- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- AUD/USD pares the previous day’s losses as RBA Governor Lowe sounds hawkish.

- RBA’s Lowe shows readiness to do “What is necessary” to tame inflation in next few years.

- Mixed sentiment, US Dollar’s retreat adds strength to the recovery moves ahead of the key Aussie data/events.

- Australia monthly inflation, China official PMIs, US employment clues and US Senate voting on debt ceiling deal eyed.

AUD/USD picks up bids to pare the previous day’s losses around 0.6520, after snapping a two-day uptrend, as Reserve Bank of Australia (RBA) Governor Philip Lowe sounds hawkish on early Wednesday in Asia.

That said, RBA Governor Lowe said, “(He) will do what is necessary to make sure inflation comes back to target range in next few years.”

Also read: RBA’s Lowe: Nominal wage growth has not been source of inflation

Apart from hawkish testimony from RBA’s Lowe, the market’s consolidation ahead of the top-tier data from Australia and China, as well as the US, joins the preparations for the US Senate’s voting on the debt ceiling agreement to favor the AUD/USD rebound.

It should be noted that the US Dollar’s struggle ahead of the key data/events also exerts downside pressure on the AUD/USD price despite the latest corrective bounce off the weekly low. That said, the greenback’s latest weakness could be linked to the market’s fears that the US policymakers will turn down the agreement to tame the US default in Congress despite looming system failure on June 05. Adding strength to the DXY’s retreat is the mixed US data and month-end positioning. With this, the US Dollar Index (DXY) rose to the highest levels since mid-March on Tuesday before snapping a five-day uptrend, as well as positing the biggest daily loss since April 19, while closing the North American trading session around 104.05.

It’s worth observing that the US Conference Board's (CB) Consumer Confidence Index edged lower to 102.30 for May from an upwardly revised 103.70 prior marked in April (from 101.30). Additional details of the survey report mentioned that the one-year consumer inflation expectations ticked down to 6.1% in May from 6.2% in April. Further, the Dallas Fed Manufacturing Business Index for May dropped to -29.1 from -23.4 and versus -19.6 market expectations.

Despite the mixed data, Richmond Fed President Thomas Barkin said that he is seeing evidence that interest rate hikes are curbing demand, which in turn prods the AUD/USD buyers ahead of an important day.

Elsewhere, US Republicans like Chip Roy and Ralph Norman showed readiness to turn down the US debt ceiling agreement but softer US data put a floor under the risk-off mood.

Against this backdrop, Wall Street closed mixed but the US Treasury bond yields remained pressured.

Looking ahead, Australia’s Monthly Consumer Price Index (CPI) for May and China's NBS Manufacturing PMI, as well as Non-Manufacturing PMI, will be the key to watching for clear AUD/USD directions. That said, a positive outcome of the Senate’s voting on the measures to avoid US default, which is very much likely, can keep the greenback buyers in the driver’s seat. Also, the US JOLTS Job Openings for April are likely to ease and hence a positive surprise from the same may strengthen the hawkish Fed bets and can recall US Dollar bulls. It’s worth noting, however, that any clear negatives from the US Congress won’t be taken lightly.

Technical analysis

AUD/USD rebound remains elusive unless crossing a three-week-old descending resistance line, around 0.6560 by the press time.

- EUR/GBP is expected to surpass the immediate resistance of 0.8650 confidently ahead of Eurozone inflation.

- ECB Šimkus expects a 25 basis points (bps) rate hike in June and July to tame sticky inflation.

- More interest rate hikes are anticipated from the BoE as UK’s inflation has yet not shown promising signs of deceleration.

The EUR/GBP pair is aiming to extend its recovery from 0.8630 above the immediate resistance of 0.8650 in the early Tokyo session. The cross is getting strength ahead of the release of the preliminary Eurozone Harmonized Index of Consumer Prices (HICP) data (May), which will release on Thursday.

As per the preliminary report, core monthly HICP is seen expanding by 0.8% at a slower pace than the 1% recorded for April. Annual core HICP is expected to soften marginally to 5.5% vs. the prior release of 5.6%. The headline HICP is seen decelerating sharply to 6.3% against the former release of 7.0%.

Eurozone’s inflation has remained extremely stubborn in the past few months one month of softening would be insufficient for pausing the European Central Bank (ECB) from further policy-tightening. ECB Governing Council Gediminas Šimkus said on Tuesday that he expects a 25 basis points (bps) rate hike in June and July. This indicates that ECB’s interest rate would at least peak around 4.25%.

Apart from Thursday’s Eurozone inflation data, the speech from ECB President Christine Lagarde will be keenly watched. ECB Lagarde is expected to provide interest rate guidance for June’s monetary policy meeting.

Meanwhile, inflationary pressures in the United Kingdom economy are showing no meaningful signs of easing. On Tuesday, British Retail Consortium (BRC) reported a historic jump in shop price inflation to 9.0% since the formation of the agency in 2005. The food price inflation slowed marginally to 19.1% from the prior figure of 19.2% led by lower energy and commodity cost.

UK’s inflation has yet not shown promising signs of deceleration, therefore, more interest rate hikes are anticipated from the Bank of England (BoE) ahead. BoE Governor Andrew Bailey is expected to announce two more quarter-to-a-point interest rate hikes in the next three meetings as forecasted by Nomura.

- US Dollar Index lacks clear direction after reversing from 11-week high.

- Mixed US data, positioning for key catalysts allowed DXY bulls to retreat.

- US Senate voting on debt ceiling deal, employment clues eyed for clear directions.

US Dollar Index (DXY) renews intraday low near 104.00 while keeping the previous day’s pullback from a multi-day top amid early Wednesday. In doing so, the greenback’s gauge versus six major currencies drop for the second consecutive day after reversing from the highest levels since mid-May, as well as snapping the five-day uptrend on Tuesday.

The greenback’s latest weakness could be linked to the market’s fears that the US policymakers will stop the US debt ceiling deal in the Congress despite looming default. Adding strength to the DXY’s retreat are the mixed US data and month-end positioning.

Talking about the data, the US Conference Board's (CB) Consumer Confidence Index edged lower to 102.30 for May from an upwardly revised 103.70 prior marked in April (from 101.30). Additional details of the survey report mentioned that the one-year consumer inflation expectations ticked down to 6.1% in May from 6.2% in April. Further, the Dallas Fed Manufacturing Business Index for May dropped further to -29.1 from -23.4 and versus -19.6 market expectations.

It should be noted, however, that Richmond Fed President Thomas Barkin said that he is seeing evidence that interest rate hikes are curbing demand.

Elsewhere, US Republicans like Chip Roy and Ralph Norman showed readiness to turn down the US debt ceiling agreement but softer US data put a floor under the risk-off mood.

Against this backdrop, Wall Street closed mixed but the US Treasury bond yields remained pressured.

Although the DXY is likely to remain pressured ahead of the key data/events, a positive outcome of the Senate’s voting on the measures to avoid US default, which is very much likely, can keep the greenback buyers in the driver’s seat. Also, the US JOLTS Job Openings for April is likely to ease and hence a positive surprise from the same may strengthen the hawkish Fed bets and can recall US Dollar bulls. It’s worth noting, however, that any clear negatives from the US Congress won’t be taken lightly.

Technical analysis

Although the overbought RSI and a downside break of a two-week-old ascending trend line’s break keeps the US Dollar Index bears hopeful, the 200-day Exponential Moving Average (EMA), currently around 103.85, limits the DXY’s immediate downside.

- AUD/JPY retreats from its weekly high of 92.01 and trades lower as the Asian session opens.

- The AUD/JPY break below the Ichimoku Tenkan-Sen at 91.55 cleared the path toward 91.00.

- For a bullish continuation, the AUD/JPY must claim 91.55; otherwise, a fall below 91.10/90.85 will expose 90.00.

AUD/JPY retraces from weekly highs of 92.01, drops for two straight days, on sentiment deterioration sponsored by US debt-ceiling woes, as traders brace for the release of the Australian Consumer Price Index (CPI). As the Asian session begins, the AUD/JPY is trading at 91.06, down 0.04%.

AUD/JPY Price Analysis: Technical outlook

From a daily chart perspective, the AUD/JPY is neutral to downward biased after falling below the Ichimoku Tenkan-Sen pierced at 91.55, exacerbating the fall toward the 91.00 figure. A one-month-old upslope support trendline was also broken, suggesting sellers are stepping in.

Even though the AUD/JPY is tilted downwards, a seven-month-old previous resistance trendline turned support, suggesting congestion around the 90.85/91.10 area. If AUD/JPY breaks below that area, the next support would be the Kijun-Sen line at 90.15, ahead of testing a support trendline has passed at around the 90.00 figure. Once cleared, the next support would be the top of the Ichimoku Cloud at 89.55.

Contrarily, the AUD/JPY must claim the Tenkan Sen line at 91.55 for a bullish continuation, triggering a rally toward the 92.00 figure. A breach of the latter will expose the year-to-date (YTD) high at 92.99.

AUD/JPY Price Action – Daily chart

“Nominal wage growth has not been source of inflation”, said Reserve Bank of Australia (RBA) Governor Philip Lowe while giving testimony before the Senate Economics Legislation Committee, in Canberra.

Key comments

We're in data dependent mode.

Not a single variable that drives our decisions.

Reasons for weak productivity growth complex.

Serious about inflation target, want to preserve gains in labor market.

Inflation expectations well anchored, cannot take for granted.

Entrenched inflation would lead to higher interest rates and unemployment.

Will do what is necessary to make sure inflation comes back to target range in next few years.

Market reaction

AUD/USD ticks up to 0.6520 in an immediate reaction to the statements from RBA’s Lowe. However, the Aussie pair stays defensive as it braces for a busy day ahead.

Also read: AUD/USD retreats amidst market uncertainty, US debt ceiling disputes ahead of Aussie CPI

- USD/CHF is looking to recapture the immediate resistance of 0.9080 despite the subdued USD Index.

- The Swiss Franc bulls witnessed immense selling pressure on Tuesday despite the release of upbeat Q1 GDP.

- USD/CHF is demonstrating a consolidation phase after delivering a breakout of the Wyckoff Accumulation pattern.

The USD/CHF pair has turned sideways around 0.9060 in the early Asian session after a V-shape recovery. The Swiss Franc asset is expected to recapture the crucial resistance of 0.9080 despite a subdued performance by the US Dollar Index (DXY).

Strength in the USD/CHF pair despite the sluggish USD index indicates that the Swiss Franc bulls are also weak. The Swiss Franc bulls witnessed immense selling pressure on Tuesday despite the release of upbeat Q1 Gross Domestic Product (GDP) data. Annual GDP matched expectations at 0.6% while quarterly GDP expanded by 0.3% while the street was anticipating an expansion of 0.1%.

Sheer volatility is anticipated from the US Dollar ahead of the release of the United States Automatic Data Processing (ADP) Employment data will be keenly watched. As per the consensus, the US economy added 170K jobs in May, lower than the prior addition of 296K. Later on Friday, US Nonfarm Payrolls (NFP) will release, which will provide comprehensive information about the US labor market.

USD/CHF is demonstrating a consolidation phase after delivering a breakout of the Wyckoff Accumulation pattern formed on a four-hour scale. Broadly, the Swiss franc asset is expected to display wider bullish ticks and heavy volume as bulls remain solid in the markup phase.

Currently, Relative Strength Index (RSI) (14) is oscillating in the 40.00-60.00 range, which indicates a lackluster performance. A confident break into the bullish range of 60.00-80.00 would strengthen US Dollar bulls.

Going forward, a decisive break above the immediate resistance plotted on May 30 high at 0.9084 will drive the asset toward March 28 low at 0.9137 followed by the round-level resistance of 0.9200.

In an alternate scenario, a downside move below May 16 low at 0.8929 will drag the asset toward April 14 low at 0.8867. A slippage below April 14 low will further drag the asset toward the Spring formation around May 04 low at 0.8820.

USD/CHF four-hour chart

-638210846382261541.png)

- WTI crude oil remains pressured at the lowest levels in three weeks after falling the most in a month.

- Downside break of bullish chart pattern, bearish MACD signals favor Oil sellers.

- Oversold RSI may prod WTI bears before directing them to monthly/yearly low.

- Buyers need validation from $76.85 to retake control.

WTI crude oil price holds lower grounds near $69.60 as bears take a breather during early Wednesday morning in Asia, after a heavy fall.

That said, the black gold dropped the most since May 02 on Tuesday to drag the quote towards the lowest levels in three weeks. With this, the energy benchmark broke an upward-sloping trend channel established since May 08, as well as extended the trading below the 200-SMA.

While the bullish channel rejection and sustained trading below the key SMA favor Oil price sellers, the MACD signals are also suggesting the commodity’s further downside. However, the RSI (14) is oversold and hence the quote needs to consolidate a bit before portraying the fresh fall.

With this, the $67.30-20 support area gains attention before the WTI bears can approach the monthly, as well as the yearly, low marked on May 03 around $64.30.

Meanwhile, the stated channel’s bottom line, close to $71.70 precedes the 200-SMA hurdle of around $73.93 to guard immediate recovery of the Oil price.

Following that, the aforementioned channel’s top line near $75.00 and the April 28 peak of around $76.85 may challenge the WTI bulls before giving them control.

WTI crude oil: Four-hour chart

-31052023-638210841469691070.png)

Trend: Further downside expected

- USD/CAD fades bounce off one-week low after snapping two-day downtrend, sidelined of late.

- WTI crude oil dropped the most in four weeks amid mixed sentiment.

- Mixed US data, month-end consolidation and cautious mood before US Senate’s voting on debt ceiling deal prod US Dollar bulls.

- Canada Q1 GDP, US employment and activity clues should be eyed on calendar.

USD/CAD retreats to 1.3600 during early Wednesday’s Asian session, fading the previous day’s rebound from 1.3567 and easing from 1.3613, as it braces for the key growth numbers from Canada. Also challenging the Loonie pair could be the anxiety ahead of the US Senate voting on the debt ceiling deal. However, a slump in the WTI crude oil price weighs on the quote.

The month-end consolidation and cautious mood ahead of the top-tier data/events gain major attention. Also challenging the greenback could be the mixed US data. With this, US Dollar Index (DXY) rose to the highest levels since mid-March on Tuesday before snapping a five-day uptrend, as well as positing the biggest daily loss since April 19, while closing the North American trading session around 104.05.

On the other hand, WTI crude oil dropped to the lowest levels in four weeks, falling more than 4.0% to print the biggest daily loss since May 02 as it bears the burden of economic fears emanating from uncertainty about the US policymakers’ ability to avoid the looming default. Apart from that, hopes of more Oil output and the US push for using the Strategic Petroleum Reserve (SPR) also exert downside pressure on the black gold price.

On Tuesday, the US Conference Board's (CB) Consumer Confidence Index edged lower to 102.30 for May from an upwardly revised 103.70 prior marked in April (from 101.30). Additional details of the survey report mentioned that the one-year consumer inflation expectations ticked down to 6.1% in May from 6.2% in April. Further, US House Price Index rose 0.6% MoM versus 0.2% expected and 0.7% prior (revised from 0.5%) whereas the S&P/Case-Shiller Home Price Indices dropped to -1.1% YoY in March versus 0.4% prior and -1.6% anticipated. Additionally, the Dallas Fed Manufacturing Business Index for May dropped further to -29.1 from -23.4 and versus -19.6 market expectations.

It should be noted that an improvement in Canada’s Current Account deficit for the first quarter (Q1), to -6.17B versus -9.35B expected and -8.05B prior (revised) also exerts downside pressure on the Loonie pair.

While portraying the mood, Wall Street closed mixed but the US Treasury bond yields remained pressured as US Republicans like Chip Roy and Ralph Norman showed readiness to turn down the US debt ceiling agreement but softer US data put a floor under the risk-off mood. Elsewhere Richmond Fed President Thomas Barkin said that he is seeing evidence that interest rate hikes are curbing demand.

Looking ahead, the US JOLTS Job Openings for April and Canada's Gross Domestic Product (GDP) for Q1 will be crucial for the Loonie pair to watch for clear directions, apart from the risk catalysts mentioned above. Should the Canadian growth number surpasses the downbeat expectations, the Loonie pair may witness fresh downside pressure.

Technical analysis

USD/CAD grinds between a two-month-old descending resistance line and an upward-sloping support line from May 08, respectively near 1.3640 and 1.3570, as oscillators suggest that bulls run out of steam.

- Despite Japanese Authorities’ intervention in the FX markets, the EUR/JPY pair maintains the 150.00 mark.

- Although the EUR/JPY is upward biased, downside risks remain, with sellers eyeing the Kijun-Sen line at 148.87.

- The RSI and the Rate of Change are mixed, warranting caution, despite the EUR/JPY bullish bias.

EUR/JPY advances as the Wednesday Asian session begins after printing two consecutive days of losses, which witnessed the EUR/JPY pair falling from around the 151.00 figure toward the low 150.00s. Factors like a risk-off impulse, and Japanese Authorities’ vocal intervention in the Forex Markets, boosted the Japanese Yen (JPY). At the time of writing, the EUR/JPY exchanges hand at 150.04, almost flat.

EUR/JPY Price Analysis: Technical outlook

The cross-currency pair remains upward biased even though it dipped to the Ichimoku Tenkan-Sen at 149.89, but buyers staying around the area lifted the EUR/JPY to the 150.00 figure. Nevertheless, there’s some weakness on the pair, with two consecutive bearish sessions, suggesting that sellers are moving into the pair, trying to send the EUR/JPY towards the Kijun-Sen line at 148.87, which would exacerbate a drop towards the April 26 daily high of 147.91.

Conversely, the EUR/JPY first resistance would be the peak of the Chikou Span at 150.76, followed by the May 29 daily high at 151.07. A breach of the latter will expose the year-to-date (YTD) high at 151.61.

From an oscillator perspective, the Relative Strength Index (RSI) indicator is still bullish, while the 3-day Rate of Change (RoC) shifted bearishly.

Even though the EUR/JPY is bullishly biased, caution is warranted.

EUR/JPY Price Action – Daily chart

- GBP/USD has climbed back above 1.2400 as the USD Index has resumed its downside journey.

- Speaker McCarthy urged Republican members to support a bipartisan deal to lift the $31.4 trillion U.S. debt ceiling.

- Signs of persistence in the UK’s inflation are solidifying the need for more interest rate hikes from the BoE.

The GBP/USD pair has rebounded above the round-level resistance of 1.2400 after a steep correction in the early Tokyo session. The Cable has climbed back above 1.2400 as the US Dollar Index (DXY) has retreated from 104.20.

S&P500 futures are showing minor losses in early Asia after a choppy Tuesday, portraying a caution in the overall market mood. US equities remained flat on Tuesday despite opening after an extended weekend.

Fears of a default by the United States economy have not waned entirely as the US debt-ceiling raise deal is yet to pass in Congress. Late Tuesday, House of Representatives Kevin McCarthy urged Republican members to support a bipartisan deal to lift the $31.4 trillion U.S. debt ceiling, calling it the most conservative deal we ever had.

The USD Index is expected to remain sideways after retreating from 104.20 as investors are shifting their focus toward the United States Employment data. But before that, US JOLTS Job Openings data (April) will be keenly watched. According to the estimates, total job openings have dropped to 9.375M vs. the former release of 9.59M.

Apart from that, Federal Reserve’s (Fed) Beige Book will be in focus which will provide economy-wise inflation and growth numbers.

On the Pound Sterling front, signs of persistence in the United Kingdom’s inflation are solidifying the need for more interest rate hikes from the Bank of England. Official food inflation softened marginally to 19.1% from the prior figure of 19.2% led by lower energy and commodity cost but is insufficient to force BoE Governor Andrew Bailey to remain neutral ahead.

Economists at Nomura cited “Following the latest inflation print, we have changed our call and now see the BoE raising rates by 25 bps at each of the next three meetings.” They further added “We thus forecast peak rates at 5.25% for the BoE.

- EUR/USD grinds higher after bouncing off 10-week low.

- US Dollar traces yields to retreat from multi-day peak amid uncertainty for US debt ceiling deal in Congress.

- US data came in mixed, month-end positioning join anxiety ahead of key events to recall Euro buyers.

- Germany’s HICP, US JOLTS Job Openings and Fedspeak will decorate calendar, Senate will vote on measures to avoid US default.

EUR/USD struggles to extend the latest recovery from the lowest levels since March, grinding near 1.0735-30 amid early Wednesday morning in Asia, after snapping a five-day downtrend. That said, the Euro pair cheered the US Dollar’s pullback from the multi-day high the previous day but depicts the market’s cautious mood ahead of the top-tier data/events scheduled for publishing today.

US Dollar Index (DXY) rose to the highest levels since mid-March on Tuesday before snapping a five-day uptrend, as well as positing the biggest daily loss since April 19, while closing the North American trading session around 104.05.

While tracing the US Dollar’s latest retreat, the month-end consolidation and cautious mood ahead of the top-tier data/events gain major attention. Also challenging the greenback could be the mixed US data.

That said, the US Conference Board's (CB) Consumer Confidence Index edged lower to 102.30 for May from an upwardly revised 103.70 prior marked in April (from 101.30). Additional details of the survey report mentioned that the one-year consumer inflation expectations ticked down to 6.1% in May from 6.2% in April. Further, US House Price Index rose 0.6% MoM versus 0.2% expected and 0.7% prior (revised from 0.5%) whereas the S&P/Case-Shiller Home Price Indices dropped to -1.1% YoY in March versus 0.4% prior and -1.6% anticipated. Additionally, the Dallas Fed Manufacturing Business Index for May dropped further to -29.1 from -23.4 and versus -19.6 market expectations.

Following the data, Richmond Fed President Thomas Barkin said that he is seeing evidence that interest rate hikes are curbing demand.

Elsewhere, Republican representative Chip Roy said McCarthy should pull the debt ceiling bill, per Reuters, which in turn raises challenges for the US debt ceiling deal as it heads to the Republican-controlled Senate for voting.

On the other hand, Spain marked downbeat inflation numbers for May and hence raised expectations of softer prints of today’s German inflation figures, as well as highlighting a lesser need for the European Central Bank (ECB) to push for higher rates. Even so, ECB Governing Council Gediminas Šimkus said on Tuesday that he expects a 25 basis points (bps) rate hike in June and July.

Amid these plays, Wall Street closed mixed but the US Treasury bond yields remained pressured.

Looking ahead, Germany’s inflation gauge, namely the Harmonized Index of Consumer Prices for May, will precede the US JOLTS Job Openings for April and China Purchasing Managers Index for May to watch on the calendar for clear directions. However, major attention should be given to the voting on the US debt ceiling agreement in the Senate.

Technical analysis

A daily closing beyond the monthly descending resistance line, now immediate support near 1.0700, directs EUR/USD bulls toward the 100-DMA hurdle of around 1.0815.

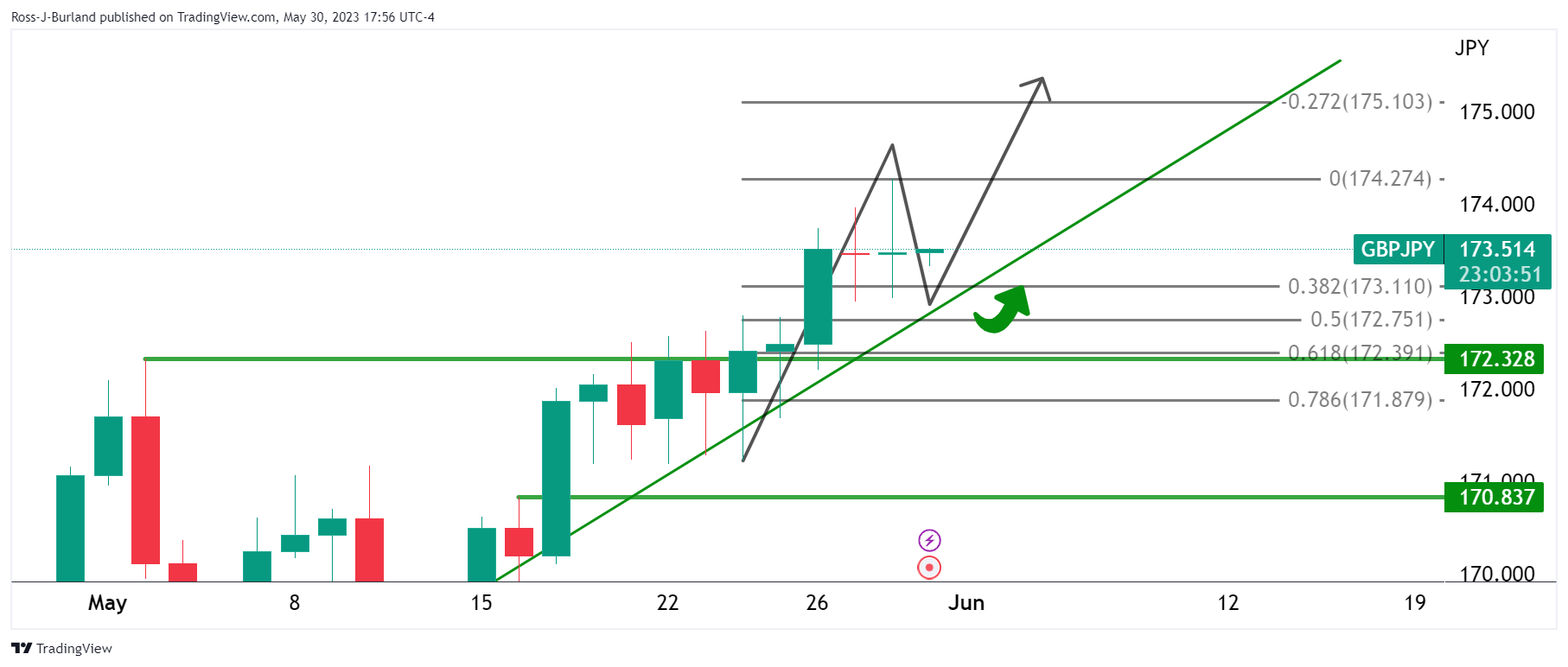

- GBP/JPY bulls need to commit to trendline support.

- Bears will be in the market on a break of 173.00.

GBP/JPY is testing fresh bull cycle highs near 174.00 but this may be the highs. We are completing the initial balance for the week and there is length in the market that could attract the bears. The following will illustrate both sides of the story.

GBP/JPY daily charts

The price is bullish above trendline support and could move higher but could just as easily head lower on a break of the trendline support.

GBP/JPY H4 chart

GBP/JPY is on the front side of the trend but the price could break the support structure and thus flip the focus on the backside.

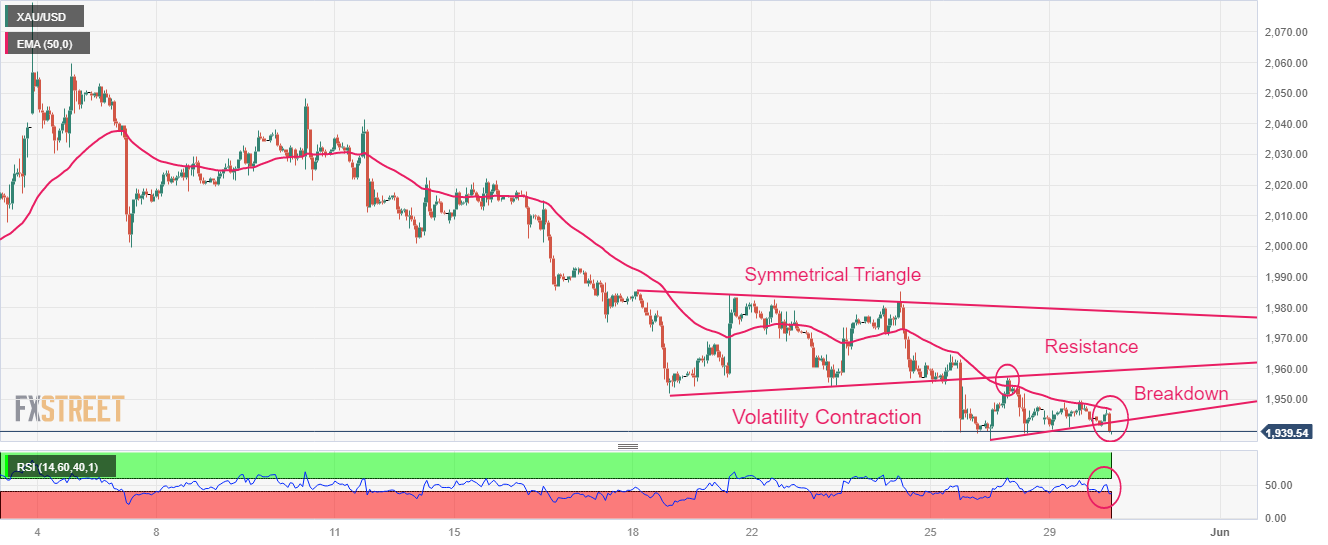

- Gold price is consolidating around $1,960.00 after a vertical rally ahead of US Employment.

- The USD Index witnessed intense selling pressure after printing a fresh 10-week high at 104.50.

- Gold price is gathering strength for a breakout above the trendline plotted from $1,952.00.

Gold price (XAU/USD) has turned sideways around $1,960.00 after failing to extend a rally above $1,963.70 in the early Asian session. A quick rally in the Gold price came after a vertical sell-off in the US Dollar Index (DXY). The USD Index witnessed intense selling pressure after printing a fresh 10-week high at 104.50.

S&P500 ended flat on Tuesday despite after an extended weekend, portraying a cautious market mood. Sheer volatility in the US equities cannot be ruled out ahead of the United States Employment data, which will build a base for June‘s monetary policy meeting by the Federal Reserve (Fed).

Despite a sell-off in the USD Index, investors are confident that the asset could be rerated ahead as one more interest rate hike by the Fed is yet to be discounted. Consumer spending has rebounded dramatically in April and now decent caliber in labor market conditions could force Fed chair Jerome Powell to look for raising interest rates further without any doubt.

On Thursday, US Automatic Data Processing (ADP) Employment data will be keenly watched. As per the consensus, the US economy added 170K jobs in May, lower than the prior addition of 296K. Later on Friday, US Nonfarm Payrolls (NFP) will release, which will provide comprehensive information about the US labor market.

Gold technical analysis

Gold price showed a V-shape recovery after dropping to near $1,932.12 on an hourly scale. The asset is gathering strength for a breakout above the trendline plotted from May 18 low around $1,952.00, which acted as a resistance for the Gold price earlier. Meanwhile, the horizontal resistance is plotted from May 19 high at $1,984.25.

Upward sloping 20-period Exponential Moving Average (EMA) at $1,954.50 indicates that the short-term trend has turned positive.

The Relative Strength Index (RSI) (14) has shifted into the bullish range of 60.00-80.00, which indicates that the upside momentum is active.

Gold hourly chart

- The AUD/USD ends with substantial losses, nearing YTD lows, weighed by disputes amongst Republicans.

- Political discussions surrounding the US debt ceiling and potential leadership change add a sour note to market sentiment.

- Investors are eyeing upcoming inflation data, Private Sector, and Housing Credit from Australia and the Chicago PMI and JOLTs report from the US for further market direction.

AUD/USD is set to finish Tuesday’s session with substantial losses, snapping two days of gains spurred by mixed market sentiment. Factors like Republicans opposing the US debt-ceiling agreement, alongside falling US Treasury bond yields, cushioned the AUD/USD’s fall. However, the AUD/USD is still hovering around the year-to-date (YTD) lows of 0.6510s.

AUD/USD heads towards 0.6510, despite higher-than-expected US Housing Prices despite

US equities finished the session mixed, as debt-ceiling discussions continued amongst Republicans looking to oust Kevin McCarthy as House Speaker. That, alongside falling US bond yields, turned market sentiment sour, weighing on Wall Street and US Treasury bond yields.

Talking about data, the US economic agenda revealed housing prices that advanced more than estimates but were ignored by market participants. Later, the US Conference Board (CB) showed that Consumer Confidence in May slowed to 102.3, above calculations but below April’s 103.7. “Consumer confidence declined in May as consumers’ view of current conditions became somewhat less upbeat while their expectations remained gloomy,” said Ataman Ozyildirim, Senior Director, Economics at The Conference Board.

In the meantime, the Dallas Fed reported that manufacturing activity in their area plunged to -29.1, beneath the prior’s month -23.4 drop, suggesting an ongoing deterioration in the Dallas Fed regional area.

On Wednesday, the Australian economic docket will feature inflation data, Private Sector, and Housing Credit, which could shed some light on the status of households. The Chicago PMI and the JOLTs report will update the economy’s position in the US.

AUD/USD Technical Levels

A busy calendar lies ahead, with a focus on Australia, with inflation data and RBA Governor Lowe's testimony. Japan will report industrial production and retail trade data. Chinese PMIs and the New Zealand ANZ May Activity Outlook are also due. Later in Europe, attention will turn to French and German inflation data. The debt ceiling drama remains unresolved, and Wednesday is supposed to be the day of the Congressional vote.

Here is what you need to know on Wednesday, May 31:

The debt ceiling deal struck between US President Biden and House Speaker Kevin McCarthy is facing hurdles and weighing on market sentiment. US stocks finished mixed, and Treasury yields dropped sharply.

The US dollar posted mixed results, affected by lower yields while at the same time, commodity and emerging market currencies were affected by risk aversion. Consumer confidence in the US dropped in May but less than expected. The focus on Wednesday will be on the debt ceiling, and then, if Congress delivers, attention will turn to employment data. Many Federal Reserve officials, including Harker and Bowman, are scheduled for public appearances on Wednesday, and the central bank will publish the Beige Book.

Analysts at Wells Fargo wrote:

Consumer confidence slipped slightly in May, and while the weakening may reflect short-term worries about the debt ceiling, the more interesting developments reveal how the sand is shifting under consumers' feet. Worries about the labor market are growing as buying plans dry up.

EUR/USD finished higher above 1.0700 after hitting a fresh monthly low at 1.0670. Spain released lower-than-expected inflation numbers. Germany and France will release inflation data on Wednesday. Another decline in annual rates could soften European Central Bank tightening expectations.

GBP/USD climbed from under 1.2350 to 1.2440 amid expectations of more tightening from the Bank of England (BoE). The EUR/GBP tumbled to 0.8628, the lowest level since mid-December.

The yen outperformed after the announcement of an emergency meeting between the Ministry of Finance, the Bank of Japan, and Financial Services Agency; also favored by the decline in government bond yields. USD/JPY dropped below 140.00 and holds a bearish bias.

USD/CHF hit two-month highs at 0.9082 and then pulled back modestly. Switzerland reported 0.6% Q1 growth, but the KOF Leading Indicators plummeted from 96.1 to 90.2 in May. Retail sales data is due on Wednesday.

AUD/USD failed to break above 0.6550 and pulled back towards 0.6500. The Aussie remains under pressure ahead of a busy Asian session, with Reserve Bank of Australia (RBA) Governor Lowe appearing before a Senate Committee and monthly inflation data. Next week is the monetary policy meeting.

USD/CAD moved sideways around 1.3600, despite the decline in crude oil prices. The WTI barrel lost more than 4%, falling below $70.00. Canada will report March growth numbers.

NZD/USD dropped marginally on Tuesday, posting the lowest daily close since November but remaining above 0.6000. The ANZ Activity Outlook and Business Confidence are due on Wednesday.

It was a positive day for Gold which finished higher after hitting fresh monthly lows. XAU/USD settled near $1,960, offering signs of stabilization. Silver retook $23.00. Cryptocurrencies rose, with BTC/USD gaining 0.45% to $27,800, and Ethereum gaining 0.60% to $1,905.

The Turkish Lira fell sharply again following the victory of Erdogan in the presidential runoff. USD/TRY climbed almost 2%, reaching a new record high at 20.40.

Like this article? Help us with some feedback by answering this survey:

- NZD/USD bears are lurking below the trendline resistance.

- Bulls eye a move into the Fibonacci scale.

NZD/USD stayed within a tight range of between 0.6025 and 0.6066 and was marginally lower ahead of the Asian open and roll over. There was a pick-up in volatility and the US Dollar was under pressure for the most part of the day.

There were concerns as to whether Congress will pass the Biden/McCarthy US debt ceiling deal. The gatekeeper House of Representatives Rules Committee is due to consider the 99-page bill beginning at 3 p.m. EDT (1900 GMT) on Tuesday, ahead of votes in the Republican-controlled House of Representatives and the Democratic-controlled Senate.

´´Although it is logical that resolving the deal will clear the way for the Federal Reserve to hike (which we think is needed, given recent US data), the fact that we have seen US bond yields fall suggests that markets are less ebullient,´´ analñysts at ANZ Bank explained.

´´Carry remains a focus for the Kiwi but carry “works” best when volatility is low and there isn’t much else going on, so it could be a patience game for carry traders. The NZ data is light until Gross Domestic Product in mid-June, and we may have to wait until then for NZ-specific factors to become drivers,´´ the analysts added.

NZD/USD technical analysis

The bears are in the market and this leaves in-the-money shorts vulnerable to a pullback. A move to test resistances could open risk to the trendline resistance in a significant correction as measured by the Fibonacci scale.

- Silver is meeting key support on the daily chart.

- Beazrs need a break of structure while bulls need to get above trendline resistance.

The price of Silver has run into a key area of daily support that leaves the bias bullish for the near term. The following illustrates this along with the market structure and various scenarios for the foreseeable future.,

XAG/USD daily charts

Silver is on the front side of the bearish trend but the price has run into a potential demand area that could see the bears throwing in the towel.

The above scenario, however, shows a bearish bias with the trendline resistance playing its role in the sell-off below the market structure.

On the other hand, the market has rallied hard into the bearish impulse and is taking out the 50% mean reversion level. A break of the trendline resistance leaves the bullish bias intact. However, that is not to say that the bears will not attempt to sell at a premium which could see the price restest recent lows as its forms structure in a stage of accumulation.

- USD/MXN pair trades higher, fueled by risk-off sentiment and declining US bond yields.

- The Conference Board reports a decline in Consumer Confidence in May, reflecting a gloomy outlook among consumers, while housing prices rise above expectations.

- Richmond Fed President Barkin warns of stubborn inflation and mixed economic signals.

USD/MXN climbs amidst a risk-off impulse as some Republicans said they would oppose a bipartisan agreement to lift the US debt ceiling, even though the US government could fail to pay its obligations. That shifted sentiment while US bond yields plunged. At the time of writing, the USD/MXN is trading at 17.6757, a gain of 0.52%.

GOP opposition threatens bipartisan debt ceiling agreement, fuels economic uncertainty, USD/MXN climbs

US equities trade mixed; after a sudden shift in market sentiment, major indices pared their earlier gains. The US debt ceiling saga continues, with the GOP right-wing expected to oust Kevin McCarthy as House Speaker. On the data front, the US housing prices in March rose above estimates though they failed to trigger a reaction on the USD/MXN pair.

Later, the US Conference Board (CB) revealed that Consumer Confidence in May slowed to 102.3, above estimates but below April’s 103.7. “Consumer confidence declined in May as consumers’ view of current conditions became somewhat less upbeat while their expectations remained gloomy,” said Ataman Ozyildirim, Senior Director, Economics at The Conference Board. The report showed that Americans’ inflation expectations remain elevated but stable at a 6.1% average over the next 12 months.

The Dallas Fed Manufacturing Index for May plummeted by -29.1, below the previous month’s -23.4 contraction, signaling that business activity continued to deteriorate.

Aside from this, Richmond Fed President Thomas Barkin said that parts of the economy are giving mixed signals and that inflation is going to be more stubborn “than many people would think.”

The US Dollar Index (DXY), a gauge that measures the buck’s value against a basket of six currencies, is down 0.06%, at 104.116.

USD/MXN Price Analysis: Technical outlook

After two consecutive days of losses, the USD/MXN shifted upwards, though the rallies could be capped by solid resistance at the 20-day Exponential Moving Average (EMA) at 17.7600. Oscillators like the Relative Strength Index (RSI) indicator and the 3-day Rate of Change (RoC) are still in bearish territory, but the RSI is about to cross above the 50-midline.

For a bullish scenario, once USD/MXN buyers reclaim the 20-day EMA, that would open the door toward the confluence of a one-month-old falling resistance trendline and the 50-day EMA at 17.9593. Once cleared, the 18.00 figure is up for grabs. Conversely, the USD/MXN must reclaim the weekly low of 17.5341 before challenging the year-to-date (YTD) low of 17.4238.

- USD/CAD bulls are starting to graze on the bearish correction.

- Trendline support could well be respected leading to a bullish continuation.

The Canadian dollar edged higher against the US Dollar on Monday as a deal to temporarily suspend the US debt ceiling boosted investor sentiment. Technically, however, the correction could be grazed upon by hungry bulls as the following will illustrate.

USD/CAD daily charts

The market is carving out a W-formation and with prospects of an upside continuation.

Zooming in, we can see that the price has rallied to make new highs only to correct back into the rally ina 50% mean reversion. This could encourage the bulls to reengage at a discount with the price respecting the trendline support.

USD/CAD H4 charts

From a lower time frame perspective, the price will need to clear the recent highs. This will mark a new bullish structure for the bulls to lean against in positioning for higher highs to come. On the other hand, a break of 1.3570-50 would be a bearish development.

- USD/JPY declined for two consecutive days following remarks from Japanese authorities indicating increased scrutiny of currency market movements.

- Japanese Yen strengthens in response to the news, putting downward pressure on the USD/JPY pair.

- USD/JPY maintains an upward bias as long as it holds above the key level of 138.74, representing the May 18 daily high.

USD/JPY dropped for two consecutive days after Japanese authorities expressed that currency market moves would be watched, following a meeting between the Bank of Japan (BoJ) and Masato Kanda, vice finance minister for international affairs. After those remarks, the Japanese Yen (JPY) strengthened. At the time of writing, the USD/JPY is trading at 139.87, losing 0.40%.

USD/JPY Price Analysis: Technical outlook

USD/JPY remains upward biased as long as the pair remains above the May 18 daily high of 138.74, though the recent pullback could be attributed to market sentiment deterioration. Additionally, the Relative Strength Index (RSI) indicator, exiting from overbought conditions, could be one of the reasons, alongside plunging US Treasury bond yields.

That said, USD/JPY first support would be the 139.00 figure. A breach of the latter will expose the May 18 high, followed by the 138.00 figure. Next would be the confluence of a previous resistance trendline turned support and the 20-day EMA at 137.76.

Conversely, if buyers reclaim 140.00, that could open the door for further upside, like the year-to-date (YTD) high of 140.93, before challenging the 141.00 mark.

USD/JPY Price Action – Daily chart

- GBP/USD bulls are taking back control on a break of structure.

- The rally has taken out the bearish trendline resistance.

Sterling rose against a weaker dollar on Tuesday as British inflation remains in focus. This has forced the price higher and placed the bulls back in control as the following analysis will illustrate

GBP/USD H1 charts

The price has broken to the backside of the old bearish trendline resistance. This is a bullish development. The bulls could be encouraged to buy in again by the deep correction of the bullish impulse.

The price has made an M-formation and would be expected to run back toward the neckline of the pattern. A bullish continuation could occur on a break of the neckline.

The bulls will need to commit to the backside of the M-formation´s bearish impulse and trendline resistance while breaking the neckline and double top.

Thomas Barkin, President of the Federal Reserve Bank of Richmond, stated on Tuesday that he is seeing evidence that interest rate hikes are curbing demand. He is attending a webinar organized by the National Association for Business Economics.

According to Barkin, there is more willingness among businesses to increase prices, but that will continue until there is a decline in demand. He points out that some parts of the economy appear to be cooling, while others remain “vibrant.”

Market reaction

The US dollar is posting mixed results across the board on Tuesday, amid falling Treasury yields and risk aversion.

- WTI falls for the second consecutive day on concerns about the passage of the US debt-ceiling bill and conflicting statements from oil producers.

- Some Republicans express reluctance to pass the debt-ceiling pact, raising fears about the US government’s ability to meet its financial obligations.

- OPEC+ meeting on June 4 fuels market unease as speculations arise about potential oil production cuts.

Western Texas Intermediate (WTI), the US crude oil benchmark plummets for the second straight day by more than 4%, spurred by woes about whether the US Congress will pass the US debt-ceiling bill as some Republicans had expressed that they would not pass the pact. That, alongside mixed messages by crude oil producers, exerts downward pressure on WTI. WTI is trading at $69.58 after hitting a daily high of $73.33.

US Congress debates debt ceiling, OPEC+ meeting adds to market uncertainty

News emerged during the weekend that US President Joe Biden and US House Speaker Kevin McCarthy sealed an agreement to suspend the debt ceiling until January 1, 2025, but it{s pending approval by the US Congress. US Treasury Secretary Janet Yellen said that the US government could not pay its debt by June 5.

Aside from this, the Organization of Petroleum Export Countries and its allies (OPEC+) would meet on June 4, one day before the US debt-ceiling deadline. Investors are nervous about the outcome of oil production, as the Saudi Arabian Energy Minister Abdulaziz bin Salman warned short sellers, which are betting that prices will fall.

That increased speculations that crude oil output could be cut, while Russian Deputy Prime Minister Alexander Novak signaled that the world’s third largest producer would keep production unchanged.

On April 6, Saudi Arabia and other OPEC+ members announced 1.2 million barrels cut per day, triggering a jump of 6% in oil prices. Nevertheless, prices stabilized and erased those gains.

WTI traders should be aware of the release of China’s business activity report late this week, alongside Global PMIs, which could give us clues about the pace of growth of the global economy.

WTI Technical Levels

- EUR/USD snaps five-day losing streak, rises 0.30% in North American session following Eurozone data indicating easing inflation in some countries.

- US consumer confidence advances, supporting the gains but falls slightly below April’s figure, reflecting concerns about future business conditions.

- Inflation expectations are elevated but stable at an average of 6.1% over the next 12 months.

EUR/USD snaps five straight days of losses, rising some 0.30% in the North American session after a tranche of Eurozone (EU) economic data showed that inflation in some countries of the bloc appears to ease. Meanwhile, consumer confidence advances in the United States (US), capping the EUR/USD gains. At the time of writing, the EUR/USD is trading at 1.0727.

EUR/USD underpinned by upbeat sentiment, soft US Dollar

Wall Street trades mixed, though tech stocks climb on AI’s frenzy. The Conference Board (CB) revealed that Consumer Confidence in May rose to 102.3, below April’s 103.7, but exceeded estimates of 99. “Consumer confidence declined in May as consumers’ view of current conditions became somewhat less upbeat while their expectations remained gloomy,” said Ataman Ozyildirim, Senior Director, Economics at The Conference Board. The report showed that Americans are becoming pessimistic about future business conditions, though expectations for jobs and income remain steady.

Inflation expectations remain elevated but stable at a 6.1% average over the next 12 months.

Recently, the Dallas Fed Manufacturing Index for May plunged by -29.1, below the previous month's -23.4 contraction, signaling that business activity continued to deteriorate.

The US Dollar Index (DXY), a gauge that measures the buck’s value against a basket of six currencies, is down 0.06%, at 104.116.

Aside from this, the Eurozone economic agenda featured May inflation in Spain, with MoM figures at -0.1%, below estimates of 0.1% and well beneath the prior’s month reading of 0.6%. Annually based, inflation expanded by 3.2%, below forecasts of 3.5%.

Meanwhile, European Central Bank (ECB) speakers led by Lithuanian policymaker Gediminas Simkus commented that the ECB could raise ratees in June and July, echoing comments by many policymakers that June’s hike is not the last. Nevertheless, when speaking about September, he said, “it’s too early to say.”

EUR/USD Technical Levels

Economists at MUFG Bank expect a strong Nonfarm Payrolls report on Friday to provide further support to the greenback.

Focus to switch to health of US labour market from US debt ceiling

“Market attention in the coming days will now turn to the passage of the bill through Congress. While there is genuine unease about the deal amongst Democrats and Republicans which could make it a close call, we expect the deal to be passed to suspend the debt ceiling in time. By passing the deal ahead of the X date the US economy will avoid a bigger negative shock.”

“Assuming that US politicians don’t surprisingly reject the deal, market attention should switch back to the health of the US labour market in the week ahead including the release of the NFP report on Friday. The US rate market has been moving to price in a higher probability of another 25 bps hike from the Fed at next month’s FOMC meeting, which is now judged as more likely than not. Another strong employment report this week would further reinforce those expectations and encourage a stronger USD in the near-term.”

The USD is trading lower. Economists at Scotiabank analyze US Dollar Index (DXY) technical outlook.

DXY is breaking below rising trend support that has guided the market higher through much of May

“USD losses are broad across the G10 FX space and while losses for the DXY do not appear that significant at this point, the index is down for a third session in a row and short-term trading patterns show the index is breaking below rising trend support that has guided the market higher through much of May.”

“A soft close on the day would imply a (technical) peak in the DXY in the short run at least and greater downside risk for the USD after its uninterrupted 3.5% run higher over the month.”

- Gold rebounds sharply as government bond yields decline.

- XAU/USD climbs $30 from monthly lows to reach five-day highs.

Gold price is rising considerably on Tuesday, supported by a decline in government bond yields. XAU/USD hit a fresh daily high at $1,962 before pulling back towards $1,950.

Earlier in the day, XAU/USD hit a two-month low of $1,931 at the beginning of the European session before jumping more than $30 in a rally that started after Spain's inflation figures.

According to preliminary data, Spain's Consumer Price Index (CPI) dropped 0.1% in May, against expectations of a 0.1% increase, with the annual rate falling from 4.1% to 3.2%. These figures could be anticipating a larger decline in Eurozone inflation, due to be released on Thursday. Germany will report April's preliminary CPI data on Wednesday.

Meanwhile, US economic data will also take centre stage, with the focus on employment figures. ADP will release its report on Thursday, and Nonfarm Payrolls are due on Friday.

Bond yields are falling in Europe and the US, with the 10-year German bund yield standing at 2.37%, the lowest since May 18, and the 10-year Treasury yield at 3.73%, down 1% for the day.

Levels to watch

Despite the recent rebound in XAU/USD, the overall trend remains downwards. If the price manages to consolidate above $1,955, it could provide some support for the bulls and potentially lead to a more sustainable recovery. The next resistance levels are seen at $1,965 and $1,970.

On the flip side, if the price declines below $1,945, it could expose the next support level at $1,935, and then potentially test the recent bottom near $1,930.

Technical levels

- CB Consumer Confidence Index declined modestly in May.

- US Dollar Index stays in positive territory above 104.00.

Consumer sentiment in the US weakened slightly in May with the Conference Board's Consumer Confidence Index edging lower to 102.3 from 103.7 in April (revised from 101.3).

Further details of the publication revealed that the Present Situation Index declined to 148.6 from 151.8 and the Consumer Expectations Index stayed virtually unchanged at 71.5.

Finally, the one-year consumer inflation expectations ticked down to 6.1% in May from 6.2% in April.

Market reaction

The US Dollar Index clings to small daily gains slightly above 104.00 after this report.

Economists at Standard Chartered expect the US Dollar to weaken against the Euro and the Japanese Yen.

Pressure on BoJ to scrap policy unlikely to go away amid rising inflation in Japan

“EUR/USD to rise towards 1.09-1.10, USD/JPY to fall towards 133-134 over the next three months.”

“Unlike the Fed, we do not see the ECB altering its tightening bias for now, given the relatively stronger growth and greater inflation pressure.”

“USD/JPY also has room to reverse its initial disappointment from the BoJ ruling out any immediate change to its Yield Curve Control (YCC) policy. We believe that the pressure on BoJ to scrap policy is unlikely to go away amid rising inflation in Japan.”

- EUR/GBP accelerates losses to the 0.8830 region.

- The Sterling outperforms in a choppy trading session.

- EMU Consumer Confidence came in at -17.4 in May.

Further strength in the British pound dragged EUR/GBP to new YTD lows in the 0.8630/25 band on Tuesday.

EUR/GBP weaker on GBP-buying

EUR/GBP retreats for the third session in a row and seems to break below the consolidative theme in place since mid-May, just below 0.8700 the figure.

Renewed weakness in the cross came in response to the better tone in the quid, while the inconclusive price action in the dollar appears to have underpinned the sentiment in the risk-associated universe.

Some support for the euro also came after hawkish comments from the ECB’s Simkus, who advocated for further hikes in June and July.

In the euro docket, the final print of the Consumer Confidence matched the preliminary readings at -17.4 for the month of May, while Economic Sentiment and Industrial Sentiment in the broader Euroland weakened to 96.5 and -5.2 in the same period.

EUR/GBP key levels

The cross is retreating 0.44% at 0.8628 and the breakdown of 0.8547 (monthly low December 1 2022) would expose 0.8386 (weekly low August 17 2022) and finally 0.8249 (monthly low April 14 2022). On the other hand, the next resistance level aligns at 0.8750 (200-day SMA) followed by 0.8834 (monthly high May 3) and then 0.8875 (monthly high April 25).

- NZD/USD recovers early lost ground to a multi-month low, albeit lacks follow-through.

- Retreating US bond yields prompts USD profit-taking and lends some support to the pair.

- Bets for more Fed rate hikes, economic woes to act as a tailwind for the buck and cap gains.

The NZD/USD pair stages a goodish intraday bounce from the 0.6025 area, or its lowest level since November 2022 touched this Tuesday and touches a fresh daily high during the early North American session. Spot prices, however, struggle to capitalize on the move and currently trade around mid-0.6000s, nearly unchanged for the day.

A sharp intraday slide in the US Treasury bond yields trigger a modest US Dollar (USD) pullback from the highest level since mid-March touched this Tuesday, which, in turn, lends some support to the NZD/USD pair. This, along with a positive risk tone, undermines the safe-haven Greenback and further benefits the risk-sensitive Kiwi. The market sentiment gets a minor boost in reaction to a tentative agreement to suspend the US government's $31.4 trillion debt ceiling til January 2025 and avert an unprecedented American default.

That said, expectations that the Federal Reserve (Fed) will keep interest rates higher for longer could act as a tailwind for the US bond yields and favours the USD bulls. The recent hawkish remarks by a slew of influential Fed officials lifted market bets for another 25 bps lift-off in June. The speculations were reaffirmed by the stronger US Core PCE Price Index released on Friday, which pointed to sticky inflation. This, along with worries about slowing global economic growth and fresh US-China tensions, could cap antipodean currencies, including the Kiwi.

Apart from this, the Reserve Bank of New Zealand's (RBNZ) explicit signal last week that it was done with its most aggressive hiking cycle since 1999 might hold back traders from placing aggressive bullish bets around the NZD/USD pair. This, in turn, suggests that the path of least resistance for spot prices is to the upside and any subsequent move up might still be seen as a selling opportunity. Traders now look to the release of the Conference Board's US Consumer Confidence Index, which might influence the USD and provide some impetus to the major.

Technical levels to watch

Loonie makes marginal headway after the 1.3660 test. Economists at Scotiabank analyze USD/CAD technical picture.

Break below 1.3560 should see losses extend a bit further toward 1.3520/25

“Short-term trading patterns look a bit soft for USD/CAD as the market backs a bit further away from technical resistance at 1.3660. But there is not really much evidence of a reversal in intraday/daily chart patterns at this point.”

“Intraday trend support at 1.3560 is within reach, however, and a break below here should see USD losses extend a bit further towards moving average support clustered around 1.3520/25.”

- House prices in the US continued to rise in March.

- US Dollar Index holds steady at around 104.00.

House prices in the US rose by 0.6% on a monthly basis in March, the monthly data published by the US Federal Housing Finance Agency showed on Tuesday. This reading followed February's increase of 0.7% (revised from 0.5%) and came in better than the market expectation of +0.2%.

Meanwhile, the S&P/Case-Shiller Home Price Index arrived at -1.1% on a yearly basis in March, down from +0.4% recorded in February.

Market reaction

These data don't seem to be having an impact on the US Dollar's performance against its rivals. As of writing, the US Dollar Index was virtually unchanged on the day at 104.05.

Economists at Scotiabank analyze EUR/USD technical outlook.

Technicals look favourable

“Intraday trading patterns are positive for the EUR.”

“Spot’s snap higher form the session low has developed into a short-term bull ‘hammer’ signal and gains have extended through the May downtrend resistance at 1.0720 (now support).”

“Gains will have to develop a bit more and hold on a daily closing basis but corrective EUR gains could extend a bit more towards 1.0775/1.0825 from here.”

See: EUR/USD may be gently making its way to the March lows at 1.0515/0530 – ING

- USD/CAD struggles to capitalize on its modest intraday uptick amid a slight USD pullback.

- Rising bets for more rate hikes by the Fed act as a tailwind for the buck and the major.

- A fresh leg down in Oil prices further undermines the Loonie and lends support to the pair.

The USD/CAD pair attracts some intraday selling on Tuesday and drops to a four-day low during the early North American session. Spot prices, however, manage to rebound a few pips in the last hour and currently trade just below the 1.3600 mark, nearing unchanged for the day.

The US Dollar (USD) pulls back from its highest level since mid-March touched earlier this Tuesday amid a sharp intraday slide in the US Treasury bond yields and turns out to be a key factor acting as a headwind for the USD/CAD pair. That said, firming expectations that the Federal Reserve (Fed) will keep interest rates higher for longer might continue to lend support to the US bond yields and favours the USD bulls.

In fact, the current market pricing indicates a greater chance of another 25 bps lift-off at the June FOMC policy meeting and the bets were reaffirmed by the recent hawkish remarks by a slew of influential Fed officials. Adding to this, the stronger US Core PCE Price Index released on Friday pointed to sticky inflation, which should allow the US central bank to maintain its hawkish stance and continue raising interest rates.

Apart from this, the prevalent cautious market mood supports prospects for the emergence of some dip-buying around the USD. Investors remain concerned about slowing global economic growth, which, along with fresh US-China tensions, overshadows the latest optimism over a tentative deal to suspend the US government's $31.4 trillion debt ceiling until January 2025 and avert an unprecedented American default.

Furthermore, a fresh leg down in Crude Oil prices seems to undermine the commodity-linked Loonie and further contributes to limiting the downside for the USD/CAD pair. The aforementioned fundamental backdrop suggests that the path of least resistance for spot prices is to the upside. Hence, any subsequent slide is more likely to remain limited as traders now look to the Conference Board's US Consumer Confidence Index.

Technical levels to watch

-

Oil price has weakened as investors start to fear the deal to extend the debt ceiling may be derailed by Congress.

-

Mixed messages from OPEC+ members further confuse the market – next meeting is June 4.

-

Odds still favor a rate hike from the Fed at their next meeting, putting downward pressure on Oil.

Oil price slides lower on Tuesday as investors question whether the debt-ceiling deal will get voted into law. At least two rebel Republicans and one Democrat have voiced their disapproval and may vote against the deal. If the US defaults on its obligations, financial chaos is expected to follow, probably hitting the Oil price, though some analysts have said the US Dollar might also suffer, which would be positive for Oil since it is mostly priced in USD. Mixed messaging from OPEC+ adds to the opaque outlook.

At the time of writing, WTI Oil is trading in the upper $71s and Brent Crude Oil in the upper $75s.

Oil news and market movers

-

Oil price loses ground as investors worry about whether the debt-ceiling deal agreed by President Joe Biden and Republican House Speaker Kevin McCarthy will get enough votes in both Congress and the Senate to pass into law.

-

A vote in Congress could be as soon as Wednesday, but so far, at least two House Republicans have voiced their displeasure at the idea of increasing the country’s already gigantic debt pile. For different reasons, Democrat Riche Torres has criticized the cuts to disability benefits that form part of the agreement.

-

Both the debt deal as well as robust US macroeconomic data has increased market expectations that the Federal Reserve (Fed) will have to raise interest rates to combat rising inflation expectations – bullish for the US Dollar; bearish for Oil.

-

The CME FedWatch tool shows a 58% chance of the Fed raising interest rates by 0.25% at their meeting on June 14 (at time of writing).

-

Although this is down from the previous day’s 60% it still shows the odds favor a rate hike at the June meeting rather than no change as had been the prior expectation.

-

Oil traders further await the outcome of the next meeting of OPEC+ on June 4, when the possibility of production cuts has been mooted.

-

Investors remain a little confused as two of OPEC+’s largest members seem to be giving divergent messages over what might happen.

-

Last Tuesday, May 24, Saudi Oil Minister Prince Abdulaziz bin Salman seemed to imply OPEC+ might cut production quotas when he warned speculators (interpreted as short-sellers) to “watch out” and expressed support for OPEC’s October decision to cut supply.

-

Russia’s Energy Minister Alexander Novak, however, later played down the idea of production cuts. “I don't think that there will be any new steps, because just a month ago certain decisions were made regarding the voluntary reduction of oil production by some countries," he said.

Crude Oil Technical Analysis: Mixed technical outlook leads to waiting game

WTI Oil is in an established downtrend from a technical perspective, making successive lower lows, and so given the old adage that the trend is your friend, this overall favors short sellers over longs. WTI Oil is trading below all the major daily Simple Moving Averages (SMA) and all the weekly SMAs except the 200-week, which is at $66.90.

-638210468658146607.png)

WTI US Oil: Weekly Chart

That said, a possible bullish right-angled triangle may have just finished forming, as shown by the dotted lines on the chart below.

-638210469200364125.png)

WTI US Oil: Daily Chart

Price initially seemed to break out above the upper borderline of the triangle on May 24 but then failed to follow through higher and reversed, forming a spinning top Japanese candlestick reversal pattern in the process. It then rallied on Monday before capitulating again and is currently trading back below the lower border.

A decisive break below the May 22 lows of $70.65, or better still, the $69.40 May 15 lows, would provide confirmation that the triangle is actually breaking out lower. Such a break ought to be represented by a long red candlestick or three down-days in a row for solid confirmation.

A break below the year-to-date (YTD) lows of $64.31 would imply a new lower low was forming, reigniting the downtrend. The next target from there would be at around $62.00, where trough lows from 2021 will come into play, followed by support at $57.50.

A breakout higher is still possible, however. The three green up bars in a row that occurred prior to the bullish breakout on May 24 are a strong signal, suggesting there is still a chance price could recover.

Oil price needs to climb back above the $74.70 May 24 highs for confirmation.

Such a bullish breakout could see Oil price rise in a volatile rally to a potential target in the $79.70s, calculated by using the usual technical method, which is to take 61.8% of the height of the triangle and extrapolate it from the breakout point higher. Oil price could even go as far as a 100% extrapolation, however, the 61.8% level roughly coincides with the 200-day SMA and the main trendline for the bear market, heightening its importance as a key resistance level.

Assuming Oil price reaches its target, a bullish break would also signify that price had surpassed the key $76.85 lower high of April 28, thereby, bringing the dominant bear trend into doubt.

The long hammer Japanese candlestick pattern that formed at the May 4 (and year-to-date) lows is a further sign that Oil price may have formed a strategic bottom.

Further, the mild bullish convergence between price and the Relative Strength Index (RSI) at the March and May 2023 lows – with price making a lower low in May that is not matched by a lower low in RSI – is a sign that bearish pressure is easing.

WTI Oil FAQs

What is WTI Oil?

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

What factors drive the price of WTI Oil?

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

How does inventory data impact the price of WTI Oil

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

How does OPEC influence the price of WTI Oil?

OPEC (Organization of the Petroleum Exporting Countries) is a group of 13 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

UOB Group’s Senior Economist Julia Goh and Economist Loke Siew Ting review the latest inflation figures in Malaysia.

Key Takeaways

“Headline inflation recorded a small blip, as it eased to 3.3% y/y in Apr (from +3.4% in Mar), marking an eighth straight month of deceleration and the lowest level since May 2022. The outturn matched our estimate and Bloomberg consensus. It was largely thanks to softer food and services (i.e. restaurants & hotels, education, healthcare, and packaged tours) price inflation amid diminishing base effects and the implementation of Festive Season Maximum Price Control Scheme (SHMMP) for Hari Raya Aidilfitri from 14-30 Apr.”

“Apr’s inflation reading further affirms our view that the disinflationary process will persist at a moderate pace throughout the remaining months of the year. In recent weeks, the government also hinted that the prospects of implementing a targeted subsidy mechanism remain intact but the timeline of execution (particularly for fuels) may be pushed to next year instead of in 2H23. With that, we maintain our 2023 full-year inflation forecast at 2.8% (BNM est: 2.8%-3.8%, 2022: 3.3%), while not factoring in any impact of government’s gradual subsidy rationalization.”

“Manageable inflation expectations and slowing economic growth momentum will continue to give central bank breathing room to maneuver its monetary policy stance as we enter 2H23. Core inflation extended its downtrend and eased at a faster pace than headline inflation in Apr, reflecting the lagged effects of past interest rate hikes and cautious consumer sentiment in light of heightened uncertainty surrounding the global and domestic economy. The existing price controls and fuel subsidies are also expected to further contain the extent of upward pressures to inflation in the near term. Recognizing these developments and peaking of global interest rates, we continue to expect no further adjustment in the Overnight Policy Rate (OPR, current: 3.00%) for the rest of the year.”

- The Turkish lira extended the selloff to the 20.40/45 band.

- The lira's exodus accelerated after Erdogan's win on Sunday.

- Erdogan reaffirmed the continuation of a low-rate policy.

The Turkish lira (TRY) magnifies its decline vs. the greenback and propels USD/TRY to a new record top north of 20.40 on turnaround Tuesday.

The Turkish lira is poised for further weakness

The march north in USD/TRY remained unabated on Tuesday amidst the unabated sell-off in the lira, which was particularly magnified after incumbent Recep Tayyip Erdogan secured his victory in the 2023 presidential election, extending his rule into a third decade in power.

The deep pullback in TRY comes pari passu with quite a pessimistic economic outlook for the country, which can even get worse after President Erdogan reaffirmed the continuation of the unorthodox (unreal? Non-sensical?) policy of tackling the elevated inflation with low interest rates.

Further concerns also emerge in a context where the country's FX reserves do everything but grow and the current account deficit flirts with its widest in series history.

It is worth noting that the pair has closed with gains in every single week since March 1.

Later on Tuesday, Trade Balance figures for the month of April will be the sole release in the domestic docket ahead of Q1 GDP results on Wednesday and the Manufacturing PMI on Thursday.

USD/TRY key levels

So far, the pair is gaining 1.37% at 20.3879 and faces the next hurdle at 20.4196 (all-time high May 30) followed by 21.00 (round level). On the downside, a break below 19.3967 (55-day SMA) would expose 19.1366 (100-day SMA) and finally 18.8192 (200-day SMA).

Sterling is the top-performer on the session as shop price data shows further gain. Economists at Scotiabank expect the GBP/USD pair to test the upper 1.24s.

UK shop prices continue to surge

“The BRC’s survey of shop prices reached 9% in May (a record) suggesting no relenting from the upward push in prices and reinforcing expectations that the BoE has more – perhaps quite a bit more – work to do.”

“Strong intraday bidding for the Pound leaves a positive impression on the short-term chart.”

“Congestion/retracement resistance stands at 1.2450/1.2495.”

Economists at Société Générale analyze EUR/SEK technical outlook.

Peak achieved in 2009 at 11.78 could be an important resistance

“EUR/SEK has recently overcome the upper part of its consolidation since February affirming resumption in uptrend. It is approaching next projections of 11.63/67 which is also a multi month channel band. An initial pullback is expected after achievement of this zone however upper limit of previous range at 11.42 should be an important support; only if this gets violated would there be risk of an extended correction.”

“The peak achieved in 2009 at 11.78 could be an important resistance near term.”

Senior Economist Alvin Liew at UOB Group assesses the latest results from Industrial Production in Singapore.

Key Takeaways

“Singapore’s industrial production (IP) contracted more than forecast in Apr, affirming the weak manufacturing outlook. IP contracted by -1.9% m/m, -6.9% y/y in Apr, worse than Bloomberg’s median forecast of +0.1% m/m, -4.5% y/y and our forecasts of -0.7% m/m SA, -3.9% y/y. Meanwhile, the March IP was revised higher to 9.7% m/m, -3.8% y/y (versus the prelim estimates of 9.3% m/m SA, -4.2% y/y in Mar. This was the seventh consecutive month of y/y decline and the worst streak since 2015 (11 months of y/y declines). Excluding the volatile biomedical manufacturing, IP actually rose by 2.2% m/m (from +5.4% m/m in Mar) which translated to a smaller contraction of -6.1% y/y in Apr (from -5.6% y/y in Mar).”

“IP Outlook – While we are heartened by the continued growth in the transport engineering components of aerospace and marine & offshore, the latest Apr IP print continues to affirm our downbeat manufacturing outlook due to the worsening electronics downcycle and weaker external demand. We maintain our forecast for Singapore 2023 manufacturing to contract by 5.4%.’

- EUR/USD rebounds from multi-week lows near 1.0670.

- The selling pressure could mitigate somewhat above 1.0830.

EUR/USD manages to regain some buying interest soon after bottoming out in new 10-week lows near 1.0670 on turnaround Tuesday.

The pair remains under heavy pressure despite the corrective bounce, although the selling mood could alleviate a tad on a convincing close above the weekly high of 1.0831 (May 22). Immediately to the upside, in the meantime, appears the transitory 100-day SMA at 1.0814.

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0488.

EUR/USD daily chart

Senior Economist at UOB Group Alvin Liew comments on the latest release of the FOMC Minutes of the May gathering.

Key Takeaways

“According to the latest FOMC minutes (released on 25 May, 2am SGT), while the Federal Reserve (Fed) policymakers in its 2/3 May 2023 Federal Open Market Committee (FOMC) meeting, unanimously agreed to raise the Fed Funds Target Rate (FFTR) by 25-bps to 5.00%-5.25%, there was a lack of collective agreement on the next move.”

“Recall in the May policy decision, the Fed made a significant change in the forward guidance of its monetary policy statement (MPS), as it removed a key part of the FOMC statement, ‘some additional policy firming may be appropriate’ (from the Mar FOMC) and replaced it with ‘In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments’.”

“FOMC Outlook – Done At 5.25% And Pause For Rest Of 2023. The change in language of the May FOMC statement and the lack of collective agreement among FOMC policymakers on the next policy move, implies our base case for a pause in the Jun FOMC remains valid. We still expect the 25-bps hike in the May FOMC to be the last one in the current Fed rate cycle and a pause thereafter. We continue to expect no rate cuts in 2023, with the FFTR terminal rate at 5.25% to last through this year.”

- DXY fades the earlier bullish move to new 2-month highs near 104.50.

- The resumption of the uptrend should retarget the 200-day SMA.

DXY comes under fresh downside pressure following earlier peaks past 104.50 on Tuesday.

In the near term, extra gains appear on the cards despite the ongoing knee-jerk. That said, the surpass of the May high at 104.53 (May 30) should put a potential visit to the key 200-day SMA, today at 105.65, back on the radar prior to the 2023 top of 105.88 (March 8).

Looking at the broader picture, while below the 200-day SMA the outlook for the index is expected to remain negative.

DXY daily chart