the Eurozone to fall into recession in late 2022/early 2023. Not only does this suggest that the window of opportunity for ECB rate hikes could be narrow but, even more worrying for EUR bulls, this suggests the worries regarding fragmentation in Europe are likely to be enhanced.”

“We continue to see scope for a dip back to the year’s low in the EUR/USD 1.035 area on a one to three-month view.”

Economists at Danske Bank expect Brent Oil prices to ease moderately towards 2023. However, the black gold is set to remain elevated in the near-term.

Tight supply supports spot despite rising growth risks

“While looming demand slowdown points towards easing commodity prices in 2023, the limited spare capacity in global markets could support the current steep backwardation and high spot prices in the near-term.”

“We continue to forecast Brent Oil at $120/bbl in Q3, $100/bbl in Q4 and $95/bbl in 2023.”

“Potential outcome space remains very wide amid mixed drivers affecting both global demand and supply outlooks.”

Economists at TD Securities expect the GBP/USD pair to continue its downfall. Although the Bank of England (BoE) could offer some support, cable is set to break under 1.20 in the near-term.

GBP vulnerable on the crosses

“The near-term GBP trajectory is biased to the downside, even though it maintains a pretty heft discount.”

“The BoE plus fiscal support may help to put a floor in cable but not before a near-term break below 1.20. Still, BoE pricing seems too aggressive relative to our forecast, leaving GBP vulnerable on the crosses.”

The EUR/USD slide is set to continue. Economists at Scotiabank expect the pair to retest the 1.04-1.0350 support zone.

Intraday trends look soft

“The EUR has failed to break through the low 1.06 area three times since mid-month, leaving markets little technical choice but to retest the 1.04-1.0350 support zone for the EUR.”

“Intraday trends look soft, with the EUR unable to reverse any of Wednesday’s losses.”

“We spot resistance at 1.0450 and 75.”

“Support is 1.0400 and 1.0350/60.”

USD/CAD is extending Tuesday’s sharp squeeze higher from the 1.2820 area. Economists at Scotiabank note that the pair could reach the 1.30 level on a break past 1.2950.

USD gains unlikely to extend much above the 1.30 area

“Gains through the 20s target intraday strength to 1.2950 and, above here, spot would have a free run at 1.30+ again. We still see limited scope for USD gains to extend much above the 1.30 area, however.”

“Intraday support is 1.2865 and 1.2820.”

Economists at TD Securities expect another push lower in the EUR/USD targeting a level around 1.03. However, the pair is set to rebound later in the year.

Lower oil would benefit the euro

“The EUR's near-term outlook remains challenging, reflecting, in part, the sluggish backdrop for risk sentiment.”

“The wall of worry around European and global growth risks remains elevated, while China is only starting to emerge from its growth slumber.”

“Oil prices are another key factor to watch in the months ahead, where lower oil would benefit EUR.”

“We expect EUR/USD to hold the 1.03/1.07 range before pushing higher in H2.”

Gold trades with a mild negative bias for the fourth successive day on Thursday. Despite increasing recession fears, the yellow metal is set to remain under downside pressure, economists at TD Securities report.

Liquidity is being sapped from global markets

“Gold prices are under pressure despite rising recession odds, in contrast to recent price action pointing to safe-haven flows supporting the yellow metal.”

“Gold prices have disconnected altogether from market pricing for Fed hikes over the past month, and have instead grown their relationship with the USD, pointing to a smaller magnitude of idiosyncratic flows for the yellow metal.”

“Liquidity is being sapped from global markets, and gold flows have not been spared.”

The European Central Bank (ECB) will divide eurozone countries as donors, recipients and neutrals for the reinvestment of the Pandemic Emergency Purchase (PEPP) Programme proceeds, Reuters reported on Thursday, citing sources familiar with the matter.

The list of recipients will reportedly include Italy, Spain, Portugal and Greece while Germany, France and Netherlands will be among the donors.

ECB is said to review these lists monthly, focusing on the size and the speed of the bond-spread moves.

Market reaction

EUR/USD recovered modestly from two-week lows in the last hour and was last seen losing 0.22% on the day at 1.0417.

USD/CAD remains in a range. Economists at TD Securities expect the pair to continue trading within 1.27 and 1.31.

BoC rate hikes start to rattle the housing market

“USD/CAD should continue to maintain the 1.27/1.31 range in the short-term. The bias, though, remains to the upside, especially as BoC rate hikes start to rattle the housing market and risk appetite remains shaky.”

“We also downplay the importance of the oil factor given limited longer-term investment implications.”

“While the consensus view around USD/CAD seems less varied than other pairs, we're generally more bearish CAD in the months ahead.”

- Gold staged a solid recovery from the $1,800 neighbourhood or its lowest level since May 16.

- Softer US PCE inflation data led to a modest USD pullback and extended support to the metal.

- Sliding US bond yields, growing recession fears further benefitted the safe-haven commodity.

- The prospects for faster Fed rate hikes held back bulls from placing fresh bets and capped gains.

Gold witnessed a dramatic turnaround during the early European session and rallied over $20 from the vicinity of the $1,800 mark or the lowest level since May 16. The momentum pushed spot prices to a fresh daily high, around the $1,825 region, though lacked follow-through buying.

Data released from the US showed that the Core Personal Consumption Expenditures (PCE) Price Index - the Fed's preferred inflation gauge - moderated to the 4.7% YoY rate in May from the 4.9% previous. Additional detail revealed that Personal Spending growth slowed significantly in May to just 0.2% during the reported month. The softer data, along with the ongoing decline in the US Treasury bond yields, forced the US dollar to trim a part of its intraday gains and offered some support to the dollar-denominated gold.

Apart from this, concerns that rapidly rising rates and tighter financial conditions would hurt global economic growth continued weighing on investors' sentiment and further benefitted the safe-haven gold. That said, the prospects for aggressive Fed rate hikes held back traders from placing fresh bullish bets around the non-yielding metal. In fact, Fed Chair Jerome Powell said on Wednesday that the US central bank remains focused on getting inflation under control and the market pricing is pretty close to the dot plot.

Even from a technical perspective, the recent repeated failures near the very important 200-day SMA support prospects for a further near-term depreciating move. That said, the emergence of some buying near the $1,800 mark warrants some caution. Nevertheless, the bias still seems tilted in favour of bearish traders and any subsequent move up might still be seen as a selling opportunity. This makes it prudent to wait for strong follow-through buying before confirming that gold price might have formed a near-term bottom.

Technical levels to watch

- EUR/USD remains offered and breaches 1.0400.

- Next on the downside comes the June low at 1.0358.

EUR/USD keeps the leg lower well in place so far this week and now breaks below the 1.0400 support to print new 2-week lows.

The inability to leave behind the 4-month line near 1.0640 should keep the downside pressure unchanged around the pair. That said, if the selling bias gathers further impulse, then another visit to the June low at 1.0358 (June 15) could start emerging on the horizon ahead of the 2022 low at 1.0348 (May 13).

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.1112.

EUR/USD daily chart

- USD/CAD trimmed a part of its intraday gains amid modest USD pullback post-US PCE inflation data.

- The ongoing decline in crude oil prices undermined the loonie and continued lending some support.

- The backwards-looking monthly Canadian GDP report did little to provide any impetus to the major.

The USD/CAD pair quickly retreated a few pips from the weekly high post-US/Canadian macro data and was last seen trading around the 1.2900 mark during the early North American session.

The US Bureau of Economic Analysis reported that the Core Personal Consumption Expenditures (PCE) Price Index - the Fed's preferred inflation gauge - rose 0.3% MoM in May. This was slightly below the 0.4% anticipated and matched the previous month's reading. Furthermore, the yearly rate moderated in line with expectations, to 4.7% from 4.9% in April.

Additional details revealed that personal spending growth slowed notably to 0.2% in May and the previous month's reading was also revised down to 0.6% from 0.9% reported originally. The softer data, along with a further decline in the US Treasury bond yields, forced the US dollar to trim a part of its intraday gains and capped the USD/CAD pair.

The downside, however, remains cushioned amid the ongoing retracement slide in crude oil prices, which tend to undermine the commodity-linked loonie. The worsening global economic outlook, which could stall fuel demand recovery, and a rise in the US fuel stocks dragged crude oil prices further away from a one-and-half-week high touched the previous day.

This, to a larger extent, overshadowed mostly in-line monthly Canadian GDP report, showing that the economy expanded by 0.3% in April. This marked a sharp deceleration from the 0.7% growth recorded in the previous month. The backwards-looking data, however, did little to provide any meaningful impetus to the Canadian dollar or influence the USD/CAD pair.

Technical levels to watch

- Canadian economy expanded by 0.3% in April as expected.

- The USD/CAD pair retreated toward 1.2900 after this data.

Led by growth in goods-producing industries, the real Gross Domestic Product of Canada grew by 0.3% on a monthly basis in April, Statistics Canada reported on Thursday. This print followed March's expansion of 0.7% and came in line with the market expectation.

Market reaction

The USD/CAD pair, which touched a six-day high of 1.2933 earlier in the day, lost its traction after this data and was last seen posting small daily gains at 1.2906.

- Initial Jobless Claims declined by 2,000 in the week ending June 25.

- US Dollar Index clings to strong daily gains above 105.00.

There were 231,000 initial jobless claims in the week ending June 25, the weekly data published by the US Department of Labor (DOL) showed on Thursday. This print followed the previous week's print of 233,000 (revised from 229,000) and came in slightly higher than the market expectation of 228,000.

Further details of the publication revealed that the advance seasonally adjusted insured unemployment rate was 0.9% and the 4-week moving average was 231,750, an increase of 7,250 from the previous week's revised average.

"The advance number for seasonally adjusted insured unemployment during the week ending June 18 was 1,328,000, a decrease of 3,000 from the previous week's revised level," the DOL said.

Market reaction

These figures don't seem to be having a noticeable impact on the dollar's performance against its rivals. As of writing, the US Dollar Index was up 0.3% on the day at 105.40.

Inflation in the US, as measured by the Personal Consumption Expenditures (PCE) Price Index, stayed unchanged at 6.3% on a yearly basis in May, the US Bureau of Economic Analysis announced on Thursday.

The Core PCE Price Index, the Federal Reserve's preferred gauge of inflation, declined to 4.7% in the same period from 4.9% in April. This print came in line with the market expectation.

Further details of the publication revealed that Personal Income and Personal Spending rose by 0.5% and 0.2%, respectively, on a monthly basis in May.

Market reaction

The US Dollar Index edged slightly lower from session highs after this data but was last seen rising 0.2% on the day at 105.30.

- AUD/USD staged modest bounce, though struggled to find acceptance above the 0.6900 mark.

- Recession fears weighed on investors’ sentiment and undermined the perceived riskier aussie.

- The Fed’s hawkish outlook lifted the USD closer to a 20-year peak and favours bearish traders.

- Investors now look forward to the US Core PCE Inflation for May for a fresh directional impetus.

The AUD/USD pair struggled to capitalize on its modest intraday bounce from the vicinity of the monthly low and remained below the 0.6900 mark heading into the North American session.

Concerns that a more aggressive move by major central banks would pose challenges to global economic growth continued weighing on investor' sentiment. This was evident from a generally weaker tone around the equity markets, which provided a fresh lift to the safe-haven US dollar and acted as a headwind for the risk-sensitive aussie.

In fact, the USD shot closer to a two-decade high and was also underpinned by Fed Chair Jerome Powell's overnight hawkish remarks, reaffirming a faster policy tightening path. Speaking at the ECB's annual forum, Powell said that the Fed remains focused on getting inflation under control and the market pricing is pretty close to the dot plot.

Hence, the market focus will remain glued to the release of the Fed's preferred inflation gauge, the Core PCE Price Index. The data would influence the USD price dynamics and provide a fresh impetus to the AUD/USD pair. In the meantime, the USD bulls seemed rather unaffected by the ongoing decline in the US Treasury bond yields.

The fundamental backdrop supports prospects for an extension of the recent depreciating move for the AUD/USD pair, though bearish traders might wait for sustained weakness below the 0.6850 area. Spot prices might then aim to challenge the YTD low, around the 0.6830-0.6825 region touched in May, before eventually dropping to the 0.6800 mark.

Technical levels to watch

- DXY surpasses the 105.00 hurdle with certain conviction.

- The 2022 peak near 105.80 (June 15) comes next.

DXY advances for the third consecutive session and looks to consolidate the recent breakout of the 105.00 barrier on Thursday.

The index has rapidly left behind the weekly high near 105.00 (June 22) and in doing so it has opened the door to a relatively quick potential visit to the YTD highs around 105.80 (June 15).

As long as the 4-month line near 102.30 holds the downside, the near-term outlook for the index should remain constructive.

Looking at the longer run, the outlook for the dollar is seen bullish while above the 200-day SMA at 98.08.

DXY daily chart

- EUR/JPY extends the corrective downside below 142.00.

- Above 138.60, further gains in the cross are likely.

EUR/JPY drops for the third session in a row on Thursday, this time breaking below the key 142.00 support.

Despite the ongoing correction, the bullish bias in the cross remains well in place as long as the support line around 138.60 holds the downside. This area of contention is currently reinforced by the 55-day SMA.

The resumption of the upside bias could see the YTD top at 144.27 (June 28) returning to the radar ahead of the round level at 145.00 and prior to the 2015 high at 145.32 (January 2).

EUR/JPY daily chart

US PCE Price Index Overview

Thursday's US economic docket highlights the release of the Core Personal Consumption Expenditure (PCE) Price Index for May, scheduled later during the early North American session at 12:30 GMT. The Fed's preferred inflation gauge is expected to rise by 0.4% MoM during the reported month as compared to the 0.3% in April. The yearly rate, however, is anticipated to moderate to 4.7% in May from the 4.9% previous.

How Could it Affect EUR/USD?

Speaking at the ECB's forum on Wednesday, Fed Chair Jerome Powell reaffirmed a faster policy tightening path and said that the US central bank remains focused on getting inflation under control. Higher-than-expected PCE results will reinforce the Fed's hawkish policy outlook and provide a fresh lift to the US dollar. Conversely, the softer print would still be far above Fed’s official 2% target and is more likely to be overshadowed by growing recession fears. This, in turn, favours the USD bulls and suggests that the path of least resistance for the EUR/USD pair is to the downside.

Eren Sengezer, Editor at FXStreet, outlined important technical levels to trade EUR/USD: “The pair is facing immediate resistance at 1.0470 (Fibonacci 23.6% retracement of the latest downtrend). In case the pair fails to reclaim that level, it is likely to extend its slide toward 1.0400 (psychological level), 1.0380 (end-point of the latest downtrend) and 1.0360 (June 15 low).”

“On the upside, the pair could recover toward 1.0500 (psychological level) and 1.0520 (Fibonacci 38.2% retracement, 50-period SMA, 100-period SMA on the four-hour chart) if buyers managed to flip 1.0470 into support,” Eren added further.

Key Notes

• US PCE Inflation May Preview: Inflation becomes moot

• EUR/USD Forecast: Euro's recovery prospects diminish

• EUR/USD Price Analysis: Sees a downside below the crucial support of 1.0430

About the US PCE Price Index

The Personal Spending released by the Bureau of Economic Analysis, Department of Commerce is an indicator that measures the total expenditure by individuals. The level of spending can be used as an indicator of consumer optimism. It is also considered as a measure of economic growth: While Personal spending stimulates inflationary pressures, it could lead to raise interest rates. A high reading is positive (or Bullish) for the USD.

"The likelihood of gas rationing in Europe has increased significantly following the recent disruption of Russian natural gas supplies through the Nord Stream 1 pipeline," Fitch Ratings said in a report published on Thursday. "A technical recession in the eurozone is now an increasing possibility."

Market reaction

The shared currency stays under selling pressure on Thursday and the EUR/USD pair was last seen losing 0.3% on the day at 1.0408. Meanwhile, Euro Stoxx 600 Index is down more than 2%, pointing to a risk-averse market environment.

- USD/JPY witnessed some selling on Thursday and moved further away from a 24-year high.

- Recession fears, the risk-off mod benefitted the safe-haven JPY and exerted some pressure.

- Sliding US bond yields kept the USD bulls on the defensive and contributed to the selling bias.

- The Fed-BoJ policy divergence helped limit losses and supports prospects for some dip-buying.

The USD/JPY pair witnessed some selling on Thursday and snapped a four-day winning streak to its highest level since September 1998, around the 137.00 mark touched the previous day. The pair remained depressed through the first half of the European session, though showed resilience below the 136.00 mark and has now recovered a few pips from the daily low.

Investors remain concerned that rapidly rising interest rates and tighter financial conditions would pose challenges to global economic growth. This was evident from the prevalent risk-off mood and benefitted the safe-haven Japanese yen. The anti-risk flow, along with recession fears, dragged the US Treasury bond yields, which kept the US dollar bulls on the defensive and exerted downward pressure on the USD/JPY pair.

That said, the divergent policy stance adopted by the Fed and the Bank of Japan acted as a tailwind for spot prices. Speaking at the ECB's annual forum on Wednesday, Fed Chair Jerome Powell reaffirmed bets for more aggressive rate hikes and said that the US economy is well-positioned to handle tighter policy. Powell added that the Fed remains focused on getting inflation under control and the market pricing is pretty close to the dot plot.

In contrast, the BoJ has signalled that it would stick to its ultra-accommodative policy and reiterated its guidance to keep borrowing costs at "present or lower" levels. The Japanese central bank had also pledged to guide the 10-year yield to around 0% and intervene to keep rates from moving higher. This, in turn, helped limit any further losses and assisted the USD/JPY pair to rebound around 25-30 pips from the daily low.

Market participants now look forward to the US economic docket, featuring the Core PCE Price Index - the Fed's preferred inflation gauge - and the usual Weekly Initial Jobless Claims. Apart from this, the US bond yields, the USD price dynamics and the broader risk sentiment should provide some impetus to the USD/JPY pair. Nevertheless, the fundamental backdrop still seems tilted firmly in favour of bullish traders.

Technical levels to watch

- EUR/USD looks stuck in the 1.0430 region.

- Germany labour market report surprised to the downside.

- EMU jobless rate ticked lower to 6.6% in May.

The single currency remains under pressure and motivates EUR/USD to navigate in the lower end of the range around 1.0430 on Thursday.

EUR/USD looks to data, risk trends

EUR/USD remains offered and extend the leg lower after being rejected from the 1.0615 region earlier in the week. The corrective downside in the pair comes in response to the resurgence of the risk aversion sentiment and the resumption of the buying bias in the greenback.

In addition, the decline in the German 10y Bund yields - now approaching the 1.40% zone – also collaborates with the sour mood around the European currency on Thursday.

Further selling hurt the euro after the inaction seen in Chair Lagarde in recent comments, as she only reiterated the bank’s intention to raise rates by 25 bps next month, while further rate hikes would hinge on the progress of domestic fundamentals.

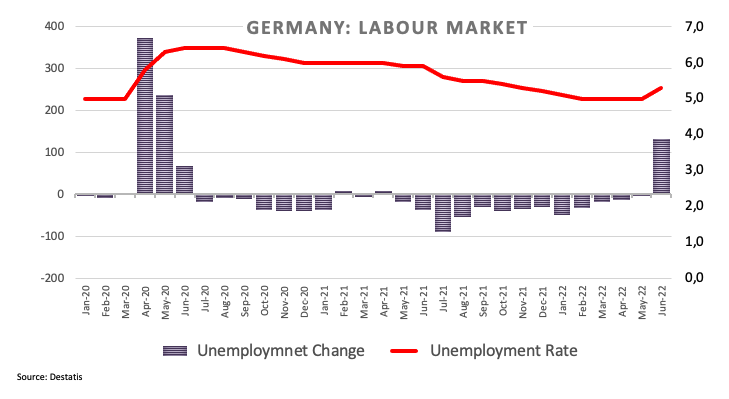

Earlier in Germany, Retail Sales contracted 3.6% in the year to May, the Unemployment Rate ticked higher to 5.3% and the Unemployment Change increased by 133K persons, both prints for the month of June.

Across the ocean, the publication of inflation figures measured by the PCE will take centre stage seconded by usual Initial Claims and Personal Income/spending.

What to look for around EUR